What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

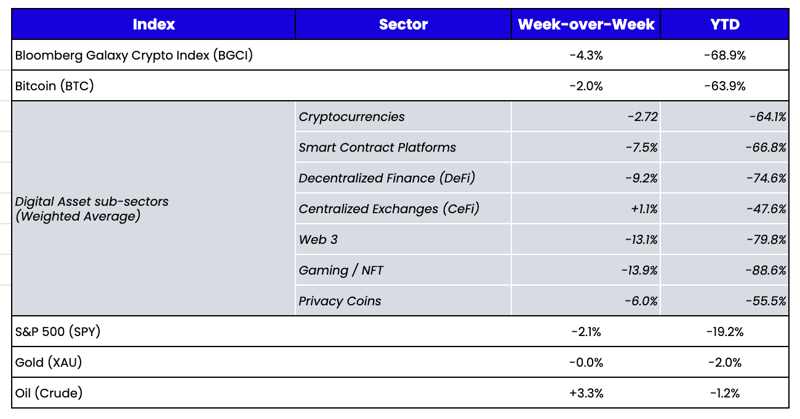

Week-over-Week Price Changes (as of Sunday, 12/18/22)Source: TradingView, CNBC, Bloomberg, Messari

Good Riddance, 2022!

It would be the understatement of the century to say that 2022 witnessed quite a few surprises. By all measures, this was a pretty terrible year for investing broadly and for blockchain investing especially. Before you dive into our 2023 Digital Asset Industry Outlook, let’s review some of the major developments in 2022 and what’s on deck for the next few weeks before we turn the calendar page. A quick trip down Two Satoshis lane reminds us that many of this year’s major themes, failures, and disruptions were discussed heavily throughout the year, with some people even predicting the events long before they happened.

Theme: The Fed Raising Interest Rates

The majority of digital assets participants had never paid attention to jobless claims, CPI reports, or FOMC meetings before 2023, but this year, everyone tried to become a macro expert. The market focus on inflation and subsequent inflation-fighting rate cuts started as far back as October 2021 and continues today.

(Nov 2021): “While some have tried to dismiss inflation while others have gone to the far extreme of calling for hyperinflation (sigh), the reality, of course, lies somewhere in the middle. The inflation we’re seeing today is real, has been persistent, and is hurting people’s pocketbooks. On the other hand, hyperinflation is not a real risk in a country that has an aging population, massive debt load, highly diversified and dynamic economy, and who controls the global reserve currency. It’s critical to recognize the current inflation as a problem without blowing it out of proportion so that we can be prudent in our policy choices and investment decisions...[G]iven the future base rates of U.S. GDP growth and CPI inflation and the momentum markets are showing currently, we believe the inflationary boom could persist for another few months, with positive implications for digital assets. However, we believe this will eventually give way to first a mild (Q1 2022), then moderate to severe (Q2) disinflationary bust. While inflationary booms have historically been favorable for digital assets, disinflationary busts are associated with increased volatility, lower returns and higher risk of crashes. The greater the magnitude of the slowdown, the more likely that risk assets, including digital ones, will suffer accordingly.

(Jan 10): “… [The] release of minutes from the Fed’s December policy meeting triggered anxiety that rippled across global markets. In short, the minutes were hawkish but were largely in line with what had been communicated by the Fed over the past two months…the first week of the new year resulted in heavy selling of growth stocks, a rotation into value stocks, a steep rise in long-term interest rates (curve steepened), and a sharp decline in digital assets. Again, the information was not entirely new, but investors were caught off guard by the forcefulness and level of consensus shown in the minutes.”

(Apr 11): “Today, the inflation that the Fed caused and miscalculated is startling them. And markets are putting a lot of faith in the Fed’s ability to stick with, and execute, a telegraphed plan to combat it, increasing expectations of rate hikes to 9 from 3 earlier this year, even as the forward curve is already pricing in rate cuts again as early as 2023. The same Fed that in 2020 projected a greater than 2% inflation rate while at the same time projecting numbers that contradicted their own projection.”

(May 9): “While pretending to fight inflation is the target of the Fed’s current monetary policy, it’s anyone’s guess whether or not real economic contraction and a market crash will ultimately cause the Fed to bring back the “Fed put” and ease up on its rate stance. The Fed and other central banks worldwide are playing a giant game of chicken. They know rate hikes don’t actually fight supply-side inflation, and rates markets have already priced in 2 years of rate hikes anyway. So the only real inflation risk is that consumers fear inflation so much that they make it worse by front-loading purchases (if you think prices will go higher, you buy more now, driving prices higher faster). As a result, the Fed's primary tactic is to jawbone about how they are "tackling inflation" just long enough to keep consumers at bay until natural deflationary forces lower inflation organically (which is already happening).”

Theme: DeFi Is Thriving, With Countless Examples of Humanless Protocols Outperforming Humans

Many centralized businesses that utilize blockchain failed miserably this year. By contrast, similar DeFi competitors thrived. It was clear that the power of DeFi—and its usefulness going forward—greatly improved in 2022 by way of default. We’ve been trying to clear up confusion and misinformed attacks for years, but it’s nice to see that the products are starting to tell the story themselves.

(Jan 31): “…[I]n digital assets, most of these events rise and fall within weeks, and any wrongdoings are discovered immediately by amazing DeFi on-chain detectives (like those that identified SiFu’s misdeeds). That cannot be understated: the on-chain detectives of DeFi are doing exceedingly more positive, and real-time self-policing of this industry than any regulator will be able to do. As a result, most of the issues within DeFi are either very easy to avoid with even a shred of due diligence or discovered immediately due to the public records of blockchain. Misinformed attacks on Web3 and DeFi will ultimately be on the wrong (and losing) side of history.”

(Feb 7): “For example, everything that could go wrong for DeFi and Layer 1 protocols did go wrong last week, yet all of the applications survived the 3rd biggest stress test we've had in the last 2 years (the others occurred in May 2021 and March 2020).”

(Apr 25): “But let’s not sit on our high horse and pretend that DeFi doesn’t solve some real-world problems while ignoring the multitude of issues that banks and brokerages continue to cause. A paradigm shift in the existing financial system is long overdue. I believe that transformation will happen through the real-world accessibility to manage life functions that DeFi enables.”

(Jun 21): “Decentralized lenders and applications are NOT failing; it’s the centralized lenders and businesses that are failing. We wrote about how DeFi apps worked with zero downtime or issues during the January 2022 meltdown, we wrote about how DeFi solves real-world problems when banks cut off their customers, and we’ve debunked many of the nonsensical statements made by naysayers. And once again, during the current wreckage, DeFi stands alone regarding transparency and health.”

(Jun 27): “While DeFi is having its breakout moment, investors in DeFi are struggling to generate yield as the widespread deleveraging is putting pressure on once plentiful yields. Perhaps these yield-hungry investors need to look at the bond market as an alternative.”

(July 5): “There is nothing new or innovative about how these lenders became insolvent. For as long as there have been centralized lending businesses, there have been epic failures such as what this crop of crypto lenders experienced in this circumstance. The technology that underpins cryptocurrencies and DeFi has nothing to do with why 3AC and these lenders got into trouble.”

(Jul 25): “On the flip side, there is one area of digital assets we’re seeing great progress on the transparency front: you guessed it, DeFi. From Dune Analytics and Token Terminal to token issuers' dashboards, blockchain-based financials are readily available in real time for digital asset investors. It’s like getting an 8-K every day, so it’s nearly impossible to miss when information changes that could adversely affect customers and/or investors.

Yet, in the end, it’s another rallying cry for how successful DeFi has become. DeFi protocols keep getting stronger through the market’s counterparty concerns. There are knock-on effects driven by this lack of trust in centralized counterparties and subsequent faith in DeFi. For instance, the rise in self-custody is evident in the increase in hardware wallet sales (Ledger and Trezor reported record sales last week).” (Nov 28)

Theme: DeFi Hacks

Of course, you can’t talk about the success of DeFi without discussing the downside—it’s still generally very risky to use the newest applications that haven’t been properly battle-tested. While most of the hacks occurred on bridges rather than via the protocols and applications themselves, in the eyes of most potential DeFi users, it’s all the same. If you don’t believe you’ll get all of your assets back, it doesn’t matter how well the platform performs.

(Feb 7): “…[A] hacker infiltrated a bridge between Ethereum and Solana called ‘Wormhole’ and stole 120,000 ether worth about $325 million. According to the ‘Rekt’ leaderboard, this was the 2nd largest hack on record—many other instances came from other DeFi bridge hacks.”

(Apr 25): “DeFi growth has been somewhat stagnant since November 2021. Activity has slowed amidst a dull, declining market, and the price of DeFi tokens has been straight down since peaking in February 2021. In addition, there has been a constant flow of hacks that have kept the media salivating over DeFi’s demise.”

(May 2): “The sell-off quickly became known as ‘Scarlet Saturday,’ as it was driven by a flurry of negative news, including Solana going down again and another DeFi hack.”

Theme: The Need for Better Governance in Digital Assets (and the Lack of Progress in 2022)

We’ve been talking about governance for almost five years, with a keen interest in why governance is so important, mixed in with reality about how disappointing most governance has been thus far. While we’ve seen some success stories, the bear market of 2022 has exacerbated this trend and there has yet to be much progress.

(Jan 24): “Equity markets have clearly defined stakeholder structures for investor recourse. These structures have resulted in governance systems that protect investor interests. But cryptocurrencies have largely been shielded from similar oversight. Decentralization was meant to empower communities to participate, voice their views, provide feedback via forums/proposals, and vote collectively. Unfortunately, voter participation is still at extremely low levels in digital assets. For example, recent proposals have only averaged 1-9% voter participation rate versus up to 90% for public equities historically.”

(Oct 10): “We will get DAO governance right one day, but today it is often a no-consequence sham.”

Theme: Stakeholder Alignment

While we still need to solve how to govern, the token structure itself does create the alignment and incentives to achieve greatness. A common theme in 2022 was how often we found ourselves discussing ways in which token structure created necessary alignment or pointed out situations whereby issuing a token would greatly improve an existing company.

(Mar 14): “Digital assets are the greatest capital formation and customer bootstrapping mechanism we’ve ever seen that fully aligns all stakeholders, from customers to founders to passive token holders.”

(Mar 28): “Tokens allow companies to turn intangible assets like their brands, customer loyalty, and networks into tangible assets. Companies and projects in the digital asset world pre-fund themselves via the sale of tokens, thereby creating a service liability in how the token is ultimately redeemed in the future. The token can unlock usage of the product, can be used for discounts on services rendered, or in some cases, can even gain economically via direct claims on future revenue. This process is similar to companies that sell gift cards, which tend to speed up revenue recognition (booked upfront), but create a liability for the company in terms of future services/products delivered. Notably, these future services don’t disappear during a recession and, as such, technically do not lose value.”

(Apr 11): “A Twitter token could have much of the same hybrid characteristics of today’s top centralized tokens:

- 10-20% of revenues or profits distributed via dividend or buyback to tokenholders, increasing stickiness and loyalty of its users

- Governance rights over the platform’s features—like an edit button

- The ability for tokenholders to lock up some of their TWTR tokens to earn more tokens via inflationary rewards

- Tweet to earn—tokenholders earn more tokens the more they participate (tweet, share, engage)

May 31): Today, tech companies are struggling. They are struggling with earnings, with employee and customer retention, and with moat. For example, Netflix (NFLX) stock is down -71% from its all-time highs and Peloton (PTON) stock is down over -90% from its all-time highs. The companies face steep competition and have customer retention concerns. Issuing a token could address both.

Theme: The Long Wait for Regulation

As much as we (and an extensive chorus of others) talked about regulation in 2022, nothing actually happened. Unfortunately, a massive fraud and hundreds of millions of dollars worth of lost assets may be the pivotal event that gets Congress’ and regulators’ full attention.

(Mar 14) “…President Biden released the long-awaited digital assets executive order. Many are calling this a pivotal moment for the industry, even though it will undoubtedly lead to more questions than answers and certainly won’t lead to any action in the short-term.”

(Mar 14): “The existing regulatory framework has been fragmented and disorganized, with states, the CFTC, SEC, IRS, and US Treasury Department each implementing different and sometimes contradictory approaches. As a result, both market participants and policymakers have been calling on the government to provide more regulatory clarity with agency responsibilities better defined.”

(Jun 6): “The NY AG also appears to be fighting for regulatory relevance in a time when the federal financial regulators are each making their plays for dominance—DOJ/US Attorney, CFTC, SEC, OCC, Fed.”

(Aug 15): The banning of Tornado Cash

(Sep 12): “We’ve seen quite a few headlines from Gary Gensler over the past few years, usually striking a similar tone (the following is paraphrased):

All tokens are securities.

The SEC should be the agency that regulates digital assets.

The digital assets market needs a ‘cop on the beat’ to keep investors safe.”

Theme: TradFi Entering the Space

While those already in the digital asset industry are suffering, the incoming class is celebrating being largely unscathed and ready to capitalize on the successes while heeding the mistakes. TradFi companies, specifically, are overwhelmingly entering the market.

(Mar 28): “…It’s unsurprising that we continue to see more TradFi participants entering the digital assets arena. For example, just this past week, we saw:

- Cowen Inc, a +100-year-old investment bank, will be offering spot trading capabilities to institutional clients.

- Goldman Sachs launched a new website design that features the words ‘cryptocurrencies’ and ‘metaverse’ on the front page. The company also executed its first OTC Bitcoin derivatives trade.

- Blackrock, the world's largest asset manager, is exploring how to serve clients with digital currencies.

- Bridgewater is preparing to back its first digital assets fund.”

(May 2): “Last week, Goldman Sachs offered its first bitcoin-backed loan. While the details are scarce, it demonstrates the willingness of institutions to utilize new tools with old techniques. Everything about this is interesting—from the lender (Goldman) to the collateral (BTC) to the clientele (a Goldman client who was willing to structure a deal like this with a newbie to the digital assets arena).”

(Sep 26): “Starbucks unveiled a platform to allow employees and members of its rewards program to earn and purchase digital collectibles that will unlock access to new benefits and experiences on the Polygon blockchain. Ticketmaster tapped Flow blockchain to let ticket issuers issue NFTs. Consumer electronics company LG is building an NFT marketplace as a feature on a range of its TV on Hedera. U.S. investment firm KKR has made its Health Care Strategic Growth Fund available to a broader range of investors via representative tokens on Avalanche. Sweatcoin, a popular ‘walk-to-earn’ Web 2 app with nearly 100 million active users, tokenized a part of its business on the Near blockchain. On just the first day of the airdrop, Near saw more than 1 million active addresses. It was one of the most active days in the blockchain’s history and more than twice the number of users Ethereum had. As 13 million people downloaded the new Sweat Economy app on Near— likely the largest onboarding of users to Web 3 on record—we're likely to see further heavy usage of the chain going forward.”

Theme: So Many Crises and Not One Government Bailout

Some may say this is a failure of the system; others might say it’s what makes it beautiful. Broader contagion is not a risk, as the digital assets industry largely operates in its own world, with no government support to buoy the market. It rises and falls organically and shows us an alternative market structure free of government manipulation. Those that fail are allowed to fail and fail fast. Those that succeed do so on their own merit.

(May 23): “The market infrastructure seems far healthier than most think. A run on the market’s largest bank, a crash in asset prices, and a semblance of all hope lost have somehow been contained without bailouts or lifelines.”

(Nov 14): “We’ve been writing this weekly market recap for almost 5 years, and we’ve touched on every problem area in this industry: from leverage and lack of transparency to anointing heroes—all of which keep happening over and over again.”

(Nov 21): The Latest Victims: BlockFi, Gemini, DCG, Genesis, and Grayscale

(May 16): Luna/Terra Crash and Subsequent Luna Restructuring (May 31)

(Jun 21): Celsius/BlockFi/Three Arrows/Babel

Theme: Ethereum Merge

Ethereum and the long-awaited merger was one of the few bright spots this year. We talked about it a lot because it was a huge technological feat—one which we will likely be discussing for decades.

(Aug 22): Concerns About the Ethereum Merge Are Overblown

(Sep 19): The ETH Merge Was a Smashing Success

(Sep 6): “…[T]here is now a clear leader in the clubhouse for a single, pure-play way to gain exposure to everything happening in blockchain: Ethereum (ETH). Ethereum has a commanding lead over every other ecosystem when it comes to the growth of smart contracts, DeFi, Web3, NFTs, stablecoins, and gaming. Following the EIP-1559 proposal and the impending ETH 2.0 merge, the ETH token becomes a low-inflation (perhaps even deflationary), high value-capture way of expressing this view.

(Nov 14): “All of this on-chain activity has led to Ethereum reaching deflationary status, meaning since the merge to proof-of-stake (POS), more ETH has been removed from circulation via burns than has been issued to stakers via inflation.”

Theme: SBF/FTX

The collapse was, of course, sudden, but the buildup happened over years. The effects and ensuing court cases will last decades.

(Oct 24): “What's more telling—and hypocritical—is that the same exchanges listing the token—FTX, Coinbase, and Binance—are asking the SEC for more regulatory clarity. Huh? It's disingenuous to publicly appeal to the SEC for clear rules protecting investor rights while providing listing support for a project that lacks transparency and disclosure detail. Exchanges that have an investment arm have a clear conflict of interest and should be held to a higher standard independent of regulation. With this in mind, it’s not surprising that Sam Bankman-Fried is starting to take the heat (lots…of… heat—lots) for his recent proposal regarding digital asset regulation and new industry standards. On the surface, SBF has earned his stripes and his reputation; it’s nice that he is using his large platform and influence to try to enact change. He didn’t ask to be the market’s de facto leader, but he has become one and is rising to the challenge. But, on the other hand, the constant hypocrisy of begging for change while you are one of the biggest beneficiaries of the current “no rules” environment is a bit hard for some market participants to stomach.”

(Nov 7): FTX/Binance Drama and Speculation

(Nov 21): “We wrote this in late 2020 regarding FTX and Alameda: ‘Prior to launching FTX, Bankman-Fried also started Alameda Research, one of the premier liquidity providers (market makers) in the digital assets industry. The potential conflicts of interest and embedded risks are large when a digital assets exchange also acts as the largest market maker and the product creator of innovative futures and index products. With a complex corporate structure, Bankman-Fried’s wallets could be tied to a number of activities taken on by FTX and/or Alameda.’”

10 of the Most Relevant Digital Assets Stories to Follow Right Now

The past is the past, but the SBF saga is currently capturing everyone’s attention. But, at this point, neither the events of 2022 nor the FTX theater has any actual impact on the market anymore. Instead, there are a few factors that are more likely to affect prices and the investing landscape in the immediate future.

1. Audits: Only a handful of audit firms have been willing to enter the digital asset industry, largely due to the lack of clear accounting standards. Last week, several of the smaller auditing firms left abruptly. Mazars and Armanino are reportedly ending their efforts entirely, while BDO is reportedly “evaluating” its ongoing efforts. These firms act as auditors for some of the larger exchanges, lenders, and stablecoins including Binance, Crypto.com, Kraken, Nexo, and Tether. Now, this is obviously not a great situation. In the wake of the FTX scandal, auditors are rightfully on edge and face potential liability, similar to Arthur Anderson following the Enron scandal. While the Big 5 dropped to the Big 4 following Enron, the auditing industry didn’t go away. The future of digital asset audits will likely change as well, but it’s too big and lucrative of a business to disappear. The issue is that the auditors are still learning how to conduct their practices accurately and correctly in this new and growing space. It's one thing to prove you have assets in a wallet; it's quite another LONG ordeal to prove you have access to all of them by moving all of the assets one by one in front of the auditor. 2. Binance and Proof of Reserves: Speaking of audits, Binance came under pressure last week for releasing what was supposed to be a proactive measure to show “proof of reserves” because the market felt it was inadequate. As Noelle Acheson wrote:

“One positive consequence of the recent crypto drama is the mounting s[k]epticism around how crypto platforms handle their customer balances, and the scramble among these platforms to demonstrate that assets match liabilities through a process called ‘proof of reserves.’ This involves a cryptographic and audit demonstration that each client’s account is included in the liabilities, and that the assets meet or exceed the total amount. This has given rise to a new problem, however – the manipulation of what the public understands to be ‘proof of reserves.’ It turns out that, as is common in crypto, there is not an established definition, so exchanges can claim they are offering this service when in fact there are no guarantees established at all. Furthermore, proof of reserves does not necessarily show that customer assets are unencumbered. Users might not appreciate this, leading them to trust platforms that perhaps are not employing best practices.”

3. So what do you do now? Well, if you don’t trust Binance or any service provider in this industry, there isn’t much of a reason to leave your assets anywhere. But it is also possible to believe Binance is a good company with a useful exchange and still trade there, but not feel 100% certainty. A true exchange is a simple business that makes money on the spread/fees from trades and does not need to rehypothecate the assets. But a futures exchange is, by definition, not going to have a perfect asset/liability match due to the inherent nature of how futures and leverage work (which differs from a spot exchange where you can have a 1:1 asset/liability match). So for Binance and other exchanges, the solution for many may be to send assets in, trade, and then send the new assets out. There’s no need to custody assets at an exchange just because you trade there. Per the audit issues above, in the current "guilty ‘til proven innocent" environment, it's virtually impossible for Binance (or any exchange) to actually prove innocence in a timely fashion. No matter what they do, it won't be enough in naysayers' eyes. So be prepared for more volatility and headlines.

4. Inflation No Longer Matters; Growth Does: Markets are reacting much more to PMI, retail sales, jobs, earnings, and other growth indicators than to CPI. Inflation has peaked, the market knows it, and now we've switched into recession/growth fears. That's why Treasuries are moving inversely to stocks for the first time all year. Stocks down (low growth) is good for Treasuries, whereas previously, stocks down (high inflation) was bad for Treasuries. And that’s potentially good news for tokens, as there is a good chance that tokens are largely recession-proof.

5. FTX Does Not Absolve: Many failed digital asset entities (and there have been a lot this year) are now using FTX as a scapegoat, but these lenders and funds were broken business models long before FTX. Redemption arcs based on FTX’s implosion will not make unprofitable/unsustainable business lines come back. Expect low recoveries on those already under court supervision and bankruptcy, while some that have yet to restructure may still be heading in that direction.

6. Perfect Substitutes: For businesses that still work (stablecoins, exchanges, DeFi), all remaining players have perfect substitutes. A failure at one will have little to no long-lasting market impact. With perfect substitutes, customers can seamlessly move elsewhere. So while the witch hunts continue, any future failings will likely have limited market impact other than sentiment and fear.

7. Yield Still Exists: Yield comes from 1) demand for working capital and 2) incentives. Both of these still exist. Funds and market makers still need working capital, and protocols and apps will still incentivize certain behaviors by issuing tokens. While many lenders are dead, longer term, lending is not. That said, with short-term Treasury yields above 4%, HY bonds at 8%, and COIN and GLXY bonds at 15-20%, the bar for yield is significantly higher. Expect 25-100% APRs to be the norm and commensurate with the risk you are taking.

8. Gemini and RIAs - Gemini Earn was an ill-conceived product--a front-end pass-through direct to Genesis with ZERO recourse for Earn customers. And many of these customers were RIAs, as Gemini, Fidelity, and Eagle Brook attracted the most RIAs. It will be a long time before RIAs come back after getting burned here, and it remains to be seen how the inevitable in-court or out-of-court restructuring of Genesis and DCG will impact Gemini customers.

9. DCG/Genesis: When DCG/Genesis ultimately files for bankruptcy or restructures, this will likely be the last dip buying opportunity of the year. While algos will sell on bankruptcy news, the bankruptcy itself would actually tie up assets and could be structurally bullish for markets. We've written a lot recently about how all of this affects GBTC and ETHE, but ultimately, if you're a shareholder of either, bad news will be good news.

10. Shorting the Market Is Hard: If you haven't sold your tokens yet, what could possibly trigger you to sell at this point? It’s hard to believe any worse news could hit than what we’ve seen in the last month. Most selling pressure at this point largely comes from inflation and shorting, but shorting is really, really hard when you don't trust leaving collateral with exchanges or OTC lenders. As such, who is the marginal seller? It's a pretty safe call to say we're at or near the bottom, even if there aren’t clear positive catalysts on the horizon.

So, What Is the Upside Potential?: While I do think the bottom is in, I don't know what sends us higher. Like many, we’re thinking through the 2023 outlooks and trying to re-underwrite new themes. Check back in a few weeks for a deeper dive into the themes and narratives we’re bullish on for 2023.