What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

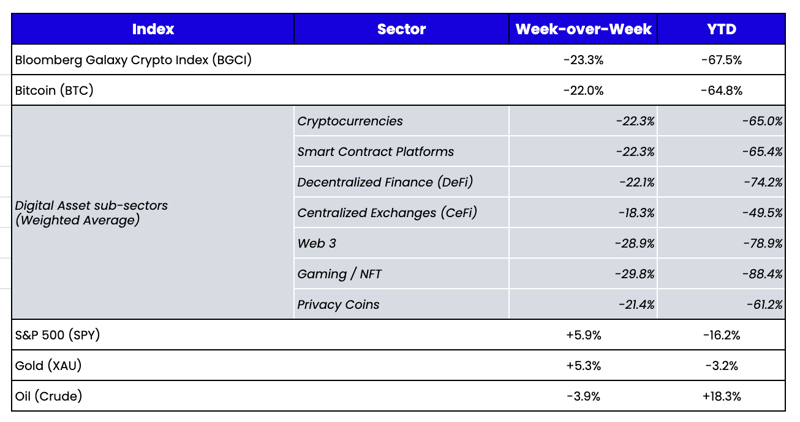

Week-over-Week Price Changes (as of Sunday, 11/13/22)

Source: TradingView, CNBC, Bloomberg, Messari

Fraud — A Tradition Unlike Any Other

It was somehow only one week ago when we pointed out how digital assets rallied while equities collapsed following the FOMC meeting. It felt like digital assets had bottomed and were becoming more resilient than other asset classes. Last week, of course, the exact opposite played out. The lower-than-expected inflation number sent equities soaring, rates plummeting, and the U.S. dollar to a 3-month low. In a frictionless vacuum, digital assets probably would have rallied 20%+ as well. But alas, there was, um, some friction.

The digital assets market uncovered a fraud so large that it looks like Bernie Madoff and Elizabeth Holmes got married inside Enron’s headquarters.

I won’t spend time recapping the crazy FTX/Alameda sequence of events—enough has been written about the timeline, and I applaud everyone who has spent time uncovering the truth. But this will likely unfold as one of the messiest, most complicated bankruptcies in history, with over 130 affiliated entities. Instead, I will highlight what I think are the most important takeaways and go-forward actions for this industry.

First, I truly love this industry. I—and so many people at Arca—believe deeply in the future of blockchain, especially concerning DeFi, NFTs, the tokenization of real-world assets, and immutable data records. We are sitting on a remarkable technology that could one day shape all of finance and ownership rights. Yet the industry continues to shoot itself in the foot and it is beyond frustrating to watch.

That said, while this is terrible for those affected and is yet another appalling instance of bad actors gravitating to an unregulated and lawless industry, it’s important to separate the assets from those who run the companies that trade and custody these assets. Most will not bother to make this distinction, instead rushing to judge the technology and the investable asset class. But if the zookeeper commits a felony, no one would accuse the lions, tigers, and bears. I hope the media and regulators can make similar logical conclusions about blockchain and digital assets. To be clear, this was finance fraud, not crypto fraud, and it looks a lot more like MF Global than it does “blockchain gone wrong.” The investable asset class and the underlying blockchain technology will bounce back without government intervention like it generally does, albeit with fewer companies driving innovation and progress. Hopefully, the remaining players and those who emerge feel a sense of responsibility to avoid the same fate.

The last cycle created unfettered market forces, which led to record levels of VC investing and amazing innovations between tech and token structures. However, without regulatory standards or stable firms in the space, much of this industry was built on rotten foundations—overleveraged businesses, ponzi-nomics, bad actors, and greed. The next cycle will have to be different. The ETH Merge, ZK rollups, KYC, DIDs, and traditional corporate and financial entrants are sowing the seeds of a cycle that may be more methodical but should be built to last.

It’s unfortunate that it took multiple failures committed by some of the worst human behaviors to demonstrate how useful self-custody, cold storage custody by regulated custodians, and DeFi are for safeguarding and transacting digital assets. Regulators and institutional investors were determined to force asset managers into antiquated regulatory frameworks reliant upon third-party systems because it fits better into existing workflows. But the irony is that the very technology we are investing in is also the solution we believe will eliminate the problems that keep surfacing.

The line between centralized companies using blockchain and native applications built on the blockchain itself is admittedly blurry; this week demonstrated exactly how the two intersect. By following on-chain evidence, a centralized company that invested, traded, and “safeguarded” digital assets was found to be fraudulent and insolvent. The blockchain records were flawless, and those trained to read and analyze blockchain explorers uncovered in a matter of days what the SEC and other regulators couldn’t find in months—possibly due to many conflicts of interest. At this point, if you don’t know how to read on-chain data, learn. Immediately.

So, where do we go from here? First, we must acknowledge that there are many more trees to shake. In my opinion, here they are in order of who is in the most trouble:

- FTX customers — including some funds with significant assets stuck that may be forced to shut down and send whatever is liquid back to their LPs. Additionally, there are companies and blockchain projects that hold their token treasuries on FTX. This, unfortunately, is quite an extensive list, and a first cut at a recovery framework indicates pretty low recoveries.

- Bitcoin miners — already facing defaults and liquidations amidst costs exceeding revenue, but will now be met with unfriendly lenders pulling back loans as the BTC price goes lower and losses accumulate at lenders.

- Market makers — aside from the fact that most used FTX themselves and therefore may also fall into category 1, many will have a difficult time as liquidity will get worse before it gets better. The already fragmented list of “trustworthy” exchanges is only getting more fragmented and untrustworthy.

- Companies and projects in which FTX/Alameda invested — especially those that were already in bankruptcy (Voyager) or heading in that direction (BlockFi) and can no longer rely on the backstop offered by FTX.

- The Solana community — hopefully, this is a short-term problem and not a long-term one, but SBF and Alameda became the de facto face of this Layer 1 blockchain and have significant economic interests in most applications built on Solana. This is yet another example of a singular entity becoming too powerful—similar to when the Bitcoin community tied its fate to Elon Musk and Michael Saylor. Whether intentional or an unintended consequence, Solana is heavily associated with SBF and his former empire.

So that’s obviously not great for many individuals and companies, but also not a death blow long-term for those who can get past what will inevitably be a very tough couple of weeks/months.

Second, we have to acknowledge how many people and firms turned a blind eye or didn’t care to ask the tough questions. For all of the great reporting that has come out this week, let’s not forget that most of the same authors fighting for Pulitzers now were also the same ones writing fluff pieces about SBF just months ago. But most people, including most of us at Arca, wanted to see SBF and FTX succeed. Anyone who has asked me about FTX or Alameda knows that I was always skeptical—not because I ever suspected fraud or foul play (not in a million years), but because I believed a couple of quant jocks with little to no experience were in over their heads as they became the industry’s largest everything: largest VC, 3rd largest exchange, largest (only) distressed buyer, largest corporate sponsor, largest Washington influence—you name it. But we still rooted for them. While we thought their most recent valuations (both equity and tokens) were inflated and hard to justify based on currently available data (the numbers always left us with more questions than answers), we still benefited from the liquidity and features of their exchange.

Moreover, the entire industry benefited from their image as the “responsible agent of this space,” even if many would have chosen a different figurehead to spearhead our cause. A reporter even asked me last week, "Does this hurt more because SBF was the face of your industry?" I replied, "The media made him the face of the industry. No one inside the industry felt that way. The media continues to create heroes and villains while the quiet builders and leaders get little to no air time.” That said, it is undeniable that SBF did become synonymous with “institutional blockchain.” And that is going to take a long time to repair. As our friends at Cumberland noted in a private chat shared here with permission, “Going forward, even for companies that are enthusiastic about coming into crypto, it’s going to be harder for them to have the confidence about finding the right partners.”

But there will also be many positives that come out of these events. For starters, DeFi is again showing outperformance to identical businesses built by corporate and centralized companies. If you look on-chain, Alameda paid back all of its DeFi loans before it covered anything on exchanges or with OTC lenders because you can’t build a relationship with smart contracts and charmingly convince the predetermined code not to liquidate you. It seems so obvious that this is a better way to avoid future blow-ups. Overcollateralized, transparent, on-chain finance protects more than opaque shadow banking. This has to be a bigger part of the future.

Second, we are finally seeing other exchanges demonstrate willing and voluntary transparency in light of this week’s events. We mentioned last week that at a very minimum, exchanges and custodians should be required to perform cryptographic proofs of reserves; some exchanges and custodians are now pledging to do it. Proof of reserves is native to blockchain. It is not possible for custodians of traditional assets, but it would add significant transparency for digital asset custodians and exchanges, providing a meaningful differentiator from the opaqueness of TradFi. As Galaxy Digital wrote in their weekly note to clients:

“There should be only two paths forward for service providers and applications: 1) centralized with rules for transparency and custody or 2) fully decentralized and non-custodial.”

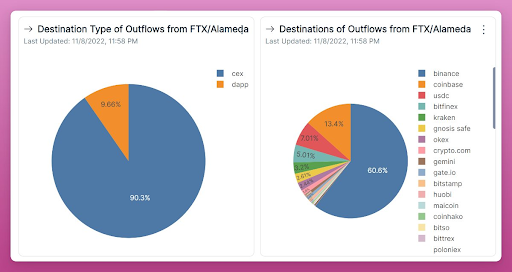

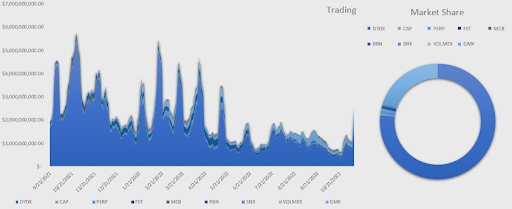

Speaking of fully decentralized and non-custodial, a clear shift is occurring. While outflows from FTX largely moved to Binance (61%) and Coinbase (13%), a flurry of trading activity also moved to decentralized exchanges like Uniswap (UNI), dYdX (DYDX) and GMX. Not coincidentally, DYDX and GMX were two of only a handful of tokens that were higher week-over-week

Source: TokenTerminal and Arca internal calculations

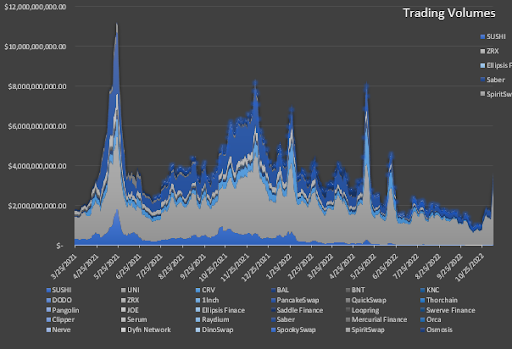

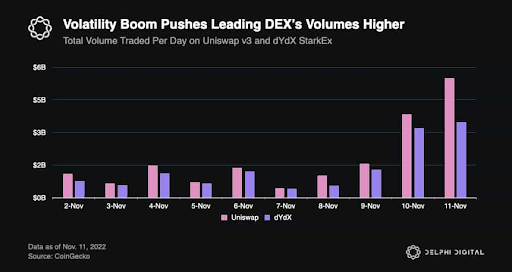

Due to the volatility of the markets and everyone offloading risk, volumes on DEXs were up 66% week-over-week to $21B. This led to one of the first month-over-month increases in volume since May (+40%). Uniswap is currently capturing 77% of the market share. Similar to spot DEXs, decentralized derivative volumes were up 130% week-over-week to $17.5B. This was led by GMX (+235% WoW), and dYdX, which currently controls 77% of the market share (GMX at 20%).

Source: TokenTerminal and Arca internal calculations

Source: TokenTerminal and Arca internal calculations

Source: Delphi Digital

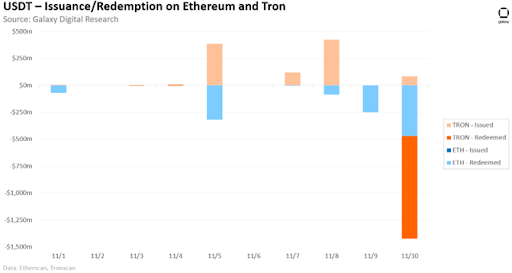

Additionally, Tether processed $2.1B worth of USDT redemptions across Ethereum and Tron networks, including $1.4B in a single day on Thursday after USDT briefly traded below its peg. What a dichotomy this created—TradFi poured hundreds of millions into FTX and FTX-affiliated funding rounds while shorting USDT. Yet, Tether is the one still standing and operating as usual.

Source: Galaxy Digital

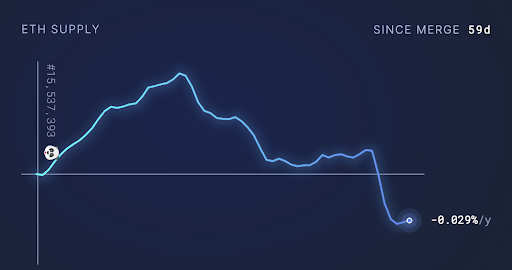

All of this on-chain activity has led to Ethereum reaching deflationary status, meaning since the merge to proof-of-stake (POS), more ETH has been removed from circulation via burns than has been issued to stakers via inflation.

Source: Ultrasound money

So while there was some good to come out of this week, it was ultimately a dark and frustrating period. We’ve been writing this weekly market recap for almost 5 years, and we’ve touched on every problem area in this industry: from leverage and lack of transparency to anointing heroes—all of which keep happening over and over again. Perhaps the team at Cowen digital put it best in their weekly report:

“In the span of my 25 year trading career, I've seen several contagions - from the 1998 Russian bond crisis, Long Term Capital unwind, 2000 tech crash, 2008 Global Financial Crisis, and the 2010 flash crash, to name a few. Having pivoted my career full time in the last few years to crypto, I've now seen an 80%+ drawdown - which has included the cascading unwind of an unsustainable protocol bring down an overly levered hedge fund, bring down a dozen+ lenders with little or no risk management - All in the last 12 months. Yet, these crises do share several common traits (not with me, I hope): Usually a lethal mix of hubris, leverage and poor risk management. So after crypto's vomit-inducing roller-coaster in June, I had to think that we'd learned our lesson in this nascent asset class. I figure, it’s better to have experienced the evil dark side of capitalism and modern finance, while the contagion could be contained, than to have seen crypto's tentacles spread deep enough to cause real damage to the broader economy. Yet, only a few short months later, here we are again. My current reaction, besides anger and sadness, is: REALLY? C'mon people, we are on the precipice of an explosion in blockchain technology that could potentially permeate every facet of society across the globe. AND WE KEEP SCREWING IT UP!! We continue to take the short path to paper riches at the expense of long term sustainable wealth creation. I have no doubt SBF is incredibly smart, and built an incredible operation that helped foster retail and institutional growth and adoption of the digital asset product. I'll spare the Icarus reference, even though.....well....anyway.

What has this got to do with the development of technologies on Ethereum (ETH) and the Web3 builders out there changing our future? Very little, I hope. What has this got to do with the growth of crypto as an asset class? Potentially quite a lot. Crypto has always been seen as fringe, with many participants hailing decentralization as a form of government protest. Not your keys, not your coins and many other phrases have come to represent the new landscape of financial and technical freedom. But to think that this asset class can reach escape velocity without proper regulation, is truly a fool’s errand. We all abhor useless and ill-advised regulation, mostly promulgated by out-of-touch politicians whose goal it is to line their own pockets. But at the end of the day, in order for the global investment dollars to be pointed towards crypto, and that really means trillions of dollars, we will need a regulatory path. I hope that investors are able to separate fear-driven sell offs from fundamental development and growth. I hope to see a competent regulatory framework that allows trillions of dollars of investment in a digital ecosystem."

Source: Twitter

Source: Twitter Source: Twitter

Source: Twitter