What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

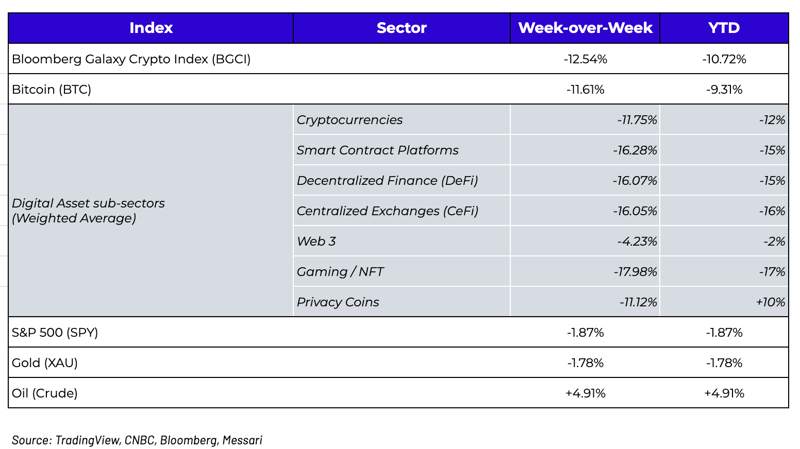

Week-over-Week Price Changes (as of Sunday, 1/10/21)

Source: TradingView, CNBC, Bloomberg, Messari

Here We Go Again – Overreactions to Macro

When we last wrote an update before the end of the year, we suggested that a strong digital assets rally was in play for the back half of December and into January. Suffice it to say: we were quite wrong about the Santa Claus rally and subsequent January effect. December was a brutal month for digital assets and equities tied to digital asset companies; the start of the new year has arguably been even worse.

Based on this somewhat unexpected finish/start to the year, it’s not surprising that the “digital assets bull market is over” chorus has grown quite loud recently. But what exactly is the bear thesis? We’ll get to that, but first, a rehash of similar conditions six months ago. Back in June 2021, during the peak of digital asset investing despair, we released our “Debunking the bear theses” report. In it, we systematically refuted each of the bear theses that we’d been hearing—and there were quite a lot at the time (some more nonsensical than others). While it was ultimately about three weeks too early to say that we officially called the bottom of the market, we were pretty close. As expected, all of the individual bear theses were slowly rebuffed over the next six months. Today, the bear theses seem to be a lot more concentrated. Essentially, many digital asset investors are becoming increasingly negative because they fear a 2018-redux (which is ridiculous given how different today’s market growth is relative to what existed in 2018), or because they think the Fed’s pivot will kill all risk assets indefinitely (which implies that a long, drawn-out Fed withdrawal will immediately and persistently crush all risk markets). Both of these arguments seem incredibly shallow and dismiss the complexity of the digital assets industry.

So let’s start with macro. Last Wednesday’s release of minutes from the Fed’s December policy meeting triggered anxiety that rippled across global markets. In short, the minutes were hawkish but were largely in line with what had been communicated by the Fed over the past two months. The biggest difference was simply the increased speed with which the Fed is now expected to begin raising rates and shrinking the balance sheet (timetable accelerated by roughly three months)—as such, the first week of the new year resulted in heavy selling of growth stocks, a rotation into value stocks, a steep rise in long-term interest rates (curve steepened), and a sharp decline in digital assets. Again, the information was not entirely new, but investors were caught off guard by the forcefulness and level of consensus shown in the minutes.

Naturally, the Fed’s new timetable coupled with a bearish response by the markets led to many macro investors salivating at the chance to call the global risk asset bull market over. In essence, their argument boils down to:

Basically, we’re back to macro investors saying “it’s all one trade” – long bonds, long tech stocks, long private equity, long VC, long digital assets—and it’s now over as yields go up and the Fed’s balance sheet goes down. As Chris Solarz at Cliffwater put it in his weekly newsletter, “The market’s ‘Buy-The-Dip’ mentality, which used to be tactical, but by now has become a Pavlovian reflex, will probably trap many once the ‘Fed Put’ is retired due to inflation concerns.”

This all sounds so simple and certainly was true for the past week, but here’s the problem: sure, the headline warrants a price reaction (and got one), but this will be a drawn-out 2-3 year process of quantitative tightening and rate rises. It’s highly unlikely that markets will continuously react to the same news over and over. Three rate hikes in 2022 will take us to a 1% interest rate by the end of 2022. And while inflation is currently above 6%, the rosiest predictions have inflation falling to 3% by the end of 2022, which means real interest rates will be between -2 and -5% one year from now. That is not what hawkish typically looks like.

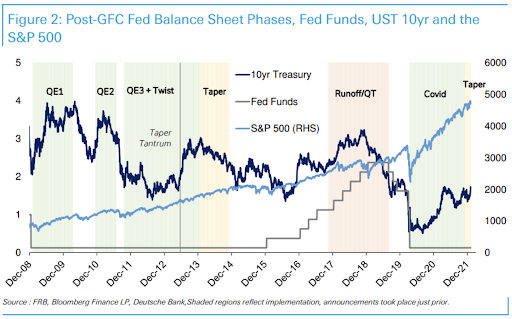

Moreover, in just a few charts, we can show why the Fed rate hike cycle, including quantitative tightening (QT), is likely not bearish at all for digital assets or equities in the near term. The last time hawkish Fed statements caused a market meltdown was in 4Q 2018 when the S&P fell -7% in October and another -9% in December. Note, this was after 2 years of rate hikes from 2016-2018—a stretch when equities and digital assets rallied throughout the hike period and only began to fall at the conclusion of the program when the market thought the Fed had gone too far. The -23% equity tantrum in 4Q 2018 led to Powell sharply pivoting on continued Fed hikes in January 2019, and instead, the Fed ended up lowering rates again, which ultimately kicked off yet another bull market. In essence, both rate hikes and QT from 2016-2019 hardly had any impact on equities or digital assets overall, and while bond yields initially rose during QT, they rallied hard during the second half of QT and into Powell’s pivot.

Going back even further, the Fed last raised rates over a 2+ year period from June 2004 to July 2006, and the equity market again rallied the entire hike cycle until finally selling off at the end of the hiking cycle in mid-2007 (when the Fed was actually lowering rates again), which culminated in the 2008 Lehman/Bear-led depression.

Source: Trading View / Fred

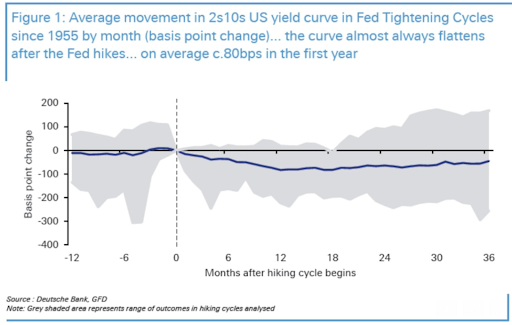

Finally, in what might be the most important indicator, the Treasury curve actually steepened last week. Historically, the 2s/10s curve almost always flattens after the first rate hike by an average of 80bps over the next 12 months, and a recession then typically occurs around 18 months after the 2s/10s inverts. So it’s likely that we’re approximately 30 months away from a recession.

As Deutsche Bank’s Jim Reid put it, “It seems that the age of ultra, uber, ludicrously loose monetary policy is coming to an end. It's inevitable markets will be impacted.” The timing is open for debate, though; the Fed raising rates and withdrawing liquidity is not what causes big, long-lasting market selloffs—it’s not until many years after very long Fed hike cycles when markets typically face sustained declines. There’s simply not a lot of evidence to support sustained lower prices of risk assets today, and it is highly likely that 2022 is another banner year for many digital assets, given the growth trajectory. Since the bear case currently stems overwhelmingly from unscientific assessments of when "money printer stops going brrr," we believe this fear will likely subside like it did in mid-2021. If digital assets fall meaningfully this year, it's not going to be because of the Fed.

Next, let’s look at 2018 PTSD. It’s no secret that 2018 was an awful year for digital asset investing—one that scarred many investors. Most of today's fear (and quite frankly the fear seen during all six of last year's 20%+ drawdowns) comes from a fear of "cycles"—that the current bull cycle is over and the 2018-like bear cycle is right around the corner. This is the easiest one to debunk, largely because it is based on a sample size of one, which is not at all statistically relevant. The characteristics of the 2018 bear market don’t even remotely resemble today's market. The assets, types of investors, infrastructure, and traction are all vastly different. Every single digital asset event pre-2020 is simply irrelevant. No projects other than Bitcoin, and to some extent Ethereum, had any traction pre-2020. Now we have four legitimate use cases built on blockchain (Stablecoins, DeFi, NFTs, and gaming—with Web3 applications coming fast). A look at the top tokens at the end of 2019, or the end of 2018, shows just how ridiculous any comparisons to that era are. These tokens are a “who’s who” of dinosaurs that never had any traction or applicability—and still don’t.

Now compare that to today, when the Block had to release a 163-slide report just to show off all of the incredible growth metrics from different areas of the digital asset industry, which includes:

- Stablecoin supply grew by 388%—from $29 billion to over $140 billion

- M&A volumes surpassed $6 billion, a 730% increase year-on-year

- DeFi TVL skyrocketed to over $250 billion, representing growth of over 700%

- Decentralized exchange (DEX) volume grew 522% year-over-year

- Wallet growth, with 170 million Ethereum unique addresses, is up 300% year-over-year

- Total NFT volume traded stood at $8.8 billion, compared to negligible volume the year before

- 18,000+ monthly active developers commit code in open source crypto and Web3 projects

- 34,000+ new developers committed code in 2021—the highest in history

- 4,000+ monthly active open-source developers work on Ethereum, 680+ open-source developers work on Bitcoin

In 2022, actual growth will trump hype, which was all 2018 was based on.

Finally, let’s look at dispersion. Even if we’re wrong, and the Fed does impact equities and Bitcoin faster than we anticipate, this notion that all other digital assets will fall just because Bitcoin falls is incredibly outdated. This is no longer a single-attribute asset class but rather a technology that underpins all asset classes. Thus, some sub-asset classes will do well while others will perform poorly, and that is a healthy dynamic that makes it nearly impossible to have a 2018-style "winter". We may continue to have steep, quick, highly correlated corrections, but certain assets and sectors will bounce back faster and stronger than others.

The correlations between digital asset sectors have been going down for years, and the price dispersions have widened. In 2021, for example, correlations spiked in each of the six 20%+ Bitcoin drawdowns, but each drawdown led to different market reactions during the recovery. Over the 365 days alone, Bitcoin is now completely flat, Defi has been in a bear market, Layer 1 protocols and NFTs/Gaming have been in a raging bull market. Even just this past week, while most of the market declined on low volumes, we continued to see rotations as Fantom (FTM), Atom (ATOM), and Near (NEAR) all rallied in the face of broader market declines. The rest of 2022 will likely yield something similar--where we have a bear market in some sectors and a bull market in others. A few weeks of high correlation due to market panic does not invalidate sector dispersion and lower longer-term correlations.

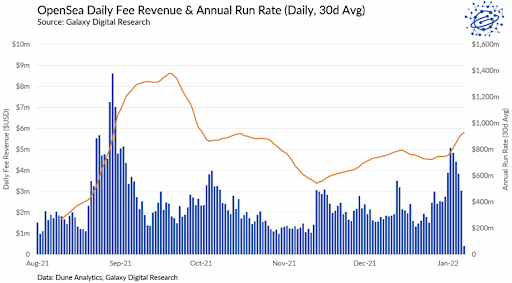

So consider us very bullish in certain sectors and pockets of digital assets to start 2022, and happy to see a nice unexpected discount with which to invest. It’s also worth noting that the popular “Crypto Fear & Greed Index“ has been indicating "extreme fear" at these levels (even though vol markets are telling a different story), which we haven’t seen since the last market bottom in July 2021. And if that’s not enough, July 21st was the day OpenSea announced a large raise at a $1.5 billion valuation, which helped stop the summer 2021 selloff and sparked the 2nd half 2021 rally. Just this week, OpenSea announced a whopping $300 million raise at a $13.3 billion valuation. It’s hard to get too bearish when you see growth like that.

A Ronin (RON) Case Study Shows Why Active Management is Dominating

One of the most mispriced tokens is about to launch any day this month, and it’s a trend that will likely continue because there are no underwriters in digital assets.

In a typical debt or equity new issue, an investment bank spends weeks or months trying to determine an appropriate price to anchor investors to and determines where demand will equal supply. Occasionally, this underwriting process is dismissed in favor of a direct listing, but in that case, there is still typically a bevy of sell-side and buy-side research that helps investors assess fair value ahead of listing; market makers heed this knowledge before setting initial prices. While the process isn’t always foolproof, there is at least a lot of thought that goes into the pricing of new assets. But in digital assets, we consistently see tokens listed by both DEX’s and major exchanges at prices with no thought at all to fair value and no research to help their clients determine whether to buy or sell.

Sometimes this is a disaster for new investors, where market makers, complicit exchanges, and early VCs should be ashamed of themselves for fleecing retail investors with egregious prices that have no chance of holding (see ICP, ALGO’s 2019 dutch auction, or just about every listing thus far on Copper). However, it can also go the other way, which we’re likely to see with Ronin (RON).

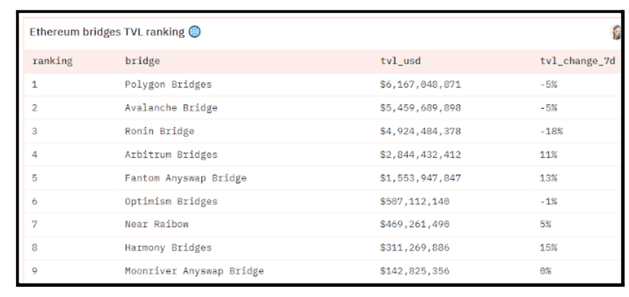

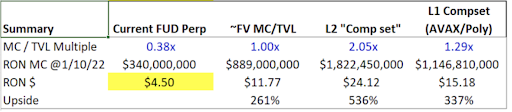

Ronin (RON) is the governance token for the Layer 2 sidechain of the Axie Infinity ecosystem. This is, in our opinion, the first notable Layer 2 token, giving it a first-mover advantage in the TVL wars. Ronin’s $5 bn of TVL puts it as the top-ranked L2 and #3 overall behind L1s Polygon and Avalanche. Looking just at its DEX (Katana), TVL is still $1 bn. The total bridge TVL is nearly ~2x Arbitrum’s TVL despite Arbitrum supporting dozens of Dapps (Uni, Sushi, Aave, etc.)

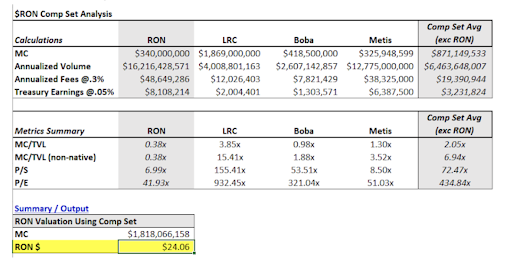

To date, the RON token can only be farmed by providing liquidity on the Katana DEX in two pools (SLP/ETH or AXS/ETH), meaning current AXS and SLP holders are earning RON rewards, and eventually, the token will be released to the market and listed on exchanges so that new investors can buy it. Had the RON token been underwritten or had any scrappy firms written research about RON, they would likely be guiding this token towards $24, conservatively, given comps:

Source: Arca Estimates

Despite the fact that RON will likely be a $1 bn market cap eventually and is part of the $10 bn+ AXS / Sky Mavis ecosystem, not one dealer or buy-side firm has written any research on Ronin or tried to quote “when-issued” RON markets. As such, the token will just eventually “come to market” with no guidance to set expectations. Recently, FTX listed a RON perpetual futures contract ahead of the RON token launch, and while volumes are too low to take this price at face value, it will likely frame the pricing of the new RON token. Using that price of $4.50, which is based on nothing other than where market makers decided to set it, you can see just how cheap this token will be to fair value.

If you believe in fair and efficient markets, the market will eventually get the price of this RON token right. And if we’re right, it will generate great returns for investors who spend the time to do the work on this token. This is where alpha comes from and why most actively managed funds in digital assets are outperforming passive investment strategies by a country mile. The ability to identify, source, and understand tokens like RON—while understanding and avoiding tokens like ICP without any help or guidance from the “sell-side”—is what separates the professional asset managers and hard-working, research-minded individuals from those who are simply trading digital assets as a hobby.

There are, of course, regulatory reasons for why many dealers refuse to get into the underwriting or research game. We anticipate investment bankers entering this space in the next several years. But in the meantime, it’s a guessing game for most investors looking at new tokens for the first time.

What We’re Reading This Week