What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

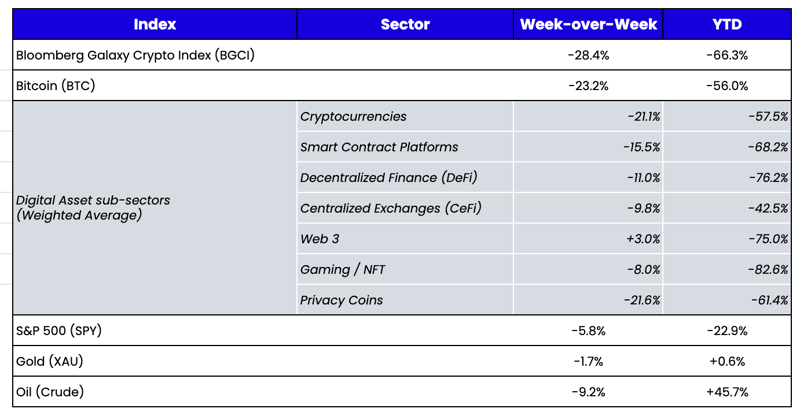

Week-over-Week Price Changes (as of Sunday, 6/19/22)

Source: TradingView, CNBC, Bloomberg, Messari

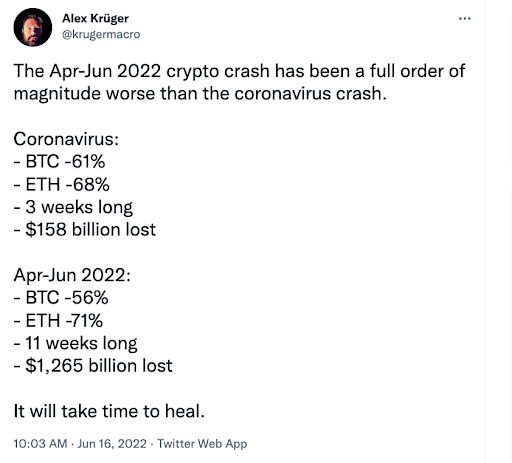

A historically bad week

Before we get into digital assets, it's worth quickly highlighting how much damage global markets have caused. Oil dropped -9% last week, gold fell almost -2%, and the S&P 500 dropped over -5% for the second week in a row despite yet another FOMC-induced head-fake rally, which was immediately reversed the next day. Monday alone was only the third day since 1962 where 10 year Treasury yields rose more than +20 bps on the same day the S&P 500 fell more than -3.5%, with the others occurring in 1982 and 1986. A 4-decade-old regime of loose monetary policy and falling bond yields has ended, and markets are vomiting all over themselves.

Meanwhile, last week may have been the darkest week in the history of digital assets. Not necessarily in terms of total wealth destruction or any singular event, but the totality of the hits made me second guess whether or not all of this actually happened in a single week. It did:

- Last Sunday, lending giant Celsius—who at its peak held customer assets of over $28 billion—halted all withdrawals, swaps, and transfers between accounts. They hired restructuring law firm Akin Gump to help with what appears to be either an out of court restructuring or imminent bankruptcy.

- Babel, Asia’s largest lender to miners followed suit and may be on the verge of collapse. Babel has assets estimated at around $2 billion.

- BlockFi, the other $20 billion+ lender, appears to be struggling to find new financing, and let’s just hope they are looking to plug a liquidity mismatch and not an asset mismatch.

- Three Arrows Capital—one of Asia’s largest prop trading firms—dabbled in everything from OTC trading, lending, Treasury management, venture capital, and NFT collecting. The company’s assets were estimated to be well over $10 billion at its peak. Now, it is likely insolvent, sending shockwaves throughout the industry, Archegos Capital-style, given how many counterparties they borrowed from (take your pick of articles to read about this implosion).

- Portfolio companies of Three Arrows Capital are publicly distancing themselves, as the market fears that Three Arrows managed the Treasuries of some of these protocols and companies.

- Arbitrage relationships were being tested left and right, from new speculative algorithmic stablecoins (USDD and USDN) deviating from $1 to staked ETH (stETH) continuing to trade at a discount to ETH to Grayscale’s GBTC and ETHE trusts trading at their lowest discounts to book value ever recorded (~35% discount).

- Ethereum (ETH), which before 2022 had put up 8 straight quarters of positive returns, has now declined for 11 weeks in a row and was down over -40% for the week before rallying back on Sunday.

Naturally, this has led to severe price declines, equity value destruction, widespread layoffs across the industry, continued deleveraging, and non-stop fear as market participants try to digest the impact. Investors, meanwhile, are forced to weigh the risks of further contagion against the opportunity to buy assets at significant discounts.

Eleven Random Thoughts On What’s Driving the Digital Assets Market

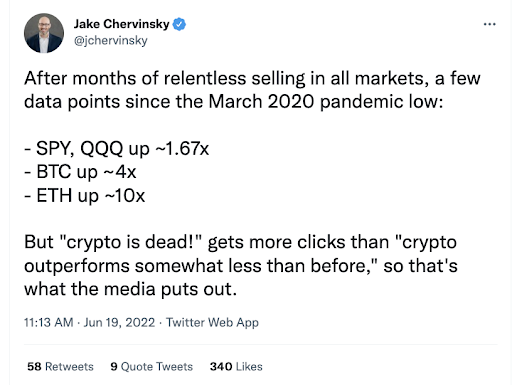

1) BTC and ETH are underperforming the broader market

Sometimes BTC underperforms ETH; sometimes ETH underperforms BTC. Rarely, if ever, do both underperform the rest of the market. But that’s exactly what happened last week, and month-to-date, as liquidations of collateral are dominating price action. Last week, most of the selling pressure was forced by centralized lenders (manually liquidating their client’s collateral as their loan-to-value metric soared) and by DeFi smart contracts, which programmatically sells collateral when the LTV hits a certain threshold. The rest of the selling has been in the form of short-selling and hedging. Since BTC and ETH are the largest and most liquid forms of collateral and the most liquid assets to delta- and beta-hedge with, these assets massively underperformed even though they are widely viewed as the safest and highest probability of success assets in the entire market. “Flight to quality” has been replaced by “run from liquidity.”

MTD and WTD returns – BTC and ETH are Underperforming

NYDIG wrote a nice piece highlighting some of these on-chain versus off-chain liquidations and how they can sometimes be misleading (leading to shorts trapping themselves by misreading the data):

“The Ephemerality of Liquidation Levels: With speculation about leverage in the crypto ecosystem running rampant, one aspect that market watchers have paid close attention to is liquidation price levels. Because much of the information about loans in DeFi is publicly available, blockchain analysis can reveal the loan terms, the value of the collateral, and determine the price at which a loan will break its covenants and be liquidated, the liquidation price level. This is interesting for two reasons. First, with counterparty risk becoming an increasing concern, this analysis can help participants determine levels at which certain entities might find themselves in financial difficulties. Second, liquidations create negative price pressure. Much of the pledged collateral is assets like wrapped bitcoin (WBTC) or ether (ETH) on the Ethereum blockchain. When loans are liquidated, large amounts of these assets can be sold on the market and drive price levels lower.

However, casual observers need to be careful about how to interpret liquidation levels. Borrowers are mindful of the prices at which they will be liquidated; and they have no interest in being liquidated. As prices approach liquidation levels, borrowers can contribute capital held elsewhere or repay some of the loan outstanding, both of which reduce the price at which their loan will be liquidated. An example is one particularly large position, likely held by Celsius, on the MakerDAO platform. MakerDAO allows users to pledge collateral to take out a stablecoin, Dai (DAI), which users can lend out, stake, or use for other purposes. In this case, as of last week, the borrower had pledged 17,758 WBTC worth $533M (as of June 9, 4PM) to borrow 278M DAI worth $278M. With a minimum collateralization ratio of 145% on the loan, this meant that liquidation would occur at a price of $22,737.71. Given the size of this position, observers were extremely concerned about this position as markets crashed. However, as price approached the liquidation level, the account quickly topped up their collateral across several transactions and returned DAI, bringing the total collateral up to 23,963 WBTC and total DAI down to $231M. This reduced the liquidation price to $14,004.11. The original liquidation price, clearly, was not in play as long as the borrower had capital elsewhere to deploy. This demonstrates the fact that liquidation levels, while interesting, may not tell the entire story of a borrower’s capital position.”

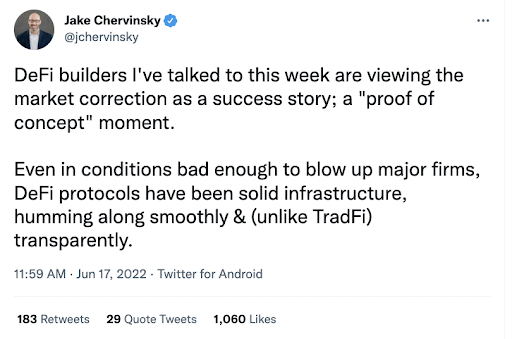

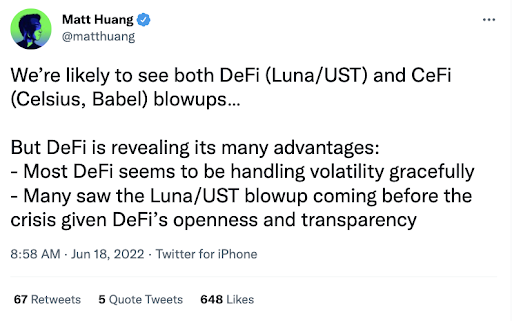

2) DeFi is kicking the crap out of CeFi

Decentralized lenders and applications are NOT failing; it’s the centralized lenders and businesses that are failing. As Brady Dale at Axios wrote this week:

“DeFi founders propose a different model for financial operations, one where everyone always operates by the exact same rules as everyone else, risk is always completely clear and no one gets a special deal. Take a DeFi lender: Every single interest-earning deposit and every single loan that's accruing interest can be seen on the blockchain. Similarly, every liquidity provider on an automated market maker can also be viewed, along with every trade it makes in each block. Compound Finance, one of the earliest DeFi money markets, shows daily updates for the total deposited and the total borrowed in each asset it supports right on its website. Here's where you can find the stats for ether. It currently has $717 million in ETH deposits and $13.9 million lent out.

The problem isn't access to the information. The problem is making sense of it because so much is available. On the other hand: Celsius doesn't work anything like this. Going all the way back to 2019, onlookers raised concerns about the transparency of its operation. At its core, Celsius has always promised to return much more of the income it makes from loans to its users than traditional banks do. What it didn't promise, however, was to make it clear how it earned those returns on a day-to-day basis. A DeFi platform couldn't suddenly lock out users' deposits, as Celsius did this week. If it were even possible, they would have to post a proposal for a public vote and discussion first (giving everyone more than enough time to go into a bank run).”

Everyone who understands DeFi is pointing this out:

3) DeFi is amazing, and its adoption is being held back

This isn’t the first, nor the last time we will write this, but decentralized finance (DeFi) flat out works—and it works incredibly well. It is the solution to many of the problems we’re seeing today concerning lack of transparency and contagion. We wrote about how DeFi apps worked with zero downtime or issues during the January 2022 meltdown, we wrote about how DeFi solves real-world problems when banks cut off their customers, and we’ve debunked many of the nonsensical statements made by naysayers. And once again, during the current wreckage, DeFi stands alone regarding transparency and health.

For those who continue to argue that DeFi has no real-world usage outside of trading and speculation, it’s not because the protocols and applications themselves don’t work; it’s because the end-user still doesn’t have a lot of options. For example, borrowing works great, but if all you can borrow is BTC, ETH, USDC, or USDT, it won’t be useful until merchants and customers accept these assets as payments. The problem isn’t DeFi; the problem is the lagging adoption of digital assets outside of the crypto ecosystem. Similarly, decentralized insurance, asset management, and exchange (DEX) protocols work terrifically, but what you can insure, which assets you can manage, and which assets you can trade are still limited to a small subset. DeFi application usage will explode once we bring real-world assets (home equity, jewelry, and other valuable assets) on chain and once we increase adoption of the assets outside this microcosm.

4) USDC = USDT; BlockFi = Celsius; Grayscale = Lido

This industry loves to make heroes out of certain players and villains out of others, even if they are exactly the same. Michael Saylor is a hero, but Peter Schiff is a villain, though they are the same type of promoters. Paul Tudor Jones is a hero, but Jeffrey Tannenbaum is a villain—and they are the same type of investors seeking asymmetric returns.

The companies that helped fuel this market—and whose problems are now damaging it—are also the same. USDC is widely viewed as superior to USDT, even though they both started as non-transparent, unregulated money markets, which only became more transparent because they were forced to be. The only difference is that USDT’s parent company, Bitfinex, has admitted wrongdoing in the past, while USDC’s parent, Circle, has a pristine reputation. But both offer identical products with identical limitations regarding centralization, potential issues in a drawdown, and potential asset-liability mismatches.

BlockFi and Celsius are the same types of lenders. They are both running unregistered hedge fund strategies using customer deposits, with inadequate disclosures, asset-liability mismatches, and loss-leading strategies funded by venture capital. Celsius has been hated for years due to an eccentric and brash founder, while BlockFi was heralded because of young, likable founders and their Tier 1 VC backers. Those who pointed out the inadequacies of both (like we did over a year ago) were largely ignored or shamed.

Grayscale and Lido are also the same—both offer an asset-backed product with no mechanism to force redemption, which was destined to trade at significant discounts to net asset value. Grayscale is vilified, perhaps due to its size and how long they have been generating fees despite losses; Lido is heralded for its innovation. They are the same.

5) Tether and Circle are making a fortune right now

Speaking of USDT and USDC, they are making a fortune right now. In a world where $20 billion worth of stablecoins (UST) can disappear overnight, and all other digital asset holders are hemorrhaging value, the issuers of the stablecoins themselves are the beneficiaries. With a combined $133 billion in AUM, the massive move higher in Treasury and corporate bond yields means they can now invest this float at substantially higher rates of return than at any point over the past five years. At a conservative yield estimate (using the 1 year Treasury yield of just under 3%), that’s almost $5 billion in annual revenues combined for these two stablecoin issuers. So any concerns about these assets not being fully backed, or being fully liquid, can be quickly offset and papered over by the enormous earnings that they are generating this year and beyond.

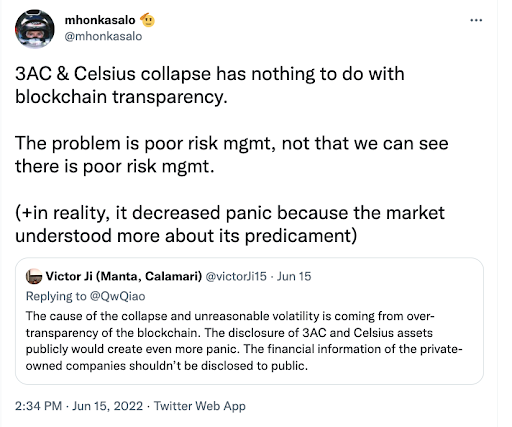

6) Transparency versus non-transparency

At Arca, we’ve always erred on the side of transparency and have pushed for more from exchanges, lenders, and token issuers. But this is a nuanced debate. For example, while Tether has increased its transparency via quarterly reports, the masses continue to cry out to Tether to show more—including revealing each asset that they own. Yet, at the same time, the second any of these companies show on-chain proof of assets like Celsius, Luna, or even Microstrategy, the vigilantes immediately begin hunting and targeting their liquidation levels and assets to put them out of business.

7) The grave-dancing, negative clickbait bias is very lopsided

We get it. The digital asset market is a train wreck right now, and train wrecks make for good stories. Anyone who has dedicated their life or career to building and educating about this industry is embarrassed, depressed, and scared.

But where are the positive stories? There have been billions in forced liquidations, but these forced sellers don’t just go into the abyss. There is a buyer for every seller, meaning billions of dollars have been put to work recently to absorb this selling pressure without a single bailout or buyer of last resort. Are any journalists trying to find who these buyers are? If Bill Ackman, Elon Musk, or Peter Thiel go to the bathroom, a journalist is there, ready to find out why. Yet not a single member of the media has written anything about the underlying bid to this market throughout the largest unwind in the industry’s history. No one is commenting on how well DeFi is working, how much cash asset managers are holding ready to deploy when the waters are safer, or trying to help all of the innocent protocols and companies that are caught up in a mess that had nothing to do with them.

CEOs, founders, and leaders are pouring their hearts out, trying to rebuild an industry they care about deeply. Let’s hope they get as much attention as the anonymous Twitter troll calling for BTC $3,000.

8) Speaking of cash, there is a lot of it

The last time the total market cap of digital assets was under $1 trillion, the AUM of stablecoins represented roughly 2% of the total market. Today, the total AUM of stablecoins is equal to $154 billion, compared to the total market cap of non-stablecoin tokens equal to just under $750 billion. That means cash in the market (as represented by stablecoins) represents 20% of all of the value of the digital assets that you can buy with this cash. And since there is very little that you can actually do with a stablecoin yet (other than converting it back to dollars if you want to leave the ecosystem or eventually redeploying it into other assets if you stay), stablecoin AUM represents a tremendous amount of built-up buy pressure that will eventually pour back into the market through a very small window. And this, of course, does not even consider the eventual reversal of the largest short-interest in digital asset history.

When buyers return, it will be incredibly lopsided.

Stablecoin AUM as % of Total Digital Asset Market Cap

Source: TradingView

9) Speaking of cash, it doesn’t take a lot to bailout this market right now

While we all know there is no Fed put, or backstop, to digital assets, one of my theories has always been that this industry is now so big, with such massive companies and politicians fully dependent on its success, that it could never get as bad as it feels right now. Eventually, if the carnage gets bad enough (subjective), there would be a few incentivized players who were big enough and cared enough about saving their own fortunes that it would be economically feasible with a high ROI to spend a few hundred million dollars to save tens to hundreds of billions of equity capital. Perhaps that is Binance, FTX, or Bitfinex. But this past weekend was critical in terms of finding white knights who could help develop a bid to stabilize this market. There's a point where smoking out your competitors takes a back seat to ending calamity. For instance, in 2020, Bitmex shut off their liquidation engine and bought liquidations with their own capital to prevent Bitcoin from literally going to $0 on their exchange (as the market was chewing through the bids set by market makers). In 2008, the banks with the strongest balance sheets bailed out some of the weakest, whether by government force or selfish incentives.

It doesn't take a lot of capital right now to support prices and failing lenders, and there are a lot of players incentivized to ensure this industry doesn’t fail.

Right on cue. Structurally, this market has weaker support than other financial markets, and the biggest players have a moral (and economic) obligation to support it.

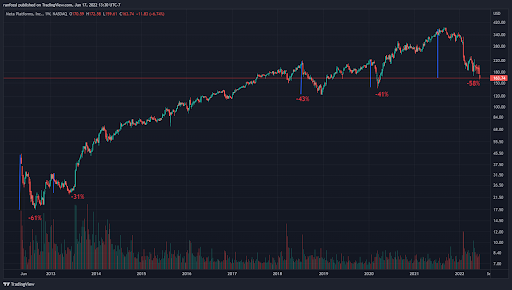

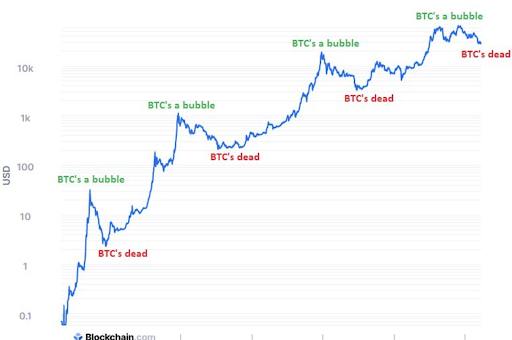

10) This market is not dying any more than FAANG stocks have died historically

The drawdown in digital assets is ferocious and painful. But Arca senior trader Renzo Anfossi took note of other large historical drawdowns—particularly of FAANG stocks. It's a good refresher on how common drawdowns of this magnitude are and how violent the moves can be on the way back. Below are some of the largest drawdowns for Facebook (META), Netflix (NFLX), and Amazon (AMZN). Note, they look pretty similar to that of digital assets.

11) Will the rumors and contagion ever stop?

As Larry Cermak put it: “The problem now is that everyone and their mom is spreading rumors about every single lending/yield platform and therefore it’s a losing game to leave money there IMO. They’ll run out of liquid cash to service withdrawals. And now they can’t really liquidate long term obligations and people would have to be dumb to want to be exposed to illiquidity risk now.”

That’s a problem. There isn’t a single financial institution on the planet that could service anywhere close to 100% redemptions due to illiquidity or rehypothecation, regardless of the health of the business. Hedge funds put up gates, not because they don’t have the assets, but because it takes time to liquidate positions. Banks don’t actually have the cash and are forced to parade their government FDIC backstops (or international equivalent). Insurance companies can’t pay all claims at once. All of finance is built on trust, and trust in digital assets is eroding.

But the withdrawals will eventually stop—either due to putting up gates (halting withdrawals) or via bankruptcy protection. Further:

- The deleveraging and forced selling will end

- Most of the companies that provide these services will disappear until there is government regulation that provides the same trust backstops as TradFi

- Those profiting massively right now from the contagion will sure up their balance sheets and implement tighter capital controls going forward.

So yes, the runs may continue from today’s exchanges and lenders, but those that can meet the redemptions will, which will increase trust. Those that can’t will file bankruptcy or halt withdrawals, which will be orderly.

12. Bonus: Overhangs are gone

There have been known overhangs regarding digital assets since inception. You can even see how many times we’ve referenced “overhang” in our five years writing this weekly market recap—from regulatory overhangs to shadow banking overhangs to custody overhangs to specific company overhangs. Well, many of those companies that were always perceived as riskiest (Luna, Celsius, Three Arrows) have now fallen, with others on death’s doorstep.

There are known risks—like swords hanging over the head of the market—and in the past month, three of those have fallen. When the overhangs are removed, that’s historically been a good time to buy.

What We’re Reading This Week