What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

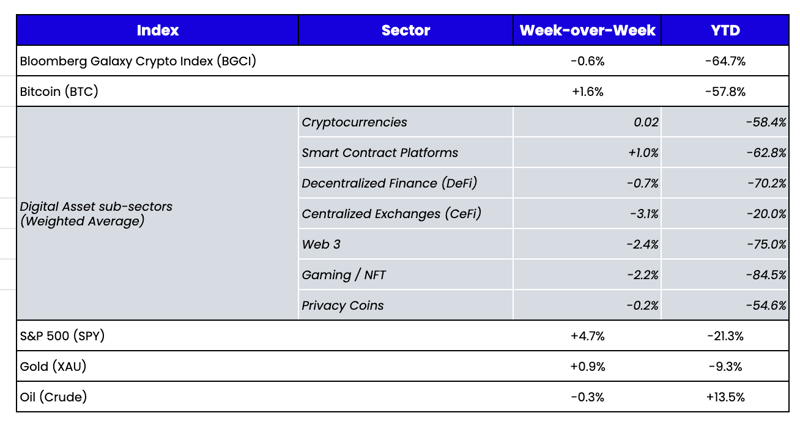

Week-over-Week Price Changes (as of Sunday, 10/23/22)

Source: TradingView, CNBC, Bloomberg, Messari

Global Coordinated Central Banks

Yields on 10-year U.S. government bonds had risen almost 70 basis points in October heading into Friday, from 3.65% to start the month to almost 4.30% on Friday morning. Amidst this fast rate ascension and subsequent U.S. dollar explosion, the Bank of England was forced to step in to support the Gilt market, and the Bank of Japan continues to intervene to support the Yen. It was only a matter of time before the Fed’s game of chicken came to an end as well.

Right on cue, Fed puppet and Wall Street Journal reporter Nick Timiraos finally put on paper what most market participants had already agreed upon: the damage the Fed has inflicted has gone too far and needs to be slowed down. I read this report as an acknowledgment from the Fed that they have to stop breaking global markets, but they can’t explicitly say they are going to pivot because that would give the equity market the satisfaction that the morally hazardous “Fed put” is still in play. As a result, the Fed will still try to talk tough but is ultimately preparing markets for the inevitable dovish pivot. The market agreed, with a violent bond rally and a large move higher in equities. What is now universally believed to be the last 75 bps hike is a few weeks away, as the market believes we’ve hit peak rates.

Now, this, of course, doesn't mean markets are entirely out of the woods. But it does allow investors to go back to picking winners and losers rather than style drifting their way into macro playbooks. Further, while higher absolute rates ultimately make some investment strategies more difficult (like arbitrage and financing LBOs), it opens the door to other opportunities. For example, certain long/short trades become more attractive when you can offset the negative carry of your short with the positive carry from higher-yielding bonds.

One place where this is playing out is in stablecoins. Tether (USDT), the leading U.S. Dollar stablecoin, has always been a popular short amongst tourists who don’t believe the stablecoin is fully backed. Regardless of the probability of success, the risk/reward is undeniable and getting more attractive. Tether trades at $1 and cannot (in theory) go above $1, but if the U.S. dollar peg breaks and there aren’t enough liquid assets to redeem, USDT can be worth fractions of its perceived value. Borrowing USDT for 8-12% and shorting USDT was difficult when rates were sub 1%, and IG bonds traded at 3%, but with Treasuries at 4%, IG bonds at 7%, and HY at 10%+, offsetting the 10% negative carry with high yielding longs has become more palatable. And that’s exactly what we’re seeing across digital asset dealer desks. Demand for USDT has increased (especially from TradFi investors), and thus lending rates have increased while short interest has risen. This does not mean that Tether is riskier today than usual; quite the opposite,

in fact. Further, Tether keeps the interest it earns on its float, and with short-term rates around 3%, the $68B of cash now earns well over $1B per year in interest. Fundamentals are stronger just as financing a short becomes easier.

Aptos, SBF, and a Lack of Transparency All Come Into Focus

Co-Written by Hassan Bassiri, CFA — Arca Portfolio Manager and Analyst

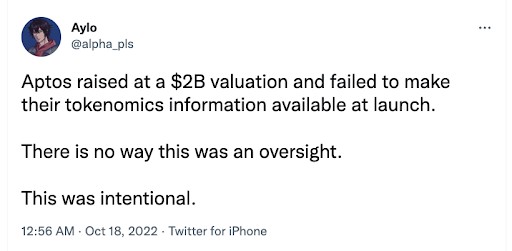

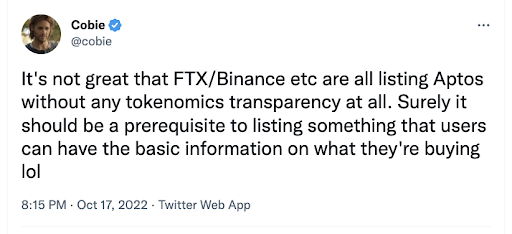

Aptos launched its highly-anticipated mainnet on Monday. However, the release drew plenty of skepticism. Developers of the Meta (Facebook) blockchain project Diem created Aptos, which was billed as a “Solana Killer.” This project has already been plagued by inconsistent communication (freezing of the Discord community communications channel) and significantly low transaction throughput in just a short week. But more importantly, it has been a lightning rod for criticism against VCs that continue to fund digital assets projects at wild valuations with favorable unlock schedules allowing them to sell quickly into retail and the digital asset exchanges that serve and enable this VC community. Worse, it’s hard to distinguish the two in many cases, as the overlap and conflicts of interest are plentiful.

- The blatant conflict of interest and overlap between the biggest investors and the exchanges listing the token.

- The intentionally vague and ambiguous tokenomics.

Aptos raised ~$350M from a cohort of investors, including FTX, Coinbase Ventures, and Binance (as well as a16z, Multicoin, and Jump). Not surprisingly, on 10/19/22—just 1 week after the token generation event—the APT token was listed on FTX, Coinbase, and Binance. It is uncommon for any exchange to list a token that quickly—well before the token has any functionality, utility, or demand—let alone by 3 exchanges widely considered premier "Tier 1" exchanges. Even more egregious, none of the tokenomics were available until less than 24 hours pre-listing. And still, the information published at the last minute left plenty to be desired. The Aptos Foundation tweeted that a more comprehensive explanation would be distributed soon, but what do we know now? Very little.

Of the 1 billion total supply (breakdown below), only 13% is considered circulating. Presumably, the 2% airdrop (~20 million) to testnet users is part of the ~125 million Community tranche designated for ecosystem-related items such as grants, incentives, and other growth initiatives. Beyond that, we have no clue about the actual float. Does the 2% airdrop comprise the entire float (excluding tokens given to market makers)? Will the Foundation sell tokens into the listings to diversify its treasury? How many tokens will be distributed to ecosystem projects from the initial 125 million, and what's the timeline for that distribution?

Additionally, the “lockup” is hardly a lockup at all. While investors and core contributors don't vest for at least a year, both vested and unvested tokens can be staked to earn yield (7% annual), and these staker rewards vest and can be sold immediately. Further, there was a 1-week pre-mine before the token generation event. At an 80% stake rate, the Foundation and Community earn another ~60 million tokens annually, but there are no details on distribution mechanics. By now, it should be clear that these tokenomics are too ambiguous to be useful to anyone. They are downright predatory for retail investors trading the new APT token on exchanges without the means to uncover further information.

“Earlier this year, The Internet Computer finally released its token, which, on a fully diluted basis, was the third-ranked digital asset by market cap behind just BTC and ETH. With no usage, no transparency, and an insane $200 bn+ valuation, ICP proceeded to fall 94% from mid-May to the end of June, crushing investors and triggering well-reasoned criticism. Furthermore, in response to a Twitter question, Dominic Williams, CEO of the DFINITY Foundation, indicated that there was no vesting schedule for treasury tokens. Meanwhile, CoinList and crowd sale participants, typically smaller retail investors, were given either a 12-month vesting schedule or a ~4-year vesting schedule (49 30-day installments). This is not industry best practices. ICP did not release a consistent supply schedule, there is no vest on treasury tokens while there is on retail participants, they transferred tokens to numerous exchanges, and they continue to offer no transparency. Worse, the exchanges themselves did nothing to help new buyers of ICP understand these issues. While they may claim that they simply provide a platform and not an underwritten investment banking service, it is pretty clear that most would have avoided this ICP token had any of this information been known. Similarly, where are the numerous prominent Venture Capital firms who funded DFINITY pushing for change and increased transparency? Both groups are just as much a part of this industry as everyday crypto native users are. The buy-in needs to come from everyone. Not surprisingly, ICP has massively underperformed over the past few months even as other Layer 1 protocols have rallied.”

What's more telling—and hypocritical—is that the same exchanges listing the token—FTX, Coinbase, and Binance—are asking the SEC for more regulatory clarity. Huh? It's disingenuous to publicly appeal to the SEC for clear rules protecting investor rights while providing listing support for a project that lacks transparency and disclosure detail. Exchanges that have an investment arm have a clear conflict of interest and should be held to a higher standard independent of regulation.

With this in mind, it’s not surprising that Sam Bankman-Fried is starting to take the heat (lots…

of…

heat—lots) for his recent proposal regarding digital asset regulation and new industry standards.

On the surface, SBF has earned his stripes and his reputation; it’s nice that he is using his large platform and influence to try to enact change. He didn’t ask to be the market’s de facto leader, but he has become one and is rising to the challenge. But, on the other hand, the constant hypocrisy of begging for change while you are one of the biggest beneficiaries of the current “no rules” environment is a bit hard for some market participants to stomach.

Change is coming no matter what, and it's essential to have the leaders of this industry push for that change in responsible ways. But it’s also not too much to ask that they self-police. Perhaps if they played by the rules they expect before explicit rules are put in place, it would lead to more favorable regulation and a community less divided.

Source: Twitter

Source: Twitter Source: Twitter

Source: Twitter