What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

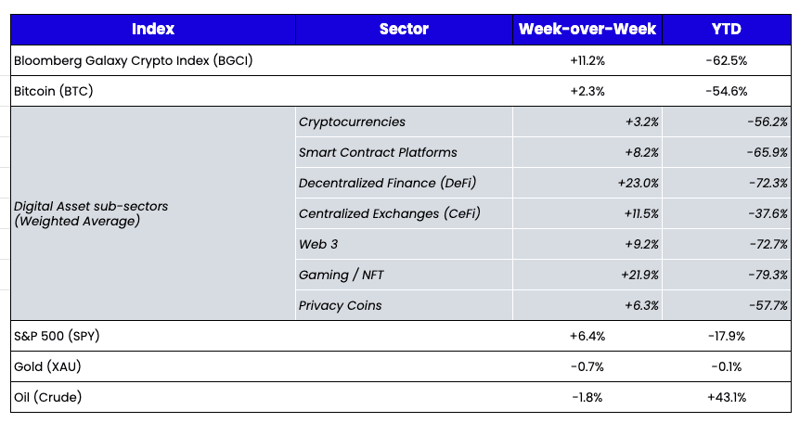

Week-over-Week Price Changes (as of Sunday, 6/26/22)

Source: TradingView, CNBC, Bloomberg, Messari

Don’t Call It a Comeback

What appeared to be the throes of despair were met with brave buyers on the dip. After back-to-back weekly losses of -5% for U.S. equities, the S&P 500 rose nearly +6.5% last week, while the Nasdaq gained +7.5%. And digital assets rallied as much as +20-30%, led by the most beaten-down sectors, DeFi and NFTs/Gaming.

The cynic in me would dismiss these gains as a “bear market rally” or merely short-covering, but the bull case is that DeFi protocols and applications did their job while their centralized exchange/lending platforms (CeFi) did not. That’s what led to the bounce in DeFi, which trickled down to the rest of the market.

- DeFi lenders Aave and Compound would not be able to misallocate assets and hide losses like Celsius did

- DeFi asset management protocols like Enzyme could not have lied about AUM and asset coverage like Three Arrows Capital did

- MakerDAO and its DAI stablecoin could not fail due to humans inadequately defending its peg like Terra Luna and its UST stablecoin did

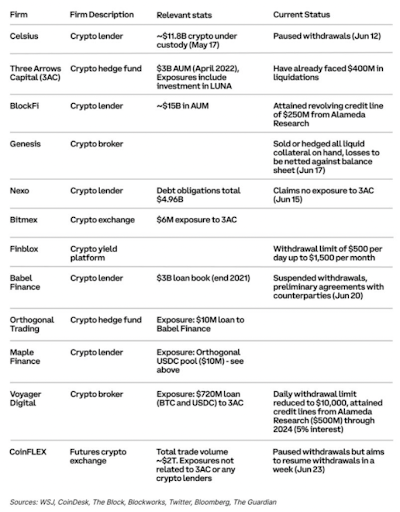

The carnage in the past six weeks has been very real, but every company that is currently facing solvency issues is a centralized company with a CEO, a board of directors, and human decision-makers. Not a single line of code from DeFi or a smart contract is capable of making the costly decisions that these companies made.

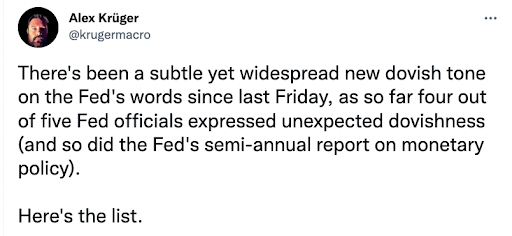

Source: Twitter

The bounce was further aided by positive signals across the global macro market. The Fed is still erring on the side of hawkish, but is now quietly opening the door to pivot when/if we get a recession or they need to step in to prevent a full-blown market collapse. This has helped the bond market rally off the lows and has sent the U.S. Dollar lower after bumping up against resistance.

In addition to a better macro backdrop, digital asset companies and projects are beginning to announce positive updates again after a 2- to 3-month hiatus, and the market is rewarding them.

- CZ at Binance said the worst is likely over, and Cumberland said something similar in an internal note to clients. Binance also announced a multi-year NFT partnership with Cristiano Ronaldo — BNB +9% week-over-week

- FTX began backstopping some of the riskiest lending shops (BlockFi and Voyageur) in a “loan-to-own” type trade — FTT +3% week-over-week

- MakerDAO (MKR) announced a $3M buyback and burn — MKR +14% week-over-week

- Galaxy Digital (GLXY) announced a buyback program of 10% of its outstanding shares — shares expected to rise on the open Monday

- DYDX announced moving its protocol from Starkware (Ethereum L2) to its own app-chain on the Cosmos IBC — DYDX rose +10% while ATOM rose +20%

- Axie Infinity (AXS) announced the Ronin bridge would be re-opening next Tuesday along with the launch of Land staking and an intent to repay victims of the Ronin hack on 6/28 — AXS +14% / RON +45% week-over-week

- Solana Labs revealed a mobile platform called SMS and an Android smartphone device — SOL +24% week-over-week

Without Reg FD rules requiring systematic updates, companies and projects are free to spit out news and updates whenever they want, and they often choose to hold these announcements back when the market isn’t in a forgiving mood. But the increased pace of positive news and a positive response from investors will likely lead to more of the same.

DeFi, Meet the Bond Market

While DeFi is having its breakout moment, investors in DeFi are struggling to generate yield as the widespread deleveraging is putting pressure on once plentiful yields. Perhaps these yield-hungry investors need to look at the bond market as an alternative. MSTR, COIN, and GLXY bonds all yield more than anything available in DeFi. For example:

- MSTR 0% converts due '27 @ $47 = 17% yield, with an extremely out-of-the-money call option attached via the convertible feature. MSTR has $2.4B of debt versus $2.6B worth of BTC on its balance sheet. Since the convertible bonds mature before the secured bonds, there is a high likelihood that these bonds will be refinanced at par.

- Even more egregious, GLXY 3% converts due '26 @ $68 = 12.75% yield plus an OTM call option attached via the convertible feature. GLXY has just $500M of debt versus $845M of cash and $2.2B of digital assets on its balance sheet, according to recent public statements and Arca estimates. Its equity ($1.7B) trades well below book value (~$3B), and the debt is covered 6x by assets! No wonder GLXY is doing a stock buyback.

- COIN 3.375% unsecured bonds due '28 @ $65 = 11.25% yield, while COIN 0.5% converts due '26 @ $61 = 14% yield plus another very OTM call option. COIN has $4B of debt covered by $6B of cash + $750M of investments (marked at cost) at Coinbase Ventures. In fact, COIN equity market cap is down to just $12B now. The market gives Coinbase zero credit for any of its actual business lines, so Coinbase might get a better ROI at this point doing what SBF is doing—buying tokens/other companies rather than running its core business.

When bonds with negative net debt and high asset coverage offer double-digit yields, smart investors will begin to divert some of their attention this way.

Developing Secondary Market Buyers

One of the biggest challenges to digital asset adoption has been a lack of secondary market buyers. Venture capital funds continue to demand most of the investment dollars, leading to many well-funded startups but few “growth equity” funds helping to take those projects to the next level. Retail investors are carrying the load until institutional investors show up. So how do we develop buyers of more mature projects? First, we must continue to educate—via blogs like this and other objective research that helps cut through the noise and focus on the depth, complexity, and valuation techniques of this evolving market. Separately, we could use more smart partnerships like the one between Bitwise and Multicoin announced a few weeks ago. In short, Multicoin is turning its VC portfolio into an index that FAs and other investors can purchase to help fuel growth. Skeptics would say this looks like a gimmick to help Multicoin “sell its bags,” but I believe this is a step in the right direction to develop secondary market interest. It’s still challenging to invest on your own, and for those who don’t have access to an actively managed fund, this is a good alternative.

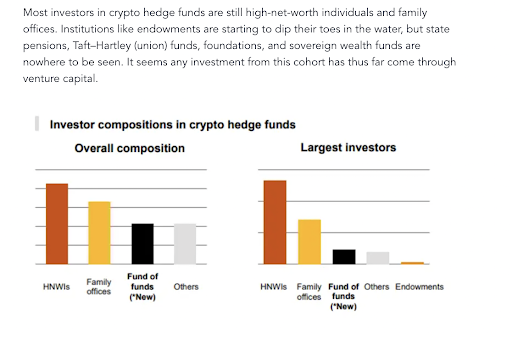

Additionally, both AIMA and PWC recently released reports about the growth of the digital asset hedge fund industry. AIMA noted that 1 in 3 “traditional” hedge funds surveyed are currently investing in digital assets, compared to 1 in 5 when they surveyed last year. And of those hedge funds that are invested in digital assets, 57% only have a toe-hold position with less than 1% of its total hedge fund AUM invested. Similarly, two thirds of those hedge funds (67%) that are currently investing in digital assets intend to deploy more capital into the asset class by the end of 2022. Additionally, 29% of hedge fund managers who are not yet investing in digital assets confirmed that they are in late-stage planning to invest or looking to invest. Meanwhile, PWC noted that adoption is still very low amongst institutional investors.

Between index products like Multicoin/Bitwise and new capital deployed to hedge funds, that secondary bid should develop quickly.

What We’re Reading This Week