What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

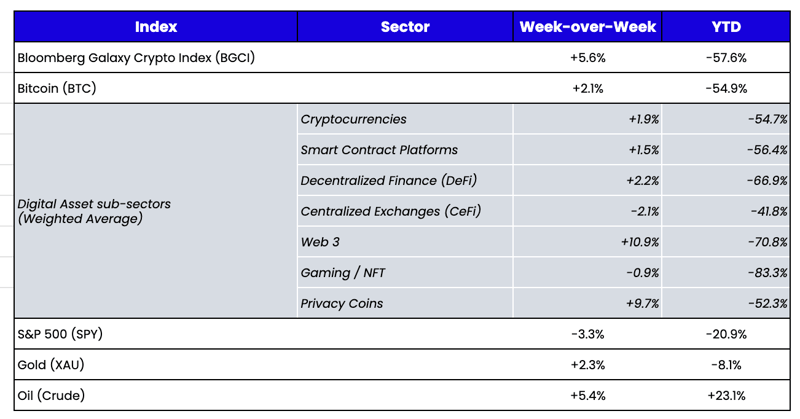

Week-over-Week Price Changes (as of Sunday, 11/06/22)

Source: TradingView, CNBC, Bloomberg, Messari

The FOMC, More Decoupling, and FTX/Alameda

We were one of the first, if not THE first, to point out that digital assets decoupled from macro many months ago. Most didn’t want to believe it when tokens were going down as stocks were going up, and only a few recognized it when tokens were no longer falling in unison with equities. But now that tokens are going up while equities are going down, it suddenly seems undeniable.

While the most common way to demonstrate this is via BTC or ETH versus equities, perhaps the best way to show the decoupling is via Uniswap tokens (UNI) and Coinbase equity (COIN). They are two identical businesses with roughly 99% of their revenue driven by retail trading, but one is the publicly traded stock of a centralized company, while the other is a governance token of a decentralized exchange. UNI and COIN had near identical returns from Nov 2021 through July 2022, but since then, UNI has broken out versus COIN, with a bulk of the outperformance coming in the last few weeks alone.

Source: TradingView

The driver of the most recent decoupling was, of course, the FOMC meeting on November 2nd, which confirmed that the central bank is not planning a policy pivot anytime soon and that the terminal rate could be higher than what was previously communicated by the September dot plot. The statement contained some dovish language regarding policy lags and the “cumulative tightening of monetary policy,” but Powell squashed the subsequent rally with a very hawkish speech. While this rope-a-dope induced a 5% peak-to-trough reversal in equities, digital assets largely ignored the hawkish rhetoric, with particular strength seen in MATIC, CHZ, ALGO, AR, and BNB. This may be because the rate of change of rising rates is bad for all assets due to a slowdown in growth, but once the pace of increases subsides, higher terminal rates alone have different effects. Cash-flow-producing equities, especially those with less cash flow today, are much more negatively affected due to lower DCF valuations, whereas a higher terminal rate has little to no effect on many tokens given they are essentially perpetual call options. Similarly, tokens are likely to be more recession-proof than equities and corporate bonds.

But the big story of the week had nothing to do with the Fed or economic data. Instead, two digital asset heavyweights, FTX and Binance, battled it out on Twitter, and chaos ensued. Roughly 80% of my Twitter feed is dominated by people uncovering new blockchain-based data about FTX, Alameda, and Binance wallet movements; often leading to speculative conclusions. But there are a few important takeaways:

- In 2012, Knight Capital, a public company with transparent financials, almost went under due to a large fat-finger loss, prompting a wave of capital calls and customer withdrawals. No one fully understood the extent of the problems, and ultimately Knight was rescued with a capital injection. Fast forward 10 years later, two large private companies—FTX and Alameda—are facing similar allegations with even less information about their financials. Yet, thousands of people on Twitter are acting as if they know everything that is happening. I wish I were as confident about anything as “Crypto Twitter” is about the health of these two companies.

- Many analyses are conflating Alameda data with FTX data; while they are most likely inaccurate, they are caused by a very murky past and lack of transparency about how the two entities are separate. And that is where public blockchain records are amazing. Much like what we saw with Celsius, Three Arrows, and all of the bridge hacks this year, the ability to see transactions on-chain in real-time gives customers and investors a level of information and comfort that was never previously available. In the last 24 hours alone, you could easily watch FTX’s stablecoin balances, Binance moving its FTT to an exchange to sell, the FTT holders list, details of panicked FTT sellers, related holdings of Alameda, and the plunge protection team mobilizing. There are also plenty of on-chain detectives willing to help out the broader community, like this great list of suspected Alameda wallets. There is a seemingly endless amount of real-time data to parse. Even the original FUD piece, which might as well have been written on a “Jump to Conclusions” map, is filled with well-researched data (albeit, in my opinion, several wrong conclusions). While calls from outsiders for more regulation grow louder with every hack and bankruptcy, the flipside is also true—the inherent transparency of the blockchain makes regulation less necessary.

- Conversely, data without proper analysis can lead to a lot of incorrect information spreading like wildfire. We’ve learned over and over in finance that a bank run can be sparked by virtually nothing, and while it's never ok to cause a bank run, it’s almost always smart to join one (rather than be last). And even though no one has enough information to make claims about FTX and Alameda’s solvency, we’ll never know for sure. That uncertainty speaks to the general opacity of centralized financial institutions and governments. Notice a pattern here? While decentralized financial applications are all still operating in fine order, many of their centralized counterparts are auditioning for a role in “The Big Short 2.” Over and over again, self-executing code via smart contracts is proving to make better decisions than humans.

- A lot of this speculation and rumor could be avoided by—you guessed it—more voluntary transparency. We’ve written over and over and over about how those issuing tokens and those who run centralized exchanges can make life a lot easier for themselves, their customers, and investors by disclosing more information. For example, exchanges should maintain a list of their hot wallets and cold wallets so anyone can check that they have sufficient reserves. There are a lot of reasons why FTX would be shuffling assets around right now: either they are scrambling for cash (bad), or they simply don’t have enough in certain wallets and banks are closed on weekends (totally normal). These are very different reasons, and makes it clear that we need more transparency from any business holding client assets. As is always the case, uncertainty and fear are worse than actual bad outcomes (and often cause bad outcomes that needn’t happen).

- Finally, there is a big difference between Celsius offering a net interest margin to customers that never actually existed—and therefore having to make up that shortfall through risky, illiquid investments—versus Alameda borrowing money against inflated collateral and then running high-velocity trading strategies with that “free money.” Many are conflating the illiquidity of their collateral with the liquidity of the assets they buy with the borrowed money. Again, we’ll never know for sure, but this is likely a non-event that is becoming an event because of how nervous the market is and how angry the digital asset community is at Sam Bankman-Fried for recent comments to lawmakers about the future of DeFi regulation.

Whether this blows over quickly or not remains to be seen. But regardless of how it ends, it’s another blow against the industry (and financial institutions in general) simply for a lack of voluntary transparency, but it’s another giant check mark for the transparency of blockchain data and the skilled researchers trained to uncover, read, and interpret this data. This will be a skill that every financial analyst will need in the very near future.

Chaos, Coordination, and Charizard

How an Obscure Internet Phenomenon Shows The Promise of Blockchains

By Nick Hotz, Research Analyst

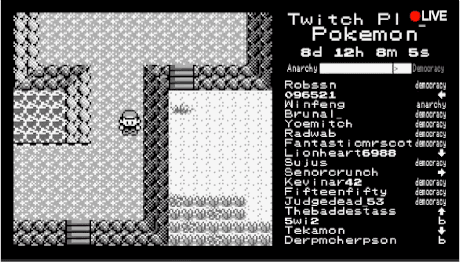

As a child of the 1990s and a pretty big nerd, I vividly recall getting swept up in the Twitch Plays Pokémon (TPP) frenzy of 2014. For the uninitiated, TPP was a social experiment in which a community of gamers on the streaming service Twitch attempted to beat the '90s Gameboy classic Pokémon Red by crowdsourcing all of the player's movements to the community (more here). To this day, TPP holds the Guinness World Record for "most participants in a single-player online video game," peaking at over 120,000 simultaneous players.

In Pokémon Red, the player controls Red, a character who roams a 2D world where he collects and battles monsters called Pokémon. (Fun fact: in the Japanese version of the Pokémon TV series, Red’s character is called "Satoshi"). The Gameboy has 7 buttons to press, which make Red perform various actions, and players on the Twitch stream could type in one of the commands (e.g., "Up" or "A") to attempt to influence the game. Unsurprisingly, given that certain parts of the game required heavy coordination among the thousands of users, the experiment was a predictably chaotic mess. Internet trolls gleefully ran amok, impeding progress wherever possible by purposefully failing puzzles, deleting the community's Pokémon from the game, and generally moving backward, while the honest majority attempted to complete the game. At the same time, even honest actors didn't always know the best move at any given time, which led to coordination failure and further setbacks as different players tried to complete the objective they deemed most important at the time.

Source: Twitch

In response to a multi-day failure to solve one not-particularly-hard puzzle, the Twitch stream added two new commands: (1) democracy, where players' button commands represented votes aggregated every 30 seconds to determine the outcome and (2) the original anarchy, where one command would be selected at random and implemented every second. A change to democracy required a 2/3 majority vote, while anarchy could be implemented with a simple majority. Despite the clear advantage of democracy, a good portion of the rest of the game was spent in anarchy. Many were outraged by the change they felt took away from the spirit of the game and worked even harder to impede the community’s progress.

Actual propaganda poster encouraging the community to remain in democracy mode

Actual propaganda poster encouraging the community to remain in democracy modeSource: Massachusetts Institute of Technology Game Lab

Despite introducing these changes and 24/7 streaming, the game took more than 16 days to complete and remained a slow-moving train wreck to the very end. As the game finally wrapped up, I recall feeling excited that the coordinated efforts of the majority were able to work together to win, but also discouraged by the number of bad actors working against the community's best efforts.

TPP was a case study in human coordination where the community, despite stumbling the whole way incoherently, eventually achieved its ultimate goal. In its small way, the community's effort to coordinate people to achieve a positive result is really the story of human progress. Great technological and cultural inventions like written language, the printing press, democracy, capitalism, and the internet were all just innovations in how people interact with one another to create more win-win outcomes. As we've played increasingly more positive-sum games throughout history, on average, we are more populous, fight less, live longer, and are wealthier than at any other time in human existence. Along the way, these leaps forward have been interspersed with many setbacks where we reverted to playing zero- or negative-sum games once more.

I contend that blockchain is another great innovation that will pave the way for coordination and win-win outcomes for humanity like never before imagined.

How Blockchains Could Help Us “Be the Very Best (Like No One Ever Was)”

Imagine for a moment that TPP ran again today, but this time with a blockchain tracking the community's commands and player's actions. How could our coordination and the overall outcome be improved?

First, non-transferrable/soulbound non-fungible tokens (NFTs) and fungible tokens could be issued to all players who log in, but only if they share a credible decentralized identity, like the one used by Gitcoin Passport to match funding for charitable grants. The NFTs would enable governance over the system and allow players to vote on changes. And identity verification would ensure, for the most part, that people are who they say they are.

The honest majority of players could quickly coordinate by requiring every player to post a small financial stake to make a decision. Any vote for the negative anarchy command would result in the voter’s stake getting liquidated by the majority, quickly weeding out bad actors. Multiple anarchy votes in a row could lead to the offending player’s removal from governance decisions or their commands carrying less weight. Decentralized insurance protocol Nexus Mutual has a similar mechanism for determining payout claims. Users vote on claims using their NXM tokens. Those who vote in favor of the claim receive a share of the voting reward, those who vote against the claim have their tokens locked for 30 days, and those found to vote fraudulently would have their tokens slashed/forfeited.

After dealing with any glaring anti-social behavior and establishing a permanent democracy, the community could then move on to facilitating the greatest amount of coordination and productivity from its honest (but not always completely rational) members. It could promote this outcome by establishing a meritocracy that incentivizes the best players to maximize their talents and allowing the community to share in the gains.

It could start by requiring each player to pay a small transaction fee for each command they send. Then, with the accumulated funds, the community could retroactively redistribute both the anarchy command penalties and transaction fees to players who performed the best at each vote for a new action. However, there's a major issue: how do you determine who actually performed the best and who was playing poorly or even anti-socially? In blockchain terms, an oracle would suffice.

One idea is that the players could establish an on-chain marketplace that uses futarchy—prediction market-based voting. In this system, people would speculate on what others think the best move is at every step, with the majority vote awarded the rewards. For example, if 40% of voters chose "A," 30% chose "Down," and 30% chose "B," then voters for A would win all the funds. The idea of a futarchy is to give honest actors an objective to coordinate around, namely winning the game. The system would incentivize people to understand what the actual best move is and vote for it, relying on the wisdom of crowds to happen upon that optimal move most of the time. Then, actual player commands could be compared with the marketplace results to determine if players were acting correctly, as determined by the market.

While it has merit, in practice, there are potential pitfalls. Namely, dishonest players can also coordinate to sabotage the market. In classic internet gamer style, they could, for example, establish a "Cult of A" that only votes for the command A and recruits others to the group to win every vote and receive the rewards. And if the "Cult of A" reaches a plurality of the voting power, the honest community is back to square one.

Alternatively, some smart community members could build machine-learning algorithms to determine the optimal move at any given point. Then, using zero-knowledge proofs, they could demonstrate to the rest of the players that their algorithm was indeed providing its optimal solution without revealing the algorithm. The community could then evaluate the results of these algorithms and stake their fungible tokens behind the one they think is best, with the majority decision of stakers deemed the optimal move. Rewards for providing this oracle would be split between the algorithm builder and stakers. Stakers choosing obviously suboptimal algorithms, such as one that always issues the command "A," could be slashed by governance, reducing the ability of dishonest members to coordinate, while improving the ability of honest ones to do so.

Although they could keep algorithms a secret, heavily incentivizing the best creators to open-source their work would allow stakers to see that the algorithm is superior. Low-quality algorithms would remain a secret, leading to a negative selection effect where algorithms that remained secret would be perceived as lower quality, and thus received less stake. With an honest majority community selecting the strongest oracle, it would simply rely on players to issue commands that matched the oracle command (determined by the best algorithm) to receive the rewards. Deviation would be self-defeating, since errant players would pay a fee to issue a command knowing they would not receive any retroactive rewards.

By using blockchain technology to create both sticks that penalize bad actors and carrots that incentivize the best performers, I believe the community could transcend the 16-day TPP dumpster fire and post a performance closer to the best players in the world who can complete the game in under 2 hours.

Zooming Out—This Is the Big Promise of Public Blockchains

Decentralization has substantial costs—the community of players performed much worse in aggregate than an average player would have independently. But it also has significant benefits, such as permissionless innovation and the fairer distribution of knowledge, wealth, and power. Moreover, coordination enabled by blockchains brings decentralization’s costs down considerably and, with the right mechanisms in place, can enhance the benefits such that the community can perform much better than the average.

While I've spent this piece fantasizing about how we could use blockchains in some weird corner of the internet, I contend that we've already seen them start to demonstrate the promise I'm suggesting. For example, regular individuals would not have had the opportunity to bid for the Constitution without the coordination enabled by ConstitutionDAO. Further, it would have been impossible to build out a global wireless network in just a couple years without the flywheel of blockchain-based incentives provided by Helium. And Gitcoin wouldn't have been able to raise and distribute over $72 million to fund open-source software without integrating its native GTC token to allow the community to decide where to allocate those funds. While the scale may still be small, the case studies demonstrating the potential of this technology are real.

After a euphoric bull market characterized by circular money games and million-dollar monkey pictures; and a bear market where it all vanished, it helps to step back and evaluate how far we've come. The tide going back out has revealed many swimming naked, but has also shed light on what has been truly impactful. While the market may not be appreciating it at the moment, the improvements in society's ability to coordinate enabled by public blockchains are more clear to me than ever. If blockchains could truly get 100,000 anonymous gamers to work together, what more could they do?