What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

Week-over-Week Price Changes (as of Sunday, 5/22/22)

Source: TradingView, CNBC, Bloomberg, Messari

Counterparty Health Check

The market didn't exactly storm back after one of the bloodiest weeks in digital asset history. Most digital assets were lower last week, though there were a few bright spots and green shoots amidst crowded shorts; more of a reflection of seller exhaustion than any real new demand or growth. U.S. equities didn’t fare much better, dropping another 3-4%, with the S&P 500 now in an official bear market (-20% from closing price peak), and the Dow Jones notching its 8th straight weekly loss (the longest streak since 1932 per Cliffwater). In addition, Target and Walmart saw their worst one-day declines (-25%, -12%) since the Black Monday crash of 1987 amidst reports that rising costs and supply-chain disruptions are hurting their profits.

Fear is rampant. And you’d have to look long and hard to find a bullish investor across any risk asset. Those that are expressing bullish views are being bullied. Our friend Paul Kremsky at Cumberland expressed this sentiment over the weekend:

“I have always viewed the significant headline of 2020 to be Paul Tudor Jones’ public entrance into Bitcoin, not because of the balance sheet deployed there but because of the permission structure that was established, allowing traders at every fund, even at the capital-I Institutions, to begin the conversation about investing in crypto. Well, after seven weeks of downticks, there is not much of a permission structure to be Long. It is embarrassing in polite company to be Bullish. That extends not just to polite company, but to pitches to the CIO or at trading team stand-ups. As it gets harder to be bullish, less funds are long. And with most funds under water this year, there’s not much incentive for an individual trader to stick his or her neck out. Being flat or short right now is not a forced position, by any means, but it is the path of least resistance.”

It’s pretty lopsided right now, for sure. Beyond price action, the rumor mill is rampantly speculating the next shoe to drop. In the wake of the digital asset wreckage, many market participants (especially those from TradFi) assume there are more skeletons in the closet ready to come out. There are renewed rumors about Tether’s collateral,

Celsius’ solvency, and Coinbase’s regulatory disclosure regarding what would happen to customer assets in a bankruptcy. So we spent most of the last week looking into this counterparty infrastructure. More bluntly, after weeks of major carnage, forced selling, and margin calls, we are working to assess whether or not there really are more dead bodies out there waiting to float to the surface. Warren Buffet notably said, “Only when the tide goes out do you discover who's been swimming naked.“ But via our channel checks, thus far, we simply haven’t found any evidence to suggest that any of the rumors are true.

The market infrastructure seems far healthier than most think. A run on the market’s largest bank, a crash in asset prices, and a semblance of all hope lost have somehow been contained without bailouts or lifelines.

Over the past few weeks, every major OTC dealer forced payback of loans from their customers, even for non-callable and overcollateralized loans, to make sure their clients were liquid. Each of our channel checks suggested that every fund, miner, or borrower could meet these demands quickly and easily. Conversely, every fund has scheduled 1-on-1 calls with their OTC dealers to assess their health, and balance sheets seem to be in great shape. What transpired was almost like a game of Clue, except it’s hard to find the murderer, the weapon, and the room if no one actually died. Activity feels orderly, with credit lines tightened and settlements easily repaid, followed by a re-extension of credit and margin to those who want it.

Sure, stablecoin AUM is falling fast—USDC is growing at the expense of DAI, USDT, and others in the wake of the UST collapse—but the process of redemptions has been orderly, with slight depegs quickly re-pegging. We’ll likely see a few more runs given the vulnerability and fear in the market, but the system seems to be functioning and capable of handling the turnover.

TradFi tends to assume that leverage and rehypothecation bury digital asset participants, but they fail to adjust to a few realities from the past few years:

- Leveraged liquidations on exchanges are much cleaner and faster in this space, with most liquidations used as de facto stop losses rather than complete loss of principal (e.g. if you use 10x leverage on a 1% position and get wiped out, that loss is no different than using no leverage on a 10% position with a stop loss down -10%). The leverage amplification is generally to the upside, not the downside.

- No one can use leverage in digital assets the way they do in debt and equities because you can’t get unlimited undercollateralized credit lines from multiple prime brokers. The TradFi PB model allows funds to operate for weeks or months, even when they are already dead (i.e. Archegos Capital), by spreading risk around the street and delaying and praying when things go south. In digital assets, margin calls are quick, and settlement is T+10 minutes using stablecoin settlement.

It’s possible that the market will worsen before it gets better, and healthy balance sheets today could be replaced by defaults, but those that are actually stress testing the system are learning the cracks are cosmetic, not structural. Perhaps a system that was built upon a skeptical foundation did a few things right to secure the dam.

Ironically, as the industry performs health checks, it is working on better ways to use its technology to solve these very issues in the future. Why guess when we can bring all of this data on-chain? The nature of a public blockchain is to be a transparent record-keeping system that can extend beyond the balance sheets of financial counterparties to employment credentials, credit checks, and uncollateralized lending.

It will be a magical day when blockchain evidence replaces the rumor mill.

Fire to Ice: An Update on the Global Macro Storm

By Arca Research Analyst, Nick Hotz

The Great Inflationary Fire

The first half of 2022 has been a firestorm. Inflation has continued to come in red hot, outpacing even the biggest inflationists' expectations. For the first few months, the firefighters at global central banks simply let it rage until it was clear the anticipated brushfire had become something greater and more sustainable. At some point, the Fed knew it had to act. Unfortunately, an inflationary fire is more like a grease fire than a natural one—liquidity only makes it worse. The only way to put out a grease fire is to stifle it, and that's exactly what the Fed has done—projecting incredible hawkishness to suffocate the fire and, simultaneously, the financial markets. As we noted in the original Storm Before the Calm piece, the Fed has been stuck between a rock and a hard place, with the difficult decision of letting inflation fester or tightening policy and hurting demand. Lately, it has confidently chosen the latter.

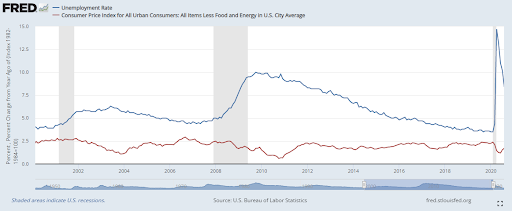

For the Fed skeptics convinced the "Fed put" is in sight since its main goal is to prop up asset prices, consider the following: every large economic shock in most people's investing lifetime has been a negative demand shock. Every meaningful decline in the stock market, including 1987, 1990, 2001-2003, 2008, 2011, and 2018, were all associated with demand shocks to the economy. 2020 saw both supply and demand shocks, though the magnitude of the demand destruction outweighed the supply crunch. Such shocks are initially characterized by worsening business confidence leading to rising unemployment rates. As a result, we see falling stocks, commodity prices, and bond yields. Demand shocks eventually create disinflationary economic forces, and require additional liquidity injection in the system to spur demand. In such a circumstance, the Fed and the investor are aligned—both want rate cuts and more liquidity to arrest the downturn.

In a demand shock, rising unemployment leads to falling inflation:

Source: FRED

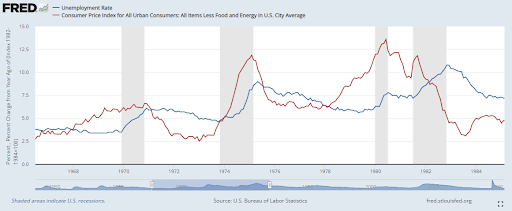

For the first time in a very long time, we're seeing a negative supply shock. This type of shock was more prevalent in the 1970s and, before that, the 1940s. It is characterized by falling household confidence due to rising inflation. It is also associated with falling stocks but, conversely, rising bond yields and commodity prices. Supply shocks force monetary policy agents to work against investors, tightening policy despite stagflationary conditions. You certainly have never heard the Chair of the Federal Reserve say, "There could be some pain involved in restoring price stability" during a demand shock. While Powell himself has been promoting a soft landing (well, at least a softish one), other speakers have been more clear about the need to slow demand and tighten financial conditions. For those of you who still have your sanity, that's Fedspeak for "increase unemployment and send risk assets lower." As monetary policy tightens, the economy slows, and, eventually, so does inflation.

In a supply shock, rising inflation leads to rising unemployment:

Source: FRED

A Calm in the Eye of the Hurricane

Investors have been seeking shelter for months as the inflationary fires continue to rage. But recently, we have seen signs that the Fed's suppressing strategy is beginning to take hold. Days of big downward action in stocks are no longer accompanied by rising Treasury yields but are now resulting in declining yields. The 10-year breakeven inflation yields (10-year Treasury yields minus the expected inflation rate) have fallen to their lowest levels since February. Crude oil has been unable to surpass its March highs over $120. Other commodities from copper to corn to gold are all off April highs. Investors are now clearly expecting lower inflation in the coming months.

Source: BofA Global Research

The winds of this storm are shifting, and there's a cool breeze in the air. Barring another supply shock, peak inflation is upon us and in the short-term, a relief rally due to an incremental easing of Fed rhetoric could be in the cards. Bearish sentiment is extreme in the digital asset markets and across risk assets; the Fed has been in wait-and-see mode over the past few weeks. However, as the weather transitions from scorching hot to comfortable, investors will soon wake up to phase two of this supply shock: a collapse in growth.

Fire to Ice

As Fed rhetoric continues to become reality, the pleasant breeze of peak inflation will continue to morph—eventually into a bitter economic frost. Growth has been in a slowdown for almost a year now, clearly so for at least six months. Many indicators like housing and manufacturing are well off reopening highs. On the other hand, earnings expectations have yet to be revised much lower and unemployment remains at its lows, meaning the slowdown's effects aren't yet obvious in the real economy.

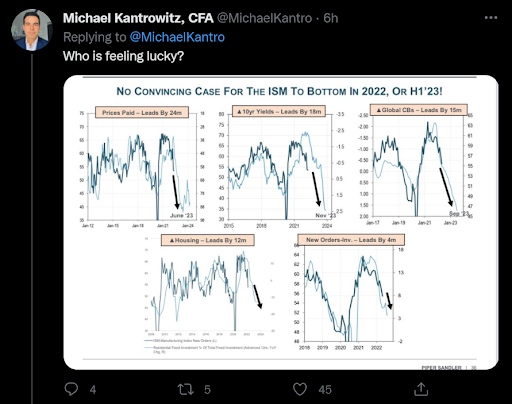

For better or worse, leading indicators of growth point to the likelihood of further slowdown. The ISM index, a bellwether of the global business cycle, is in position to continue falling in the months to come, reflexively leading to lower profits and higher unemployment.

Source: Twitter

Notice in the chart below that the most lagging indicator of interest rate hikes is Core CPI. We need to see all other parts of the economy weaken before we can expect negative pressure on inflation beyond what year-on-year base effects bake in. This means inflation likely continues to be sticky high until the housing and manufacturing weakness flows through to the rest of the economy and investors start worrying more about recession than inflation. Only when growth is at its coldest will we see the inflationary fires really start to extinguish.

%20.1%20.jpeg?width=512&name=unnamed%20(2)%20.1%20.jpeg)

Source: Piper Sandler

While a potentially vicious relief rally appears more likely at this point than we've seen in a while, the case that the supply chain and monetary supply shock has spawned a cyclical bear market is stronger than ever. Risk assets of all stripes, including digital ones, continue to have a tough outlook ahead as long as inflation remains high, growth continues to slow, and the Fed keeps the liquidity faucet turned firmly off.

Digital asset investors looking to understand and profit from the shifting macro conditions need to change their understanding from what's worked the past few months. As inflation peaks, the dollar may lose its potency as an easy risk-off signal of tighter policy. Bond yields will start rising on risk-on days, not falling. And when growth slows to the point that stocks start trading down on positive news and up on negative news due to expectations about monetary policy, understand that the pivot, and potentially the market bottom, is imminent.

Speaking with people involved in the space over the last week, two things have stood out most. The first is that sentiment is almost uniformly bearish and everyone is expecting new lows. The second, however, is that people expect the coming bear market to wash out the excesses of 2021 and leave a new crop of the most passionate long-term thinking builders and investors to create the ideas that will power the next cycle of adoption. Despite the dire nearer-term outlook, everyone in this space has as much conviction that great things will come out of it as I've ever seen. Though the global macro storm has been fierce, we've reached its final phase, and the seeds of the next bull market are being sewn as we speak.

What We’re Reading This Week

%201.jpeg?width=603&name=unnamed%20(2)%201.jpeg)