What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

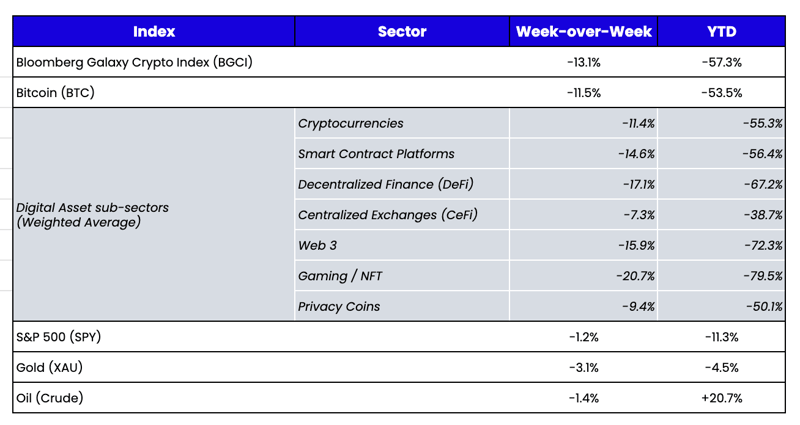

Week-over-Week Price Changes (as of Sunday, 08/21/22)

Source: TradingView, CNBC, Bloomberg, Messari

High Beta Losses

A week after we declared that digital assets have decoupled from macro, naturally, the macro backdrop took center stage once again, as equities, bonds, and digital assets sold off following hawkish statements from Fed officials. It sets the stage for this week’s Jackson Hole economic forum, where Powell will likely tread carefully after missing the mark with his assessment of the economy at last year’s summit.

Almost every coin and token traded lower last week, with only a handful of exceptions. It’s been six weeks since digital assets traded homogeneously like this, breaking a long string of healthy price dispersion. However, digital assets traded with close to a 10x beta to equities last week, which is abnormally high, suggesting something else was at play besides a generic risk-off environment. This outsized move was likely driven by continued negative (and uncertain) interpretations regarding far-reaching sanctions OFAC levied on Tornado Cash and everything it touches. Most notably, last week, Ethereum core developers discussed at length measures to preserve the Ethereum protocol’s censorship resistance. While mostly hypothetical for now, this debate picked up steam after a question to Lido Finance, Coinbase, Kraken, and Staked asked how they would handle validating Ethereum nodes if U.S. regulators requested they censor certain transactions. Brian Armstrong, CEO of Coinbase, responded and said that while the scenario is one he hopes the exchange does not encounter, Coinbase would ultimately choose to shut down itsx staking operations rather than participate in censorship.

This hypothetical situation put the market on edge, leading to significant losses across the board and one of the largest long futures liquidation days since the Three Arrows implosion. The market went from “long on the ETH 2.0 merge” to “so many concerns about the ETH 2.0 merge” in a matter of days.

But is it really that big of a deal? With the Ethereum 2.0 merge only weeks away, we considered the 6 major concerns investors and blockchain experts have cited regarding the merge and found most are overblown. While “long ETH” is certainly a crowded and telegraphed trade, it is likely still one of the best risk/reward investment opportunities in digital assets right now.

Concerns About the Ethereum Merge Are Overblown

Written by Arca Research Analyst Nick Hotz, CFA

It's official! Ethereum developers selected September 15 (+/- a day or two) for the Ethereum blockchain to merge with the Beacon chain, which will transition Ethereum from using proof of work (PoW) consensus to proof of stake (PoS). With under a month left, confusion about all aspects of the merge has swept the community. Rumors abound of capital sitting on the sideline anxiously waiting to see if the merge is successful, ready to deploy into ETH post-merge once uncertainty dissipates. Tensions are running high ahead of arguably the biggest protocol change in blockchain history, and many worries—some legitimate, some not—are being tossed around with little context. Let's consider the most prevalent concerns and see if there is as much potential risk as many seem to think.

Concern #1: The Merge Will Be Delayed Again

After nearly seven years of delays since the switch to proof of stake was first proposed by Ethereum founder Vitalik Buterin, the digital asset community is perhaps justifiably a little skeptical that this time the merge is actually happening.

Why It's Overblown:

Simply – the date is set; developers would need to change the code again to push the merge back further. There is little desire among developers to see the merge delayed.

Technically – total terminal difficulty (TTD) is the total amount of computing power/hash power ever dedicated to the Ethereum network. A specific number of TTD is set to determine the timing of the merge.

At their most recent core developer meeting, Ethereum developers expressed openness to changing the TTD, but only to make it lower if computing power dropped sharply. While they discussed other risks, none brought up potentially delaying the merge as a result. There is one shadow fork test left between now and the merge; if it somehow went catastrophically wrong and introduced a new set of bugs, then it could delay the merge. Color us skeptical.

Concern #2: A Miner Revolt

Ethereum miners rely on a proof of work system to earn their profit; once the system goes to proof of stake, their equipment won't be worth much. Last year, concerns grew that miners would attempt to tamper with the chain to force proof of work to stay in place.

Why It's Overblown:

Simply – the merge date is set; there's little leverage miners have left.

Technically – originally, developers decided to use TTD rather than a specific block number to initiate the merge to mitigate the risk of miners manipulating the hash rate dedicated to the chain to gain leverage and potentially delay the merge. With TTD set, miners' best option to delay the merge is to simply go offline—but this would mean missing out on the remaining mining rewards. Additionally, the largest mining pool, Ethermine, is switching to a staking service provider. Most other big pools either publicly support the merge or have plans to mine Ethereum Classic after the merge occurs. So at this point, there isn't sufficient interest or incentive to attack the chain.

Concern #3: Some DeFi Apps Will Stop Working/Assets Will Not Copy Over CorrectlyThis is probably the concern we’ve heard more than any other and is likely the lowest risk. Strong Y2K vibes here.

Why It's Overblown:

Simply – this isn't how the merge works.

Technically – a hard fork means that blockchain nodes and validators decide to build a new block on top of a changed set of code. This code change only affects the Ethereum protocol and does not refer to individual applications. We've spoken to many project teams from DeFi to rollups, who all said the same thing when asked what they were doing to prepare for the merge: "nothing."

Concern #4: The Merge Will Be Unsuccessful

Prominent traders and others in the digital asset space have speculated that the merge may simply be unsuccessful when the time comes for the switch.

Why It's Overblown:

Simply – there's no world where we would reach the merge timing and nodes receive the message, "Merge unsuccessful, :( sorry." Ethereum will switch to proof of stake at the time of the merge.

Technically – an "unsuccessful" merge is too general to address, so we’ll try to break this down in a few directions.

When the merge happens, it's up to the consensus layer (Ethereum 2.0) clients to talk to the execution layer (Ethereum 1.0) clients correctly. As long as they are communicating, the blockchain can progress to achieve "finality" of blocks. However, if 1/3 of clients aren't understanding each other or go offline, the chain will not be able to reach finality for some time. In all testnets and shadow forks, this issue has been resolved quickly, if it happened at all.

Three Ethereum testnets (Ropsten, Sepolia, and Goerli) and nine "shadow forks" have merged successfully. Many of the hiccups seen in testing arose from the fact that these tests were not the real thing, whereas the actual Ethereum merge probably would have gone smoothly. If there are issues, it would likely be a short disruption to some clients due to a fault in communication.

Others may be concerned about the chain reaching TTD and the switch from proof of work to proof of stake simply not happening. As far as we know, this wouldn’t be possible unless every single client was offline—then, there would be much bigger issues. When the TTD is reached, Ethereum will switch to proof of stake, regardless of any hiccups.

Concern #5: The Proof of Work Fork Will Compete With Ethereum

When the merge occurs, miners will be left with equipment that's not good for much. Thus, some miners have banded together to create a proof of work fork of Ethereum (ETHW) around the merge, attempting to take market share from Ethereum. The most "credible" attempt is backed by notorious Ethereum Classic proponent Chandler Guo, founder of the Tron blockchain Justin Sun, and a handful of Chinese Ethereum miners.

Why It's Overblown:

Simply – in an interview with Blockworks, Guo stated, “There is still a 90% chance this will not succeed."

Technically – because stablecoins provided by Circle (USDC) and Tether (USDT) and wrapped assets like WBTC will not be redeemable on any forks, all assets collateralized by them will immediately be subject to liquidation in DeFi after the fork. As a result, the new miners have decided to freeze all accounts related to DeFi "to protect users’ ETHW tokens until the protocols’ controllers or communities find a better way." Talk about decentralization!

In addition, last August's EIP-1559 upgrade currently burns around 80% of all ETH paid in transaction fees on the network. However, on the proposed fork, these funds will go to a multi-signature wallet managed by miners. As a result, miners will get all fees paid to and all inflationary rewards issued by the blockchain; tokenholders will get nothing.

Sometimes it's hard to tell the fish from the shark at the poker table, but this time it's obvious. Don't get burned by an obvious cash grab.

Concern #6: Validators Will Censor Transactions

Censorship fear is the most legitimate concern regarding the merge and could be a separate piece by itself. Under the proof of work system, miners are generally anonymous and well distributed around the world. In proof of stake, many validators are centralized, with over 60% of staked ETH located inside the U.S., staked by companies and DAOs like Coinbase, Kraken, Lido, and Staked that need to comply with U.S. regulations.

The recent OFAC blocklisting of Tornado Cash addresses brought this issue into a starker context. Will regulators be happy to only sanction addresses, or will they apply their mandate broadly? Is staking easier to regulate than mining? The perceived risk here is that in the event of further action by regulators, the Ethereum community will fracture into camps of those who oppose the censorship and those who support it, potentially leading to a contentious fork in the worst-case scenario.

Why It's Overblown:

Simply – companies and projects are overreacting to the limited guidance from regulators, and developers are intent on seeing the merge through on time regardless of these concerns. This is a potential medium-term risk, but it will not affect whether the merge happens. While it’s always good to prepare and debate “what if” scenarios, it’s improbable that the OFAC sanctions on Tornado Cash were intended to have more far-reaching implications than they already have, let alone the potential to shut down Ethereum staking. It’s much more likely that regulators didn’t consider the 2nd and 3rd derivative issues that their actions caused.

Technically – it comes down to how U.S. regulators define "facilitating" illicit transactions. From a technical perspective, hashing a new block onto the longest chain in proof of work accomplishes the same result as signing a new block in proof of stake. However, the act of "signing" onto a block containing transactions to/from blocklisted addresses could be seen differently by regulators. However, enforcement would likely need to come from another regulatory body, as OFAC is a U.S. Treasury sanction—not an SEC sanction and not criminal.

Core Ethereum developers discussed these developments on a recent call and agreed that they would rather leave the community than tolerate censorship, meaning a fractured community is unlikely. There was also no discussion of delaying the merge. In addition, an organization called Flashbots, which provides software to help bundle transactions into blocks, also open-sourced its code, which will help those who wish to create blocks with all transactions be able to do so.

Even under proof of work, the largest mining pool, Ethermine, is already censoring transactions. While these transactions will still be included in the chain by non-censoring miners, they will be delayed whenever Ethermine wins a block. So, in this case, switching to proof of stake will reduce protocol-level censorship.

Finally, as noted earlier, Coinbase founder Brian Armstrong said that he would rather give up Coinbase's lucrative staking business than censor transactions as a validator, which would lock up millions of ETH without yield until withdrawals are available sometime next year. If this occurred, it would be very bad for Coinbase but inconsequential for Ethereum as other non-U.S. validators would step in.

Depending on highly uncertain regulatory action, the Ethereum community may have some things to work out; still, the community is very much in consensus about the direction it feels Ethereum should take if the worst-case scenario should occur. Either way, it would be a problem to deal with after the merge.