What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

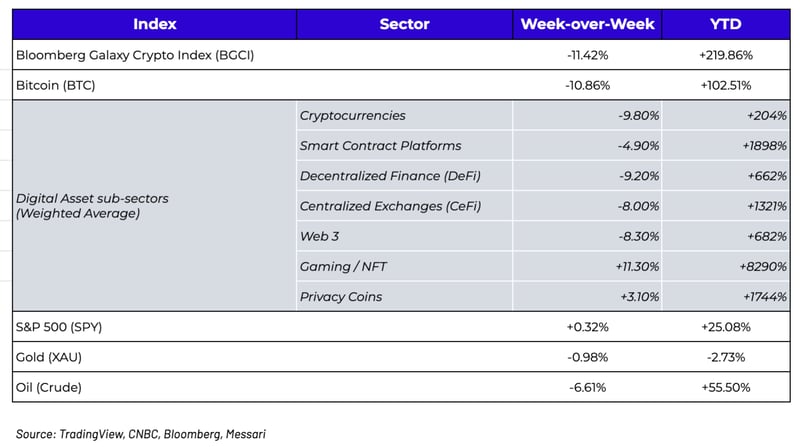

Week-over-Week Price Changes (as of Sunday, 11/21/21)

Source: TradingView, CNBC, Bloomberg, Messari

The digital asset market sold off because...because… it was just time to reset

It was a rough week for the majority of digital assets, as three-quarters of those in our coverage universe saw declines. Of course, that also means one-quarter of digital assets rose week-over-week despite Bitcoin and Ethereum falling over 10% each, once again shedding light on how diversified the projects in this industry have become, and how little reliance there is on large cap cryptocurrencies and protocols. While there were plenty of headlines last week, it was difficult to pinpoint a specific catalyst that warranted the steep decline. Across the dealer community, we heard a bit of the following rumblings:

- Continued concerns about inflation following the CPI print over a week ago

- The SEC rejected VanEck’s proposal to launch a spot bitcoin ETF

- Bitcoin’s Taproot upgrade (which leads to lower transaction fees and higher security) failed to drive upward momentum

- China continued its crackdown on miners

- Biden signed into law the infrastructure bill, which includes new legislation on how cryptocurrency investors report their taxes.

- The US Dollar jumped 2% to a 1-year high

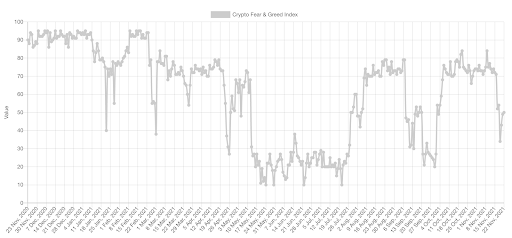

None of these seemed powerful enough by themselves to take the market over 10% lower, and in most cases are not even new information, which likely means the market just needed a healthy reset. However, it’s interesting to observe just how fast sentiment can change from “Greed” to “Fear” on the heels of lower prices… digital assets seem to take the stairs up and the elevator down.

In lieu of any specific digital asset news shaping price, it’s a good time to revisit the overarching macro landscape with which investors should be focused going forward.

Let’s Talk About Inflation

[Written by Arca Sr. Analyst, Nick Hotz]

The macro backdrop is front of mind for investors in the space following a scorching hot 6% CPI inflation rate in the U.S. and a correction underway in digital assets. So, let’s talk about inflation, or rather, let’s first define what inflation is not.

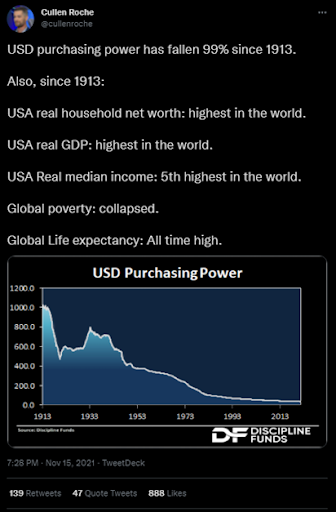

Inflation is not increasing the money supply or “printing money”. Inflation is a rise in prices of the things that matter to people, not some arbitrary measure of the monetary base that’s driven just as much by the banking system (both shadow and regulated) as it is by the Federal Reserve. There are a couple types of inflation – growth in the prices of goods/services and growth in the price of assets. While asset inflation is valid to worry about, it’s more of a longer-term problem concerning the future rates of return on risky assets in relation to their valuations. Although it’s much more difficult to measure than its counterpart, monetary policy actions such as Quantitative Easing explicitly attempt to, and generally succeed at, boosting asset prices by reducing long-term discount rates. This has positive effects for the economy in the near-term but more uncertain long-run implications.

The far bigger concern for most people is the price of goods and services - the cost of living, commonly measured by the consumer price index (CPI). And while there are some valid criticisms of CPI as a measure of inflation, primarily that it overstates, not understates true inflation (looking at you @jack), it remains one of the better measures we have for broadly assessing the cost of living in the U.S.

When it’s low and tame, inflation isn’t inherently problematic. On the contrary, it slowly and naturally reduces the strain on debtors at the expense of creditors, fostering greater credit creation and greasing the wheels of a productive capitalist system.

Source: Twitter

Issues start when inflation begins to erode real purchasing power. When this happens, inflation becomes an effective tax on the population, with the middle and lower classes hit hardest due to the greater proportion of their incomes spent on goods and services. This is exactly what we see today. After the huge positive shocks to average incomes because of government stimulus, inflation-adjusted incomes have declined precipitously from their highest levels, leaving many considerably worse off than they were just a few months ago. It’s worth noting that, counterintuitively, real incomes remain higher than they were before the beginning of COVID – a testament to the aggression of government stimulus efforts.

While some have tried to dismiss inflation while others have gone to the far extreme of calling for hyperinflation (sigh), the reality of course lies somewhere in the middle. The inflation we’re seeing today is real, has been persistent, and is hurting people’s pocketbooks. On the other hand, hyperinflation is not a real risk in a country that has an aging population, massive debt load, highly diversified and dynamic economy, and who controls the global reserve currency. It’s critical to recognize the current inflation as a problem without blowing it out of proportion so that we can be prudent in our policy choices and investment decisions.

Macro views going forward

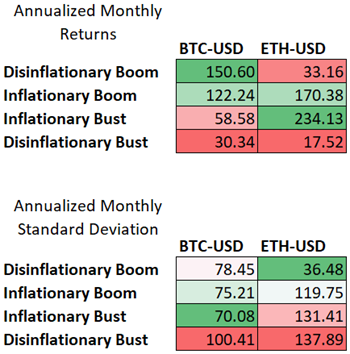

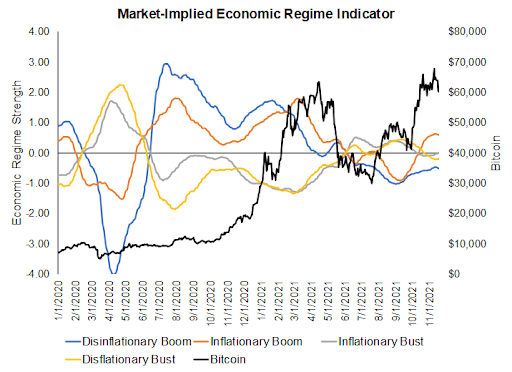

Growth and inflation are two of the most important drivers of many macroeconomic data and policy decisions. Historical backtesting shows that the rate-of-change in these factors is also the primary driver of the performance of major asset classes. By forecasting these rates of change, we can get a sense of where the market will probably trend going forward. We can classify these four possible regimes of the direction of these key macro variables.

- Disinflationary Boom (Growth Up/Inflation Down): Risk assets’ paradise. The best environment for equities, high yield credit, and some cyclical commodities.

- Inflationary Boom (Growth Up/Inflation Up): A pro-risk environment. Cyclicals in the stock market (energy, financials, materials, technology) and commodity market (crude oil and copper) outperform.

- Inflationary Bust (Growth Down/Inflation Up): Also known as stagflation. Gold tends to rise as real interest rates fall. While stocks (especially technology) can do well, this is not the optimal environment for equities.

- Disinflationary Bust (Growth Down/Inflation Down): Watch out. In a Disinflationary Bust, the U.S. dollar and Treasury bonds are the only assets that consistently outperform. This is where we typically see increased volatility, weakness in most stock sectors, commodities, and risk assets broadly.

Source: Bloomberg, Arca Internal Research

Source: Bloomberg, Arca Internal Research

Sources: Bloomberg, Yahoo! Finance; Data since assets achieved ~$10 billion market capitalization:

BTC-USD data since 1/1/2014, ETH-USD data since 5/1/2017

Since October, the market has shifted into inflationary boom territory, characterized by rising government bond yields and commodity prices and the outperformance of cyclical stock sectors such as energy, consumer discretionary, and technology, especially relative to defensive sectors such as healthcare and utilities. Such an environment is also historically highly positive for digital assets like Bitcoin and Ether.

Source: Bloomberg, Arca Internal Research

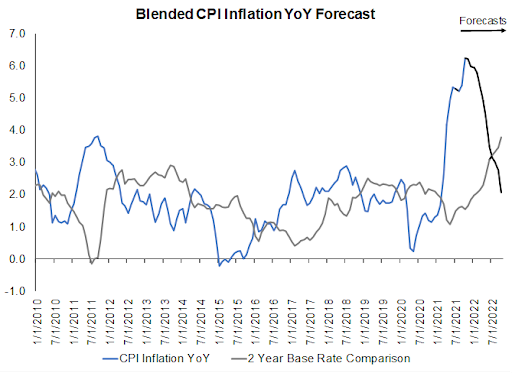

Using the forecasting technique of measuring base effects of year-over-year rates of change, we can get some edge on understanding where the economy, and thus the market, may be heading going forward. Broadly, given the future base rates of U.S. GDP growth and CPI inflation and the momentum markets are showing currently, we believe the inflationary boom could persist for another few months, with positive implications for digital assets.

However, we believe this will eventually give way to first a mild (Q1 2022), then moderate to severe (Q2) disinflationary bust. While inflationary booms have historically been favorable for digital assets, disinflationary busts are associated with increased volatility, lower returns and higher risk of crashes. Notable previous sharp busts include Q4 2018 and February/March 2020.

A dip into this risk-off quadrant doesn’t have to mean a crash in prices, with the mild disinflationary bust in Q2 2019 a notably good quarter for digital assets. However, the greater the magnitude of the slowdown, the more likely that risk assets, including digital ones, will suffer accordingly. Especially as we move into the second quarter, base effects of inflation are highly likely to be too steep to overcome and will lead to a decline in the rate of price growth.

Source: Bloomberg, Arca Internal Research

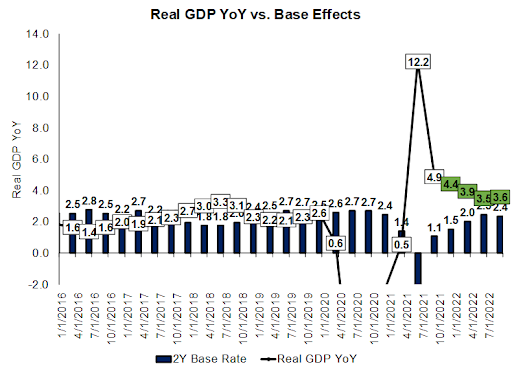

While the story isn’t quite as dire for growth, we still believe that after another few months of relative strength, persistently steepening base effects will pressure U.S. GDP growth lower over the coming quarters before finally easing up in the back half of next year.

Source: Bloomberg, Arca Internal Research

When looking to the near-term (next twelve months), we can use macro tools such as these to frame the economic backdrop and help drive smarter investment decisions. A few more months of economic momentum-driven tailwinds are likely to be followed by a tougher environment for digital assets and risk assets in general. Of course, it won’t affect ALL digital assets in the same way. Much like how defensive stocks will outperform growth stocks, certain sectors within digital assets will outperform others. As we go further out, the proverbial crystal ball gets more and more foggy as factors such as demographics and geopolitical events will drive economies rather than short-term fluctuations in macroeconomic variables. Over the long-term we can say with high confidence, to paraphrase Raoul Pal, that digital assets are the future of macro. For those taking a more fundamental view, figuring out what path we take to a specific outcome is nearly as important as knowing what the outcome will be – and that’s where some thoughtful macro analysis can aid in overall portfolio construction.

Digital Assets M&A, DAOs and Corporate Actions

Lost in the recent price action and macro overlays is how far this market has evolved in just a few short years. Remarkably, it was two-and-a-half years ago when we first publicly refuted some of the lazy narratives regarding whether or not digital assets had intrinsic value, introducing a few of the unique digital assets that had nothing to do with cryptocurrencies. Today, we’re still fighting some of these stale narratives, but anyone who has spent real time digesting this market knows it’s nearly impossible to lump all of the different types of projects and tokens into a single category. Moreover, the financialization of these tokens has every fundamental and event-driven investor on the edge of their seats. This financialization provides new ways to invest without worrying about the macro environment or market beta.

Just in the past few months alone, we’ve seen the following events, whose outcomes are completely separated from broader market moves. Some are more investable than others, but they are all unique events. While these topics deserve a separate, deeper dive, it’s worth highlighting the totality of these advancements in M&A, DAOs and corporation actions.

Buy backs: Two scenarios where the token is trading below book value, so governance proposals have been initiated to buy back tokens at a discount.

- FEI / TRIBE - A two-token algorithmic stablecoin model that had a rather catastrophic failure out of the gate in April 2021 has started an initiative to buy back $160M TRIBE using balance sheet assets.

- Nexus Mutual (NXM) - A decentralized insurance protocol with a capital pool consisting of ETH worth over $650 million is under-utilizing its assets, and has voted to buy back WNXM tokens at a significant discount to book value.

M&A: While there are still a lot of kinks to workout regarding what is actually being acquired, the idea of merging two protocols or chains is certainly worth monitoring.

- Gnosis (GNO) - the DeFi protocol known for its Gnosis Safe product (one of the most popular decentralized multi-sig solutions for dApp developers), proposed to merge/take over the xDAI chain in its governance forum. This move (if it passes) also places Gnosis squarely in the ‘layer 1’ club - potentially allowing for interesting products to be developed in a high throughput, low fee chain like xDai.

- Mango (MNGO) has an ongoing governance proposal to acquire the team from Psy-Options.

Restructuring / Private Equity DAOs

- PleasrDAO, which was created by pooling assets from a collection of professional investors in the digital assets space, acquired an NFT for a record $4 million, fractionalized the NFT, and sold the fractionalized units for a hefty profit. The original NFT was deposited into an on-chain vault, then fractionalized into 17 billion ERC-20 tokens called “DOG”, where 20% of these tokens were sold to the public via a 24-hour auction, drawing in roughly 11,000 ETH and causing the valuation of the underlying NFT to nearly triple. Both illiquidity and high unit prices have impeded retail investors from gaining meaningful exposure to valuable artwork, so this could be a meaningful innovation even outside the digital assets space.

- ConstitutionDAO grabbed headlines this past week as it quickly assembled over $45 million from 17k+ unique Ethereum addresses in an (failed) attempt to purchase a copy of the Constitution from a Sotheby’s auction. As Galaxy Digital wrote, “the idea for the project highlights the potential of Web3 technologies to revolutionize public ownership of private goods. It is also one example of a larger trend for using DAOs to collectively purchase and govern valuable items. As more DAOs are proven to be effective vehicles for decentralized organization, it is likely that fractional ownership of property and other types of private goods will also start to become more prolific in the mainstream markets.”

Governance Proxy battles

- [Republished from Galaxy Digital]: DeFi whales are fighting over control of DeFi exchange Curve.Finance (CRV). Curve has been a staple of the Ethereum DeFi stack since it went live in April 2020. With the Total Value Locked in the protocol exceeding $20bn, Curve holds over 7% of all liquidity staked on Ethereum dapps. But Curve’s dominance and its place as the hub for almost all Ethereum-based activity is just the tip of the iceberg for this stablecoin and ERC20 marketplace. DeFi aggregators StakeDAO and Yearn.Finance have vied for control of Curve via its governance token (CRV). Aggregators wanted to access the protocol’s revenue streams whilst also gaining power over the emissions of CRV, which are ongoing and reselected periodically. In return for depositing yield bearing liquidity into their vaults, Stake and Yearn offered better returns and auto-management of funds. While at first Yearn dominated Stake, the terrain of the so-called “Curve Wars” shifted when some Curve developers introduced their own dog into the fight: Convex Finance. Unlike Stake and Yearn, Convex locks CRV tokens deposited into its vaults forever. This means Convex’s own token (CVX) and the liquidity provider token for CRV deposits, cvxCRV became “symbiotic” with CRV revenue and Curve governance. Convex, in part due to its ongoing emissions and token architecture, has quickly overcome other aggregators to the point that Stake now delegates all of its assets to Convex while Yearn delegates a significant share of its tokens to it as well. Because Convex holds an outsized amount of CRV (~35%) in circulation and because he who controls Convex essentially controls CRV, major DeFi players, including the reserve currency protocol OlympusDAO, are now fighting for control of Convex in the hopes of gaining direct control over the liquidity, revenue, and flow of stablecoins within the Ethereum protocol. Bottom line: parties within the ecosystem want to control the organization’s present and future, capturing future revenue and defending against would-be competitors. Decentralized organizations like Olympus are now using those moats (and protecting them) to secure revenue and, most importantly, capture and control liquidity. In an industry that prides itself on having open, composable, transparent, and neutral platforms, the Curve Wars show how groups can align to compete in an extremely free market and turn the design space into a battle zone of powerful interests

These are just a few examples of the financialization happening in digital assets today, where financial outcomes can be modeled using traditional event-driven and fundamental techniques. We’ve come a long way from the “cryptocurrencies are pure speculation” camps.

What’s Driving Token Prices?

- Arweave (AR) dropped -9% despite Arweave storage now natively available in Polygon through Arweave's Blundr Network. This is a partnership with Polygon that gives users access to Arweave's network as they plug their storage solution to be "universally accessible across all platforms with any tokens".

- Polkadot (DOT) gained +2%. Polkadot’s first parachain auction was November 11th-18th with DOT increasing +22%. Acala won with 32M DOT staked; as a result, 1.2B of DOT was taken out of circulating supply. The second parachain runs November 18th-25th with similar results expected.

- Sandbox (SAND) gained +42% after Sandbox's alpha version of the game was announced with a release date on 11/29 and will run until 12/20. SAND's metaverse will be progressively opened over Q1/Q2 2022 with LAND owners who have built high-quality experiences and through the launch of the DAO with staking and voting mechanisms for SAND, LAND and AVATAR holders.

- AAVE fell -5% even as Aave launched Aave Arc, Aave's institutional offering. Aave Arc provides an isolated Aave market and a sandbox environment for institutions to experience the power of DeFi: transparency, decentralized governance, rapid innovation, automated smart contract-based execution, liquidity, and programmability.

What We’re Reading This Week