What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

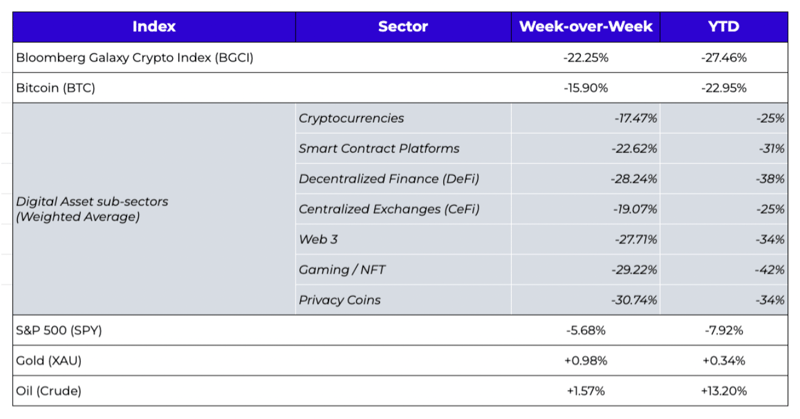

Week-over-Week Price Changes (as of Sunday, 1/23/21)

Source: TradingView, CNBC, Bloomberg, Messari

A Brutal Week

As usual, there are now calls for complete collapse. However, current positioning doesn’t really point to that. The beauty of a closed ecosystem with data transparency is that it’s pretty easy to tell when money is leaving the ecosystem versus just temporarily fleeing the assets; right now, it’s the latter. For example, stablecoin supply isn’t decreasing, nor are stablecoin balances on exchanges, indicating that money isn’t being withdrawn from the system. Instead, it is sitting there in cash, waiting for better entry points back into the same assets that were just sold. There were no value investors in prior, longer-lasting bear markets, and many participants legitimately thought digital assets might die and never come back. Today, capital is sitting on the sidelines just trying to figure out when to buy back in. Until that money leaves the ecosystem, it is supportive of asset prices. In the meantime, it is being used as collateral to short tokens, and some of it is even being used to buy NFTs (NFT volumes and floor prices of top projects have been much more immune to the selling pressure).

Most investors we speak to know this drawdown is temporary; the disagreement lies in how bad it can get first and how long it will take to recover. In the meantime, new entrants keep on coming. Still, for now, the entire digital asset market is simply a pawn in U.S. monetary policy.

The Storm Before the Calm

[Written by Arca Macro Research Analyst Nick Hotz]

While a nearly infinite number of components drive global markets, most can be summarized by two key factors: the addition/removal of liquidity and the acceleration/deceleration of the economy. Risk markets like it when liquidity is added to the system because it reduces bid/ask spreads and creates buying flows. They also like it when the economy accelerates; it boosts corporate profits and creates wealth effects, driving further capital into assets. When the opposite occurs, bad things tend to happen to risk assets. Fear of precisely that outcome is what catalyzed Thursday and Friday’s capitulation.

While digital assets may be the newest kid on the block, experienced macro traders know that no asset class is immune from these mega factors. An enormous amount of liquidity has been injected into the system in recent years, both direct—in the form of credit creation from global governments responding to the coronavirus pandemic, as well as lending from commercial banks from the recent economic boom—and indirect reserve creation from global central banks purchasing bonds to reduce long-term discount rates. At the same time, on a rate-of-change basis, the economy has boomed as it came out of the deepest and fastest depression in modern history. However, the winds have recently shifted from that overwhelmingly positive backdrop towards a more muddled one, and soon, one that is entirely the opposite of what we’ve experienced in recent years. On the other side of this shift, we’ll likely see a sharp pivot towards a more favorable environment again; one that could leave many investors sidelined and unable to reenter the new bull market. But before that, we must weather the storm.

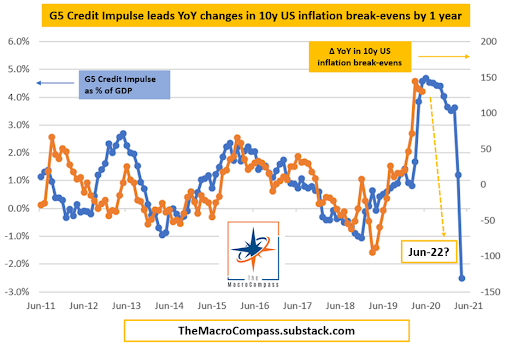

Fiscal Impulse Drying Up

After trillions were injected into the system by governments to fight the pandemic’s public health and economic impacts, authorities now need to be more constrained following rampant inflation in response to supply chain shocks, cash stimulus and fiat currency debasement. Since economics is all about rate of change (e.g., we look at GDP or CPI in terms of annual or quarterly change), we need to focus on the change in stimulus to understand what’s relevant to markets. After the massive fiscal injection over the past year, global governments will be highly unlikely to pony up sufficient amounts to reach the same spending levels as last year, especially in the wake of the highest inflation rates in decades. Even if they manage to pass a few stimulus measures, most of the spending will be pushed into next year or later without a significant impact to the overall credit impulse today. Today, that leaves us with the largest net global fiscal draw we have seen in at least a decade, and likely in modern history.

Source: The Macro Compass

As shown here by Alfonso Peccatiello, that drawdown has significant negative implications for inflation (and indeed the economy more broadly) over the coming months.

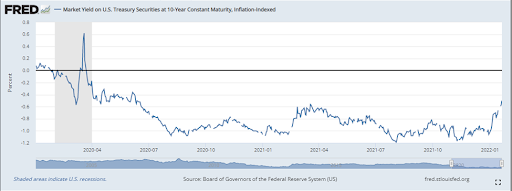

Source: FRED

The chart above may be the most important chart for digital asset investors, but hardly anyone is watching. The real yield on U.S. Treasuries is essentially the world’s discount rate—the after-inflation rate at which investors modify future cash flows to bring them into the present to help value assets. Among myriad other reasons, the main reason many digital assets are so risky is that, like technology stocks, their future cash flows are mainly probabilistic and relegated to the far future—if they have cash flows at all. One could even argue that the value of an asset like Bitcoin is entirely a function of discount rates since the decision to hold Bitcoin entirely depends on the expected debasement (rising discount rate) of fiat currency. Thus, when discount rates rise…

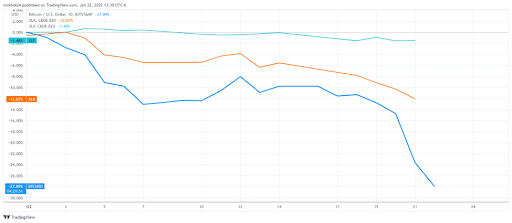

Source: TradingView

…digital assets and other long-duration assets like tech stocks get smoked, while cash-flow-plentiful consumer staples barely bat an eye. The spike in real yields to their highest levels since mid-2020 was a major driver of the selloff we’ve seen. There is, of course, nuance with digital assets, primarily due to a lack of education across retail and new professional investors. Many digital assets should behave more like consumer staples than profitless tech companies due to the high revenues and cash yields, but the market doesn’t seem quite ready to draw a distinction between tokens of recession-proof gaming companies (e.g. AXS) and high cash flow exchange companies (e.g. FTT, SUSHI) versus protocols with no cash flows (e.g. BTC) or early-stage products with little fee generation (e.g. SOL, AVAX). The jump in yields has been driven by increasing concerns about a hawkish Fed, now with nearly five 25bp rate hikes priced into 2022 (hiking rates to 1.25-1.50% from 0-0.25% by year-end), along with expectations for the ~$120B of monthly additions to the balance sheet to transition to a net draw of $50B—a -$170B change/month.

Source: Andreas Steno Larsen

This expectation of tighter policy pushes real yields higher and forces investors to reevaluate asset prices in the context of the higher rates. Higher interest rates can be devastating for venture-like assets such as the Layer 1s or monetary commodities like Bitcoin. And unfortunately, the monetary conditions we’d expect to see in the near future are likely to be significantly different than the ones we’ve experienced these last two years. That said, with inflation currently around 7%, and expectations that it will settle in at closer to 3-4%, we’re still miles away from positive real rates even after this year’s expected rate hikes. The market is much more concerned with the narrative of rising rates than it is with actual positive real rates themselves.

Global Economic Deceleration

The icing on the proverbial cake of the macro headwinds is the slowdown that is already underway, driven partially by contractionary policy and partially by stiff year-on-year base effects for both growth and inflation.

Source: Arca Internal Research, Bloomberg

Usually, markets can stomach a policy pivot if accompanied by a strong economic backdrop (think of the Fed rate hikes in 2017 and early 2018). However, policy shifting into a slowdown is typically a recipe for disaster, with the market feeling both deteriorating economic fundamentals and a withdrawal of liquidity simultaneously. In the wake of the COVID economic collapse, year-on-year numbers for both growth and inflation have been thrown out of balance and will likely continue moving lower through the first half of the year.

Where Do We Go From Here?

Digital asset traders love to talk in terms of max pain—that is, which side (bulls or bears) will be hurt the most by a given move. While this has merit in terms of derivatives positioning, there’s something to be said for the prevailing narrative also leading to maximum pain for the most people. My read is that the marginal digital asset investor is now very nervous after the preceding week, but not quite ready to throw in the towel on the bull market.

While it may turn out alright in the short term after Friday’s option expiration and into this week’s FOMC meeting, this sentiment flies in the face of the worst macro conditions we’ve seen since March 2020 and before that, Q4 2018. With inflation as high as it is, the Fed is trapped. Much of the inflation is due to sticky factors such as supply chain and impending wage increases, primarily supply-side issues that aren't significantly affected by rate hikes. On the other hand, the Fed is facing increasing public and political pressure to do something about the spiraling inflation. It needs to project a hawkish stance to restore global public confidence even though it knows very well that a hawkish stance won’t do very much to solve the problem. Inflation will fall, but it will take time and space for that to happen. Until that point, the Fed is in a similar position as Homer Simpson.

Tightening monetary policy doesn’t have to be negative for asset prices. As we’ve written recently, in many cases, the Fed is able to hike for years while stocks and digital assets continue to soar. However, we need to separate the average hiking cycle from this particular case. Tightening into slowing economic conditions with contractionary fiscal policy is a very different environment than tightening in a fiscally-driven boom as we saw in 2017 after the Trump tax cuts, especially for the riskiest assets. The overtly negative macro conditions portend a volatile and rough experience for digital asset investors over the next couple of months.

Tightening monetary policy doesn’t have to be negative for asset prices. As we’ve written recently, in many cases, the Fed is able to hike for years while stocks and digital assets continue to soar. However, we need to separate the average hiking cycle from this particular case. Tightening into slowing economic conditions with contractionary fiscal policy is a very different environment than tightening in a fiscally-driven boom as we saw in 2017 after the Trump tax cuts, especially for the riskiest assets. The overtly negative macro conditions portend a volatile and rough experience for digital asset investors over the next couple of months.

When The Bulls Return to Catalonia

After a few months of getting chopped up, the prevailing narrative is likely to change to a more bearish consensus, and the max-pain trade may start looking quite different. Just when everyone is settled in for a year-long bear market (driven by the Bitcoin halving cycle, obviously!), we’ll likely see the macro shift that no one is anticipating. As the toughest base effects ease in terms of growth, we will swing from the feared economic disinflationary bust (falling growth, falling inflation) to a disinflationary boom (rising growth, falling inflation)—an extremely positive environment for asset prices.

Source: Arca Internal Research, Bloomberg

At the same time, we’ll likely have seen a couple of slowing inflation prints by that point, along with general signs of an economic slowdown. Knowing tight policy isn't accomplishing anything, the Fed will be comfortable pointing to the signs of cooling as a rationale to pivot more dovish. The nearly five hikes priced into markets for 2022 appear overdone in the near term; a more moderate line of a couple of hikes and balance sheet runoff is the more likely path. The worst of the negative credit impulse will also be behind us by mid-year, setting the stage for a more balanced fiscal stance in the future. Such a combination could be dramatically positive for digital assets, particularly at lower valuations, leaving newly cozy bears stuck on the sidelines waiting for the bear market to continue as a new bull market begins and digital assets rip higher.

As new players have entered the digital assets arena over the past year, this market has responded by getting more challenging to predict. “Old school” crypto investors are still hanging on to past narratives that are almost certainly not true, while newcomers are trying to use a traditional macro playbook that is untested in digital assets. Narratives of 4-year cycles or supercycles will be relegated to the sidelines as digital assets are irreversibly integrated into the global macro game and the global economy as they grow in prominence and fall in volatility.

Regardless of what happens in the near term due to macro conditions, none of these events should have any long-term impact on digital assets. At this point, most investors are in one of two camps.

Either:

- You believe digital assets are impossible to value, prices are overvalued, and the technology is nothing more than a vehicle for trading; or

- You believe that digital assets are a transformational technology that is reshaping everything from asset transfer to capital formation to stakeholder coordination and alignment.

We’re firmly in the latter camp, and nothing that happened these past few weeks has changed our minds—nor should it change yours.

Governance is Heating Up – a Maker Case Study

[Written by Arca Research Analysts, Matt Hepler and Alex Woodward]

Why Governance Matters

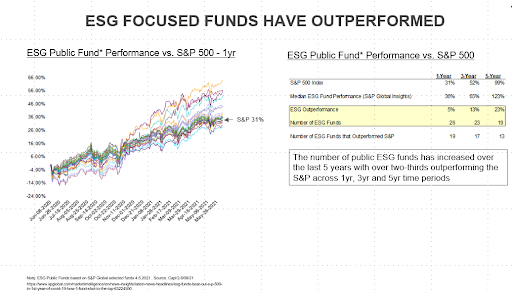

Governance in digital assets is becoming more critical as assets mature, and revenues and economic value rapidly increase. There is now something truly worth governing. In public equities, there is a clear relationship between companies with best-in-class governance and price performance, based on multiple ESG studies where governance is a key criterion. According to research by Axioma, “Companies with better environmental, social and governance standards typically record stronger financial performance and beat their benchmarks.”

S&P Global - Outperformance

Governance Participation

Equity markets have clearly defined stakeholder structures for investor recourse. These structures have resulted in governance systems that protect investor interests. But cryptocurrencies have largely been shielded from similar oversight.

“At an individual level, real monetary value is at stake, which in turn gives rise to investor and payment protection concerns,” says Philipp Hacker, a researcher who has authored a paper on corporate governance systems in cryptocurrencies. According to Hacker, cryptocurrency investors have rights similar to those for company shareholders because they are directly affected by protocol changes in a blockchain.

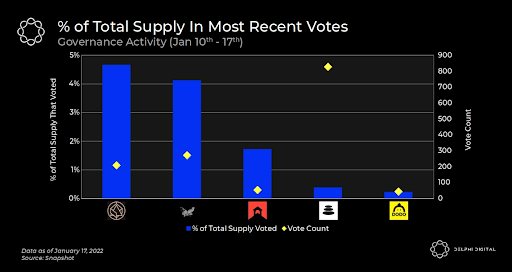

The question remains: how do we improve governance in digital assets? Many of the governance frameworks implemented over the last 50 years in public equities do not exist or are nascent in digital assets. These include a consistent cadence for investor proposals, financial reporting, and elections of representatives who are mandated to act as fiduciaries for investors. The core ethos of digital assets was to decentralize many of these decisions typically made by management teams and board members. Decentralization was meant to empower communities to participate, voice their views, provide feedback via forums/proposals, and vote collectively. Unfortunately, voter participation is still at extremely low levels in digital assets. For example, recent proposals have only averaged 1-9% voter participation rate versus up to 90% for public equities historically.

Prohibitive gas fees for smaller token holders, a lack of a regular cadence for proposals, and lack of standardized frameworks for voting are all hurdles for increased community participation. We believe increased transparency, accountability, incentive alignment and voting cadence will all be critical in improving governance and increasing investor confidence in the asset class.

A MakerDao (MKR) governance case study

Last week, ParaFi submitted a proposal to replace MKR’s current governance voting structure (one MKR token = one vote) with a new “governance boosted MKR” token (gbMKR). Essentially, Parafi proposes "veMechanics” (the “vote-escrowed” token model popularized by CRV) where investors that lock up MKR the longest (up to 4 years) are rewarded with more votes without additional incentives. Unlike other recent tokenomic proposals that improved incentives and economic value, such as Yearn (YFI), this MKR proposal lacks true incentives for utility or value. The support for this proposal was based on:

- Improving security (defense against an attack using borrowed tokens for votes to change the protocol)

- Taking supply off the market

- Increasing incentives for DAOs to hold the new token (gbMKR)

Though we applaud tokenomics changes, we believe the current proposal hinders voter participation and does not create true economic value or price support for MKR holders. A response to this proposal after submission from one of Maker’s Core Unit Facilitators summarizes this dynamic well:

“Governance participation for MKR is already paltry. You have three sets of MKR holders:

- a large majority who have no interest in participating in governance

- a small minority who delegate

- an even smaller minority who actively participate in governance

Adding lock-ups without incentives to participate in governance won’t stimulate anyone in set A to lock-up their tokens. Members of Set B and C are already participating in governance and empirically tend not to sell, but some subset will stop participating in governance due to the undesirable restrictions of locking up their tokens.”

Many of these arguments to add lock-up incentives for more votes without rewards can be compared to the same “short-termism” fears in public equity markets throughout history. Poison pills, staggered boards, dual-class voting structures, and joint Chairman/CEO structures are all mechanisms to defend against change from investors even when a company is underperforming and could benefit from a change. Most structures have been eliminated over time as institutions and investors have embraced an annual cadence of voting for proposals and representatives based on their performance instead of duration of ownership or employment.

Existing token holders should be considered the longest-term investors because they own the token today and are taking the most economic risk. However, at any point in time, particularly in times of high volatility, new token holders are typically buying from long-term holders that are selling, making them the new “long-term investors”. By definition, when an investor owns an asset valued at 15x sales or earnings, that is considered a very long-term investment.

One of the most critical points of support for the MKR proposal was to increase security. The recent MKR proposal does not cover the security case where the rewards of executing a protocol change outweigh the borrowed MKR's fair market value. In other words, if investors are borrowing to accumulate votes to change the protocol negatively, they are also taking the risk that their changes will destroy value. It will not be worth pursuing these changes if value is negatively impacted with a significantly lower exit price. Security defenses can be built into the token’s existing governance structures via bylaws or councils for significant protocol changes.

With no real tokenomic improvements, this type of proposal could likely decrease rather than increase voting participation; without real incentives, it could provide a minimal decline in MKR sell-side pressure. For this proposal to work, we believe MKR should incentivize locking up MKR for gbMKR via passing through protocol revenue to stakers. The growth of Dai over the past 2 years has led to a significant increase in protocol revenues; a portion could be distributed on a pro-rata basis based on the length of lock-up.

As economic value continues to increase in digital assets, further enhancements to governance structures are necessary to ensure responsible oversight. Creating a clear cadence, improving transparency, and continued advancements in tokenomics will begin to improve the lackluster voter participation. It’s very likely that some of the best practices from traditional finance will be adopted to support the evolution of the asset class.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM

Alex Woodard - Research Analyst

Andrew Stein - Research Analyst

Nick Hotz, CFA - Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Trading Operations

David Nage - Principal, Venture investing

Michael Dershewitz - COO of Arca Funds

Matt Hepler- Research Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency