What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

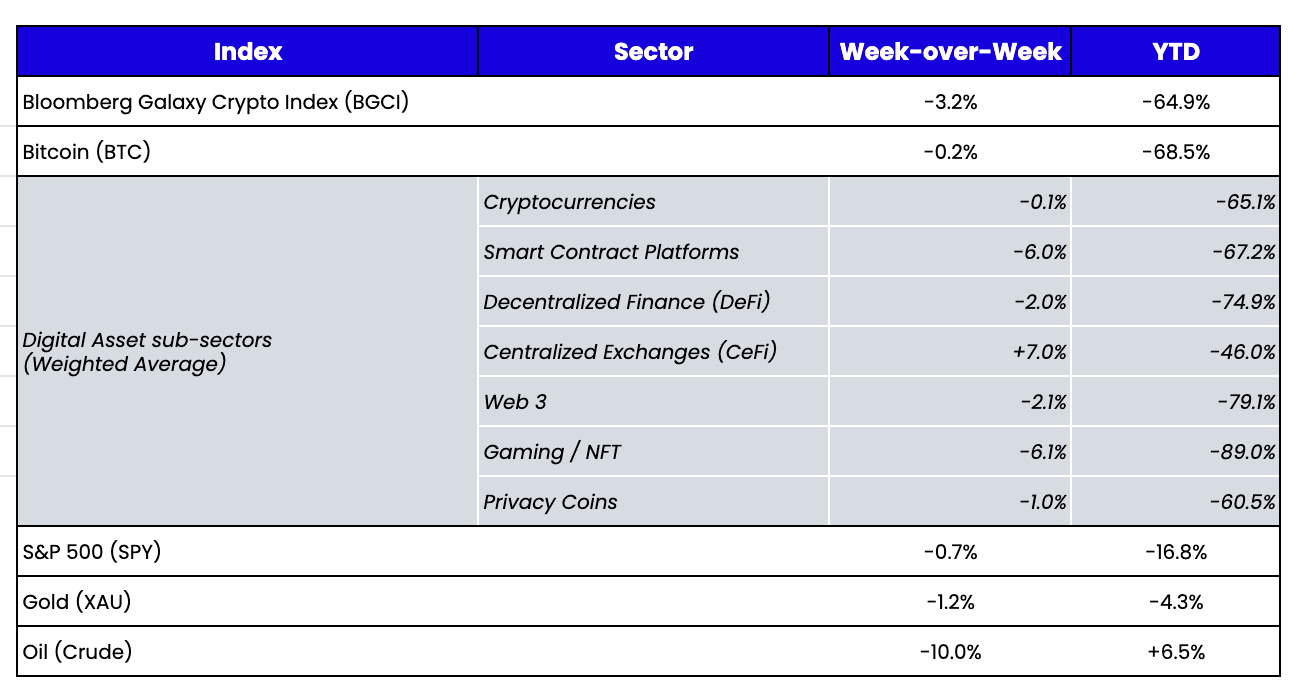

Week-over-Week Price Changes (as of Sunday, 11/20/22)Source: TradingView, CNBC, Bloomberg, Messari

No One—and Everyone—Saw It Coming

The digital assets market is reeling right now, although prices of digital assets themselves are holding on relatively well despite the recent string of bad news. Some of the largest service providers in the industry are either restructuring or heading that way. Many retail investors have their money trapped or liquidated, while some institutional funds are unwinding. Reporters are out for blood, and the “I told you so” crowd is louder than ever. The rumor mill is nonstop, and even without merit, you’d be foolish not to at least take each rumor seriously enough to investigate. And as often is the case when an extreme event happens, many are trying to make heroes out of the few who saw these events coming.

But that last point is tricky—who really saw it coming? There are only a handful of publicly traded companies in this young industry with transparent financials and a growing yet small list of successful, transparent, decentralized protocols. But the industry is still dominated by large, centralized companies. Almost all the problem children in this market have been private, centralized companies with human decision-makers acting fraudulently or, at best, had opaque (if not purposefully hidden) private balance sheets and corporate structures. So even if you “saw it coming,” did you really?We wrote this in late 2020 regarding FTX and Alameda:

“Prior to launching FTX, Bankman-Fried also started Alameda Research, one of the premier liquidity providers (market makers) in the digital assets industry. The potential conflicts of interest and embedded risks are large when a digital assets exchange also acts as the largest market maker and the product creator of innovative futures and index products. With a complex corporate structure, Bankman-Fried’s wallets could be tied to a number of activities taken on by FTX and/or Alameda.”

“You can sign up for a BlockFi account in seconds to earn interest on your Bitcoin with ‘no hidden fees,’ and they now have 225,000 clients who have deposited over $10 billion in assets on their platform. Presumably, that means you deposit Bitcoin, BlockFi pays you a yield, and they must be lending that Bitcoin out 1-for-1 to others who want to borrow Bitcoin at a higher rate—a simple Net Interest Margin (NIM) business right? There’s certainly nothing on the website that indicates anything differently, or anything that suggests there may be hidden risks involved in this process. Then again, you may wonder why a company in such a simple business line that should be immediately profitable has needed to raise over $500 million since inception from investors, and is, according to a Coindesk interview, just now ‘operating profitably for several months.’ Here’s a riddle: What’s a bank called that isn’t actually a bank and doesn’t offer FDIC protection? Answer: A secretive hedge fund.”

“… recently some of their practices have come under the microscope. The dirty secret is that there really isn’t that much demand to borrow Bitcoin. Plenty of customers want to earn a yield by lending their Bitcoin—but very few need or want to pay money to borrow Bitcoin. Most of the interest to borrow digital assets comes in the form of US-dollar stablecoins and ETH. As a result, you now have a very lopsided asset/liability mismatch (people lend BTC, but borrow USDT, USDC and ETH), and this mismatch needs to be managed very carefully to ensure that all interest can be paid and all principal can be repaid. Anyone who has seen BlockFi’s external capital raising deck has known for a long time that some of that yield shortfall has been filled using risky practices, including the very same Grayscale (GBTC) arb trade mentioned above that used to be a cash cow (when GBTC was trading at a large premium), but just recently started to become a loss leader (with GBTC at a steep discount to NAV). This didn’t become broad public knowledge though until BlockFi’s Form 13G was filed at the end of last year, showcasing that of BlockFi’s $10 billion in customer deposits, over $1 billion of this was invested into GBTC (BlockFi is the 2nd largest holder of GBTC).”

So did I see this coming? I mean, I guess—sort of, but not really. Certainly not to this extent. Suspecting loose organizational structures and being irritated that the media and other investors rushed to anoint a bunch of 20-somethings with no experience as genius investors and entrepreneurs is a lot different than suspecting outright fraud, deception, and incompetence. Specific to FTX, we certainly never held SBF, FTX, or Alameda on a pedestal and often steered clear of the well-known SBF-contrived “low float, high FDV” token launches, but we didn’t have any evidence or reason to assume foul play. In fact, the FTX exchange worked really well, and it was a super helpful counterparty in terms of capital-efficient trading. Their motto, “Built by traders for traders,” was actually true to some extent, as the exchange solved some of the operational challenges of investing in this nascent market.

I was skeptical of many of the companies in this space, but no more or less than I was with just about every new ecosystem entity with a short track record. Did I know enough to publicly bash any of these companies and perhaps prevent more people from getting hurt? Unfortunately, no. However, I have tried to be objective with the facts I did have, but it can be a slippery slope to spreading rumors without basis.

In the end, a select few correctly predicted the demise of some of the industry’s biggest players. There are also plenty of people who have, for years, unsuccesfully tried to take down companies and individuals with innuendos and false rumors. If you scream at enough trees, eventually, one might fall, but I’m not sure how impactful your role was.

The Latest Victims: BlockFi, Gemini, DCG, Genesis, and Grayscale

Following the FTX scandal, the market waited with bated breath for the next domino to fall. It didn’t take long to find the next victims, but again, we’re dealing with a combination of facts coupled with outright speculation. For example, crypto lender BlockFi is planning to file for bankruptcy (fact). Additionally, the largest OTC broker and lender, Genesis Global Capital, said that it temporarily suspended both withdrawals and new loan originations in its lending division while it assessed strategic options (fact). At its peak, Genesis had over $12B in its loan book, but following the brutal 2Q of 2022, its loan book shrunk to only $2.8B by the end of 3Q. The dominoes continued to fall as crypto exchange Gemini suspended withdrawals from its “earn” product (fact), which was essentially just a front-end pass-through service directly back to Genesis lending. And Genesis’ parent company, Digital Currency Group (DCG), is supposedly looking to plug a capital hole with an emergency $1B in rescue financing, leading to wild and inaccurate opinions about how the subsidiaries and trusts will be handled in a bankruptcy (speculation).

We’ll learn much more in the next few months as the bankruptcy proceedings and voluntary restructurings progress. For example, the FTX Chapter 11 first day declaration finally came out last week. It was filled with anecdotes about sloppy accounting, while the newly released docket is filling up fast with information about creditors and the movement of assets. If BlockFi files, it too will be a fascinating reveal. It has already been discovered that BlockFi took a $250M loan from FTX in the form of FTT tokens. If I’m interpreting (speculating) correctly, BlockFi already had an asset/liability mismatch and a massive balance sheet hole due to risky bets gone wrong, so they borrowed FTT in the form of a loan (without a deep enough market to sell), and therefore likely posted this FTT as collateral to take out more loans (probably from Genesis), thereby making both their asset/liability mismatch and their balance sheet hole even worse. All of the details will come out during the bankruptcy process.

For those new to distressed investing, this will be an interesting way to learn how a bankruptcy process works. I’d encourage everyone to read the dockets instead of relying on summary Twitter threads. Most of what I know about finance came from my experiences in 2008 and 2009. This distressed cycle in blockchain-based companies will become the cornerstone of many younger investors’ educational journeys. More importantly, after years of dealing with shadow banks and opaque (if not outright deceptive) business practices, the bankruptcy process will help validate or invalidate all of the rumors that have floated around for years in this space.

What Happens to Digital Currency Group, Genesis, and Grayscale Now?

By Mike Dershewitz, Head of Risk Committee

We are officially in the ‘trust no centralized counterparty’ phase of digital asset markets after FTX’s unsound balance sheet and misuse of customer deposits led to its insolvency. Suspicions are especially and rightly high for companies borrowing or lending to insolvent firms, such as how a single massive loan to Three Arrows caused Voyager to file for bankruptcy. The next domino looks to be the digital asset brokerage Genesis, which halted customer redemptions last week after disclosures that it had $175M exposure to FTX, among other delinquent loans throughout the year. While Genesis is experiencing a liquidity crisis (at a minimum), I want to analyze market concerns surrounding its corporate parent Digital Currency Group (DCG). Additionally, I will address stories in the market about potential ramifications for other DCG subsidiaries—the giant Grayscale Bitcoin and Ethereum Trusts.

DCG is the largest conglomerate in the digital assets space, with equity interests between asset management, lending, exchanges, mining, venture capital, and news. DCG was founded in 2015 by Barry Silbert, who previously founded the innovative employee options exchange SecondMarket. DCG’s crown jewels are the Grayscale trusts, which total $14.8B AUM and were the only U.S. exchange-traded digital asset product for years until the approval of Bitcoin Futures ETFs in late 2021. DCG also owns the digital asset broker and lender Genesis, African exchange Luno, digital assets news leader Coindesk, mining and node operator Foundry Digital, and significant token and venture investments. Based on the strength of these businesses, DCG raised $700M at a $10B valuation in November 2021.

As the corporate parent, DCG has worked to maintain solvency for its embattled Genesis subsidiary all year. Typically, parents own the equity in their subsidiaries and receive dividend income while not directly supporting their liabilities. Because I do not have full visibility into the accounts between DCG and Genesis, I cannot quantify any obligation that DCG has to Genesis’ liquidity or asset shortfalls. I don't know what liabilities have been fully "ring-fenced" to the troubled subsidiaries such as GGC (lending arm of GGT) and GGT, and I don't know what guarantees DCG has made on behalf of GGT. That said, DCG has contributed capital to Genesis on numerous occasions. First, when Three Arrows went into insolvency, Genesis reported a $2.4B loan to 3AC with a likely ~$500M loss, and DCG sent $1B to Genesis’ balance sheet (which is rumored to be an intercompany loan rather than an equity infusion). Second, when FTX filed for bankruptcy last week, DCG sent $140M to Genesis to negate the $175M shortfall. There are also rumors that Alameda allegedly repaid a big loan to Genesis—likely with customer funds—within 90 days of its bankruptcy, which may be subject to a clawback, making the hole at Genesis even larger. Lastly, the WSJ reported that DCG sought $1B in an emergency loan at the same time as the $140M injection to address a liquidity crunch. Whether from direct obligation or the belief that Genesis can once again be profitable, DCG has been a motivated parent.

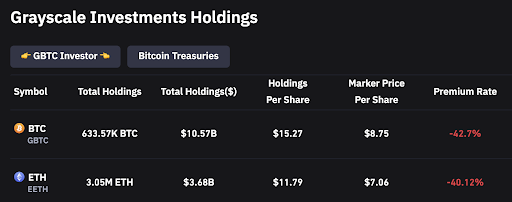

With this implicit support known, several market participants are hypothesizing that DCG will need to access liquidity from Grayscale, including potentially liquidating the Trusts, which would cause a lot of selling pressure of BTC and ETH. It makes sense to first review the Grayscale Trust structure to understand what levers can be pulled. The Grayscale Trusts today have $14.8B AUM, mainly consisting of $10.5B in their flagship Bitcoin Trust and $3.7B in their Ethereum Trust (ETHE). When investors historically purchased shares from the Bitcoin Trust, the Trust purchased Bitcoin at market and then issued exchange-traded secondary Trust shares (ticker: GBTC) that investors could trade after a six-month hold. Due to SEC regulations, there is no direct mechanism for Trust shares redemption outside of trading GBTC on the open market. Historically, GBTC traded at a premium to the underlying NAV of the Bitcoin controlled by the Trust, making the creation of new Trust shares highly profitable. Today, however, GBTC trades at a record 42% discount to NAV, making the creation of new Trust shares value-destructive and halting all primary inflows. DCG is the Sponsor of the Trusts and receives a 2% annual management fee, which is agnostic to whether GBTC trades at a premium or discount to NAV. While AUM is 80% below the $50B highs of April 2021, Grayscale remains a cash cow for DCG with over $300M of annual cash flow.

To emphasize the point: all of the assets in the Trusts are owned by trust holders and not by the Sponsor. DCG could choose to liquidate the trusts, but all proceeds would go pro rata to the holders of trust shares. DCG would therefore realize no liquidity from such a move. Further, even though some combination of Genesis and DCG owns a large stake in both GBTC and ETHE (from buybacks and from assuming the collateral of defaulted borrowers), it is unclear if DCG and Genesis mark these positions at the discounted price or at NAV. If it is the latter, they stand to gain nothing from closing the discount gap, as no mark-to-market gains would exist. Based on these facts, we believe that DCG choosing to liquidate the Grayscale Trusts is highly unlikely to occur in the near term. Clearly, the sell pressure of $14.8B in digital assets would weigh heavily on markets if DCG chose to liquidate the Grayscale Trusts, but I believe DCG has many more available options.

First, DCG should allow Genesis to file for Chapter 11 as a bankruptcy-remote entity if its funding hole is too great and it has no hidden liability. Second, if DCG is indeed compelled to continue supporting Genesis, it should look to other liquidity levers around Grayscale. DCG currently owns 28 million shares of GBTC (4% of the outstanding) and should sell this at market (and they may already be doing this, as GBTC and ETHE have been under pressure all week). To be sure, this is undesirable at present, given the extreme discount to NAV, but at least the market price pressure will be minimized. DCG can also sell off a portion of its Grayscale equity. Assuming $300M in annual net income, this cash flow stream should be worth at least $2.5B, depending on how a would-be investor/buyer values the longevity of this cash-flow stream. I am unsure of the financial needs at Genesis, but based on the WSJ’s report of a desired $1B fundraise, monetizing Grayscale equity may be a full solution to allow the subsidiaries to continue as a going concern.

But the question marks regarding DCG Holdings, its subsidiaries, various intercompany loans, and possible guarantors are more plentiful than the facts, given not everyone has access to DCG’s corporate structure and legal docs. (Here’s a good attempt based on what I know, but it’s not all-encompassing.) So this leads to a good trading environment whereby various scenarios and outcomes could play out. The Grayscale trust assets could trade back up to NAV if the Trust is liquidated, or the discount could widen further if one of the large holders (DCG, Genesis) become sellers on the open market. It is difficult to predict, but some of the possibilities include:

- Genesis files for bankruptcy as a bankruptcy-remote entity, in which case parent company DCG simply becomes a creditor, and there is no effect at all on GBTC, ETHE, or Grayscale

- DCG files for bankruptcy, Grayscale is sold and remains a solvent going concern, and Genesis and DCG sell their GBTC and ETHE holdings on the open market

- Grayscale is insolvent, and the Trust is somehow not backed—a low risk, but one that is permeating the market since Grayscale refuses to publish proof of reserves

- DCG or Genesis raise equity, in which case all subsidiaries are likely to continue as a going concern

- Nothing happens, and all of the rumors floating around about liquidity issues at DCG are false

Where Do We Go From Here?

That’s the billion-dollar question. The perception of digital assets as an investable asset class has always been polarizing. Now, the chasm between those willing to double down in support and those throwing in the towel will only grow deeper. We'll likely see many investors that are shutting down start to distance themselves from blockchain’s future prospects, while others who are still in business will reiterate its potential. For example, one goodbye letter from a shuttering fund-of-funds remains pretty optimistic about the long-term future (albeit very skeptical about the near-term fundraising and allocations). Meanwhile, Fidelity Digital Assets and Galaxy Digital hosted conference calls this past week for investors; according to sources familiar with the calls, both had more participants than at any point during the bull market. Bifurcation is coming fast.

In terms of markets, this is much tougher to assess. As we wrote last week, the zookeepers’ problems shouldn’t implicate the animals. Many protocols and tokens are unaffected and thriving due to the sharp increases in trading volumes and the flight from centralized exchanges to DeFi. Long-term, fundamental investing processes will likely yield strong returns in some assets that live to see the other side of this fallout. But structurally, it’s challenging to figure out where the next forced seller or incremental buyer may emerge. Moreover, while the news of the collapse of FTX is empowering digital assets skeptics, we will once again point out that all of the recent collapses in the blockchain ecosystem have been from centralized players and not decentralized protocols. While that sounds like an excuse from a crypto insider, a recent JP Morgan report echoed the sentiment. It is critical to recognize this difference.

But FTX, Alameda, Gemini, Celsius, Three Arrows, Genesis, BlockFi, Voyageur, Babel, and many more were all finance failures, independent of the assets being financed. Fraud and leverage could (and will) happen again in any aspect of the financial world as long as there are companies that can skirt regulations and condone reckless behavior.

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Director of Research

Hassan Bassiri, CFA - Portfolio Manager

Sasha Fleyshman - Portfolio Manager

Nick Hotz, CFA - Vice President, Research

Alex Woodard - Research Analyst

Bodhi Pinker- Research Analyst

Wes Hansen - Director of Trading & Operations

Kyle Doane - Trader

David Nage - Principal, Venture Investing

Michael Dershewitz - Principal, Venture Investing

Michal Benedykcinski - Research Analyst

Andrew Masotti - Trading Operations

Topher Macpherson - Trading Operations

To learn more or talk to us about investing in digital assets and cryptocurrency