What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 2/07/21)

Our Argument For DeFi

Welcome back to the “bad news is good news” market. On the heels of disappointing employment data, U.S. stocks posted their best weekly gain since November, with major indexes closing at fresh highs, now up 73% since the March lows. Crude oil traded to its highest level in more than a year, gaining almost 10% for the week. And the 10-year US Treasury note pushed above 1.15%, quickly approaching March 2020 levels. Fiscal-stimulus expectations, progress on vaccine distribution, and less-than-terrible earnings continue to underpin the overall bullish market narrative.

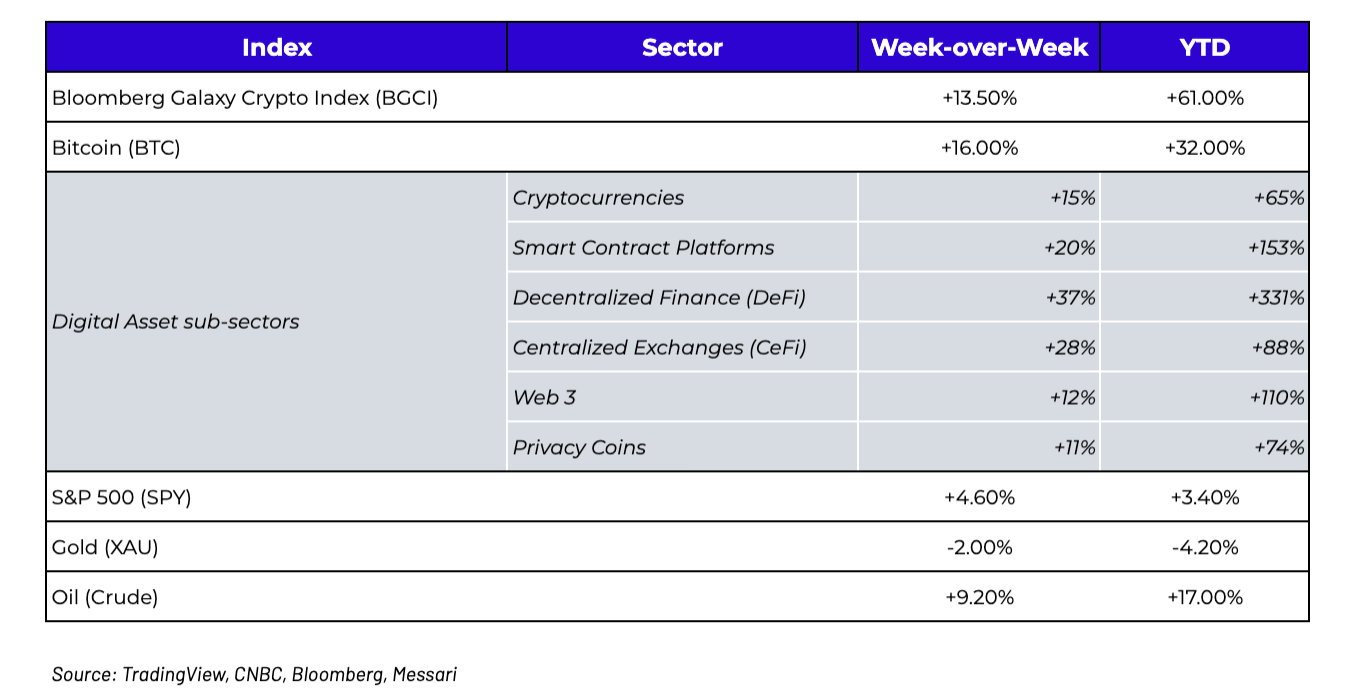

With this backdrop, digital assets remain well bid too, but once again, there was great sector dispersion. Cryptocurrencies like Bitcoin had a good week, posting double digit weekly gains fueled by excitement from Elon Musk and Michael Saylor, as well as progress announcements from Paypal and Visa. But cryptocurrencies actually underperformed the reset of the market. Smart contract platforms like ETH, ADA and DOT outperformed cryptocurrencies slightly, while centralized exchange “pass-thru” tokens like BNB, FTT and HT outperformed even further as the whole Exchange sector repriced higher based on relative value ahead of the Coinbase equity direct listing. Meanwhile, decentralized finance (DeFi) pass-thru and asset-backed tokens continue to outpace the field, generically rising 37% week-over-week. The DeFi Index has now doubled the performance of Bitcoin since the 4Q of 2020, and has gained +225% YTD compared to BTC’s +32% YTD gains.

The DeFi Index has massively outperformed BTC since last summer

Source: TradingView

The growth in DeFi, from a fundamental usage standpoint, has been nothing short of outstanding. And the price of underlying tokens, many of which directly benefit from this growth of users and revenues, has naturally followed. But many casual market observers, and even some industry professionals like to collectively refer to all assets that aren’t Bitcoin as “altcoins”, an archaic term that is at best confusing, and at worst misses the entire evolution of this asset class. This characterization incorrectly assumes that all digital assets are homogenous, and that owning Bitcoin or non-Bitcoin tokens requires a mutually exclusive choice much like betting on Tiger Woods versus the field at Augusta. But as the asset class continues to differentiate, and bifurcate, even the loudest Bitcoin maximalists are being forced to pay attention.

There are a few pundits out there that have built amazing media careers as Bitcoin supporters. In fact, Anthony Pompliano has arguably done more good for the adoption of Bitcoin than any single person, pushing Bitcoin into mainstream media and institutional investor focus. We applaud his work, and continue to support his efforts. In fact, in one of his recent “Pomp Letters”, he wrote one of the most profound statements about this space that I’ve ever read:

“...we may see the repeat of the 1990s equivalent. In the 1990s, you made a lot of money if you took existing businesses in the analog world and brought them online. In the 2020s, you are probably going to make a lot of money if you take existing businesses and figure out how to build decentralized versions.”

Well said. We have frequently highlighted some of Pompliano's best work. However, more recently, Pompliano wrote something about DeFi that we feel is incorrect and misleading. We feel that it is important to offer a counter argument. Pompliano wrote:

“There has been an explosion of interest in various applications and protocols that fall under the defi ecosystem. These different experiments are aimed at taking legacy financial services and decentralizing them in different ways. I use the word experiment intentionally because some of these will work and most of them will not. That is how experimentation is supposed to work though. What is interesting to watch is the extreme ends of the spectrum play out at the same time. On one hand, you have many of the most popular projects hitting all-time highs right now, on the other hand, you have projects that are being hacked for millions of dollars.

This presents a really interesting environment. You have high risk, high reward. Most people will shy away from this situation, but traders and professional investors will flock to it. This is especially true when you realize that the asymmetric upside presented is in the thousands of percent, but the downside risk to many of these professionals is 1x (they lose only the money they invest). I continue to caution people about the various investment opportunities outside of Bitcoin. The high levels of price and liquidity for the digital currency has drastically reduced the risk when people are gaining exposure to it. The same can not yet be said about these DeFi protocols or applications. Maybe one day that changes, but maybe it doesn’t. The market will be the ultimate referee. What I do know is that it will be hard for institutional investors to get comfortable allocating capital to areas of the market that are susceptible to theft or hacking. While an individual or company can be hacked in the Bitcoin world, there are no hacks of the actual blockchain. This will be an area to watch over the coming months. If institutions get comfortable with the risk-reward, there should be significant capital inflows. If there continues to be security breaches, it may prevent that wall of institutional capital from entering. Time will tell.”

To start, we do agree on one thing. Using decentralized finance applications is new, risky, and experimental. There have been hacks, including a recent $11 million hack of asset management protocol Yearn Finance. If you decide to send assets to a non-custodial, faceless entity in order to trade, borrow, lend or earn income, you are taking risks and may potentially have little recourse if there is a hack or user error.

But that is the only thing we agree with. Let’s break down the areas with which we disagree.

First, deciding to use a decentralized protocol as a customer is very different from deciding to invest in the tokens that power, govern and underlie the protocol’s success. Just like you don’t have to be an Amazon customer to own AMZN shares, and you don’t have to fly 30,000 feet in the air at 500 miles-per-hour in a giant metal tube that is prone to crash in order to be a Delta (DAL) shareholder… similarly, you don’t have to be a DeFi user in order to invest in DeFi tokens. To conflate investing in DeFi with using DeFi is misleading and inaccurate. There are less benefits when you choose to be a passive investor versus being an active participant in a decentralized network, and that can lead to lower return potential, but that doesn’t mean you have to be an active participant. Plenty of investors own the tokens of DeFi protocols without ever putting funds at risk.

S

econd, even if you are a DeFi user, there are ways to protect your assets. Insurance protocols like Nexus Mutual allow you to protect your assets from hacks on a number of DeFi applications. For a very modest premium, you can protect 1-for-1 any assets that you choose to put at risk. In fact, the same $11mm Yearn Finance hack that was highlighted above has had several valid claims on Nexus Mutual, and those who insured their risks will be made whole. As DeFi grows, so do ways to insure and protect against the risks.

Third, many DeFi protocols don’t force you to put your assets at risk. Decentralized exchanges, like Uniswap and Sushiswap for example, never force a user/trader to give up control of their assets. As such, while a user of the platform still risks user error when sending and receiving digital assets, that is the same potential risk of any blockchain transaction, including Bitcoin.

And finally, the difference between owning the equity of a centralized FinTech company in digital assets (Coinbase, Robinhoood, BlockFi, Binance) or any other centralized company (Target, Equifax, Verizon) is not that different, from a risk standpoint, than owning a token of a decentralized company or project. Centralized companies that handle customer email addresses, data, and customer assets have frequently been subject to hacks. While the Bitcoin blockchain itself has never been hacked, investments in companies that handle Bitcoin, digital assets, customer data and other forms of value have been hacked frequently. To suggest that these equity investments are somehow different, or less risky, than investing in DeFi tokens is false. When Robinhood makes a mistake with customer assets (and oh boy have they made plenty), the value of shareholder equity may go down due to fundamental declines in Robinhood’s business, but your shares are not at risk just because customer assets are at risk. Similarly, when a blockchain is hacked (like Yearn Finance), the native YFI token may deteriorate in price as the fundamentals supporting that token decline, but you are not at risk simply by passively owning the YFI token itself. The risks of the blockchain are totally independent of the risks to an investor in the blockchain’s native token.

“What I do know is that it will be hard for institutional investors to get comfortable allocating capital to areas of the market that are susceptible to theft or hacking.”

Institutional investors are educating themselves quickly on the different types of digital assets, and in many cases, are further along with these educational efforts than those doing the educating on the main stage, especially those that have ignored this part of the market in favor of Bitcoin for the past several years. An investor’s goal is to understand the risks and rewards, and to allocate based on those expectations. A protocol being susceptible to hacking or theft is far less dangerous to an institutional investor than the spread of repeated and unchecked misinformation.

Bad Questions Deserve Bad Answers

Pompliano of course isn’t alone here. A very prominent financial media outlet asked me to opine on the following question earlier this week.

“Bitcoin vs. Ethereum: Which Is the better Investment?”

Since there is no chance that my answer will ever make it to print, we decided to print our answer below.

Asking whether Bitcoin or Ethereum is the better investment is like asking whether apples or chocolate are the better fruit to eat. It can't be answered because the question is flawed. BTC is a cryptocurrency on the Bitcoin blockchain that has graduated from an unknown internet fad to a global form of "money" that now touches more sections of the investment universe than any single asset other than US Treasuries. BTC is being used or traded by hedge funds, insurance companies, corporate treasurers, central banks, broker/dealers, RIAs, family offices, individual investors, and just about any individual with a smart phone who lives in an emerging or tyrannical economy. Whether BTC goes up or down in US dollar terms remains to be seen, but it is clearly a powerful asset. ETH is a token on the Ethereum blockchain, and is not a cryptocurrency; it is a smart contract platform that powers a growing decentralized economy that attracts both human and financial capital. It is a base layer technology with which many other applications are built upon it. Think of Ethereum as the IOS app store, and Bitcoin as Apple Pay.

The two are not comparable. Both can be owned, and the risk/reward is very different. Blockchain is a wrapper, in the same way that the ETF is a wrapper. What we put inside the wrapper is most important, and BTC and ETH are very different assets that just so happen to be inside the same blockchain wrapper. You would not compare a healthcare equity ETF to a municipal bond ETF just because they are both ETFs --- In the same vein, looking at BTC and ETH and assuming that they are related to each other, or related to other digital assets, simply because they share the same blockchain wrapper is woefully insufficient. Digital assets can be anything from in-game swords to securitizations to PDFs to music files. Cryptoassetsare all in the same subclass, which is blockchain, but they are clearly not the same.

BTC will likely be a strong investment because governments around the world are double-dog daring you to own cash and bonds, and with interest rates low, the US dollar going down, and money ubiquitous... BTC will increase its purchasing power in US dollar terms. ETH will likely be a strong investment because an entire multi-trillion dollar financial services economy is being replicated on the Ethereum blockchain. And a select few other digital assets, from asset-backed tokens to revenue pass-thru tokens, will likely be strong investments as well because tokens are becoming the greatest capital formation and company bootstrapping mechanism we have ever seen, effectively combining shareholders and customers into one entity.

When participants in this industry start asking the right questions, there will be a lot of money to be made listening to accurate answers.

What’s Driving Token Prices?

Bitcoin dominance (BTC.D) continues its downtrend, falling another 2% (-14% YTD). As of now, this marks the steepest decline in BTC.D since April 2018 (dead cat bounce, -20%). This metric is just a reflection of market conditions, and the climate right now reinforces that movement: Bitcoin is consolidating after a stellar 4Q (+170%), CEX’s are soaring as Coinbase’s direct listing is right around the corner, DeFi is flying as projects continue to iterate and value continues to flow to the tokens. Overall, capital rotation from BTC into ETH has given rise to heavy trading and drastic moves. Hell, a certain token, which shall not be named, is up 15x YTD purely on evangelism.As noted in a previous edition of Two Satoshis, these market conditions are few and far between - but boy are they wild. This market is akin to shooting fish in a barrel, except you miss the barrel and somehow still get a fish. This week, we focus on projects with fundamental updates, ignoring the fact that their price movements blend in with the crowd:

- Hxro (HXRO) announced that they have chosen Solana as their layer-1 blockchain in an effort to increase speed, throughput, and cost efficiency of their options and derivatives products. The token itself will continue to exist on the Ethereum blockchain (ERC20), while also existing on the Solana blockchain (SPL). The team also mentioned that the token economics will be revamped, with staking, incentive rewards, and on-chain governance around the corner. These direct incentives will be given out as a function of network transaction fees, not perpetual inflation. In the following weeks, the project is looking to release more information on the token redesign, the path towards decentralization, and the roadmap moving forward. The token reacted to the news, finishing the week up 38%.

- Nexus Mutual (NXM/wNXM) saw a sharp increase in active cover (+$414M, +150%) since the launch of Armor (not affiliated) on January 24th, a DeFi coverage aggregator underwritten by Nexus Mutual. As of this writing, $505M in cover (per Dune Analytics) has been purchased since launch (with the discrepancy coming partially from active cover rolling off, and partially from seven claims being accepted following the Yearn finance exploit). Separately, Nexus Mutual passed proposal #121, which is “one of the largest upgrades we’ve made since launch”. Highlights from this proposal include mutual investments being enabled, and a restructure of the bonding curve to protect against potential extreme scenarios in both directions. We believe that the true price of Nexus Mutual is reflected in the free market price of wNXM, which gained 32% on the week.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.png?width=512&name=unnamed%20(53).png)