Source: TradingView, CNBC, Bloomberg, Messari

The CCC-Rally Stalled

A few weeks ago, we talked about how the

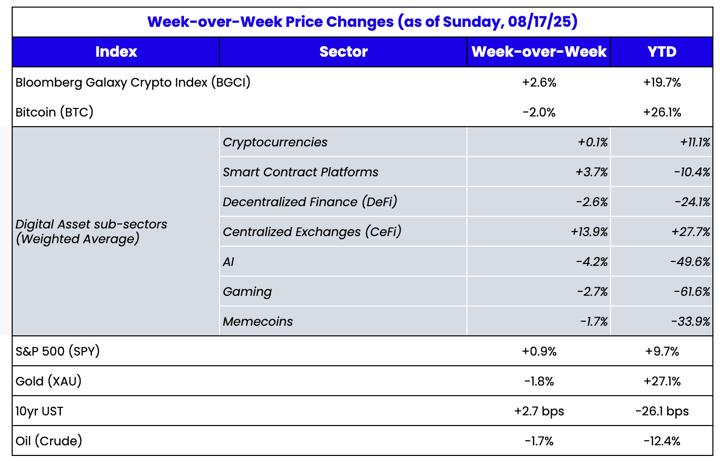

lower-quality assets were starting to rally, similar to a CCC-rated bond rally in the high-yield bond market. That stalled last week. Even though week-over-week crypto prices were mixed, the near 10% decline in both ETH and BTC from mid-month highs sent many memecoins and other low-quality tokens down 20-40% from their highs.

It’s actually amazing that BTC and ETH pulled back at all, given the inflows. From August 11th to August 15th, Ethereum spot ETFs saw a record weekly net inflow of $2.85 billion, marking a new all-time high. Bitcoin spot ETFs recorded a net inflow of $548 million during the same period, with BlackRock’s IBIT leading the pack with $888 million in net inflows.

While BTC and ETH have had strong YTD returns as a result of the ETF and DAT demand, as have some other large-caps (as captured by the CoinDesk 20 Indices – the top 20 assets by market cap), the CoinDesk 80 Index remains negative YTD (assets 21-100 by market cap), as has the equal-weighted CoinDesk Memecoin Index. Said another way, this is NOT an everything rally. A few large assets have captured all of the crypto excitement at the expense of others.

Source: Coindesk Indices

Everyone Wants to Have Their Own Layer-1

The race to control value capture in crypto is officially on. If you thought the Layer-1 wars were cooling off, think again. The latest entrants are the largest fintech and stablecoin companies in the world.

This week,

Stripe announced Tempo, an EVM-compatible blockchain designed specifically for stablecoin payments and enterprise adoption. Tempo’s goal is to build a chain optimized for cross-border settlements that Stripe can fully control. This comes on the heels of Stripe’s acquisitions of Bridge (stablecoin infrastructure) and Privy (crypto wallets), signaling their intent to own the full stack from payments to rails to wallets.

Hot on Stripe’s heels, Circle, the issuer of USDC stablecoin,

unveiled Arc, its own EVM-compatible L1. Arc is designed from the ground up around stablecoins, with USDC as the gas token, optional privacy features, and a built-in FX engine. Circle’s validator set will be permissioned, further highlighting that this isn’t about decentralization; it’s about efficiency, compliance, and margin capture. Arc is expected to go live on mainnet in 2026, but the intent is already clear that Circle doesn’t want to be a guest in someone else’s ecosystem anymore. It wants to own the house. This likely hurts Solana much more than Ethereum, as Solana’s stablecoin base is USDC-heavy (~80% USDC / ~20% USDT), whereas Ethereum’s is USDT-led (~37% USDC / ~63% USDT).

Earlier this year, Tether and Bitfinex

announced Plasma, their own blockchain initiative aimed at settlement and financial infrastructure. While details are still emerging, the positioning echoes the same theme: why remain dependent on external chains when you can control the rules, fees, and transaction flows yourself? For Tether, which already dominates stablecoin issuance, Plasma is a logical extension of its empire, one where it not only issues the money but also runs the rails beneath it. For Bitfinex, it further cements vertical integration across exchange, token issuance, and infrastructure.

As we argued recently,

Layer-1 blockchains are nearly impossible to value. That said, we made it very clear that these blockchains do have value, we just can’t figure out what they are worth. But nearly everyone has realized that infrastructure is the highest-margin part of crypto

. It’s no longer enough to be an app on someone else’s chain — the gravitational pull is to own the chain itself.

It’s worth remembering that none of this is new. Cosmos (ATOM) has been evangelizing “sovereign blockchains” since 2017, with the Cosmos SDK and the Tendermint consensus engine. Their pitch was exactly what Stripe, Circle, and Tether are chasing now - don’t rent blockspace on Ethereum or another chain, build your chain tailored to your application. Cosmos made this modular by offering plug-and-play components (consensus, governance, staking) while letting projects customize fees, tokens, and execution environments.

Some of the earliest vertical integrations in crypto came out of the Cosmos ecosystem. Binance Chain, dYdX’s new chain, Osmosis, and dozens of appchains were built using Cosmos SDK. These projects didn’t want to be apps competing for blockspace; they wanted to be sovereign ecosystems that captured more value from users, sequencer fees, and governance. Cosmos’ vision was that every company would eventually be its own Layer-1, which is exactly the shift we’re watching Stripe, Circle, and Coinbase pursue today.

In many ways, Cosmos was ahead of its time. Today’s wave of corporate L1s and appchains is simply validating the Cosmos thesis that customization and sovereignty are the endgame. The question remains whether the companies building Tempo, Arc, Plasma, and others will succeed in bootstrapping usage.

But not EVERYONE is building their own chain. There are counterexamples worth noting as well. Coinbase, for all its vertical integration, made a deliberate decision to launch Base as an Ethereum L2 instead of a new L1. Alignment with Ethereum’s liquidity, developer ecosystem, and credibility was deemed more important than starting from scratch. Similarly, Robinhood prioritized speed-to-market by building its new chain on Arbitrum Orbit. Both of these decisions reflect the trade-off - give up some control and theoretical long-term value capture, but gain faster deployment, credibility, and network effects.

It’s worth noting, though, that the goal is still to own the full vertical stack. At Coinbase, for example, on their Q2 earnings call, Brian Armstrong explained how Coinbase is integrating decentralized exchanges (like Aerodrome - AERO). Aerodrome will also be the destination DEX for Coinbase's ambitions to tokenize stock and other assets. The old model of Coinbase Exchange only generated an exchange fee on trading. The new model will allow Coinbase to benefit in three ways: Exchange fee, sequencer fee on Base (solely owned by Coinbase), and via a cut of the DEX fee (Coinbase Ventures is an investor in AERO).

The irony, of course, is that this cycle looks eerily similar to Web2. In the same way that Amazon and Apple built vertically integrated stacks to own distribution, hardware, software, and payments, crypto companies are now racing to build their own sovereign layers. Some will succeed, but most will underestimate the difficulty of bootstrapping real usage outside their captive ecosystems.

Whether it’s Stripe with Tempo, Circle with Arc, or Coinbase with Base and Aerodrome, the common thread is clear — everyone wants to move up (or down) the stack to maximize margin. But history tells us that network effects are stubborn, and building in isolation rarely beats building where the users already are. For every Tempo and Arc, there will be dozens of failures. The winners will be those who strike the right balance between control and ecosystem alignment.