What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

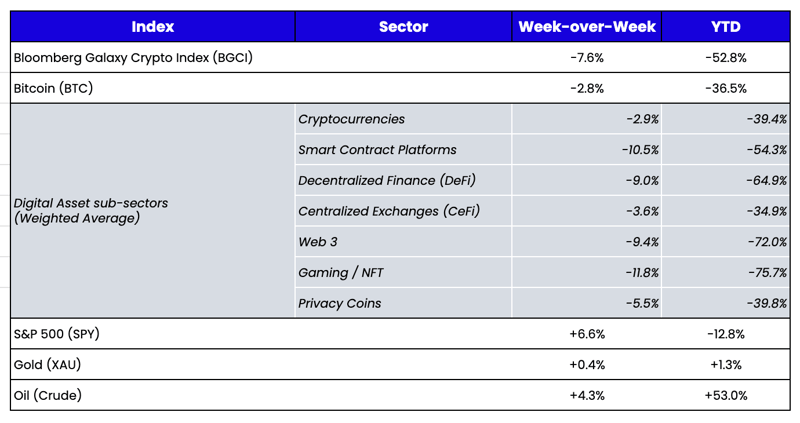

Week-over-Week Price Changes (as of Sunday, 5/30/22)

Source: TradingView, CNBC, Bloomberg, Messari

The Decoupling – But Not in a Good Way

Digital asset prices finally decoupled from equities, but not how most market participants had hoped. Digital assets failed to participate in the risk-on rally that sent the S&P 500 +6.6% (now positive MTD), oil +4%, Treasuries higher, and the dollar lower. The stark underperformance is most likely due to spillovers from the carnage caused by the Terra Luna collapse. Those ripple effects are still gripping the industry: lending has tightened, retail investors are hesitant, and funds are heavy cash. We’ve been on record that the recent high correlation to equities would likely not persist, as digital assets are still uncorrelated over longer-time horizons. Further, the very nature of the constantly changing short-term correlations is, by definition, what an uncorrelated asset looks like. Nevertheless, digital assets have now broadly declined for eight weeks in a row, and metrics are finally starting to decline due to apathy from the negative price action. As we begin to see an unthawing process in macro (inflation expectations declining, dollar declining, rates declining, and the Fed’s hawkish tone seemingly more cautious) which seems to be lifting equity spirits, it remains to be seen if digital assets will still trade like one giant “risk-off” asset, or if we’ll begin to see some differentiation again amongst sectors and tokens.

|

|

Netflix and Peloton Should Issue a Token Today

While most of the world focuses on today’s blockchain use cases (cryptocurrency and smart contract platforms), the apps that live on these blockchains will ultimately be far more impactful than the blockchains themselves. Most of these apps exist, but have yet to adopt a digital asset as part of their fundraising and customer bootstrapping, retention, and incentive programs.

For years we’ve foreshadowed a world that we think is inevitable—one where every company, municipality, university, and organization issues its own token. But like many new technologies and ideas, few want to introduce change to the status quo during times of prosperity. It’s only amidst struggles do we look to alternatives. Today, tech companies are struggling. They are struggling with earnings, with employee and customer retention, and with moat. For example, Netflix (NFLX) stock is down -71% from its all-time highs and Peloton (PTON) stock is down over -90% from its all-time highs. The companies face steep competition and have customer retention concerns. Issuing a token could address both.

Let’s first consider Netflix: most of us use the service, and most of us have a price in mind that we’re willing to pay for it. As long as the subscription price increases do not exceed what we’re willing to pay, we will continue to contract the service. Unfortunately, most of Netflix’s users do not care about Netflix itself; they simply care about the content and the ease of use—not the platform they use to access it. As a result, few Netflix customers feel brand loyalty and are unlikely to lock in future services by paying upfront in a meaningful way. Moreover, Netflix has over 220 million subscribers, but 80% of their shareholders are institutions. While it is difficult to measure exactly what that ownership/customer Venn diagram looks like, it’s clear that most of their customers are not meaningful shareholders. Whether or not Netflix succeeds as a business is not relevant to most Netflix customers, as there is no stakeholder alignment.

But a Netflix token, outlined in the example below, could solve many of Netflix’s issues. Netflix could issue a token with a fixed supply that cannot be altered. Of the 100% of tokens issued, the distribution could look as follows:

- 30% retained by Netflix for future issuance, held as an asset on the balance sheet

- 10% given away to Netflix employees for employee alignment

- 40% sold to Netflix fans, customers, and shareholders who want to profit off of Netflix’s success or simply lock in current subscription fees before price hikes

- 10% given away for free to all Netflix subscribers based on how long they’ve been members as a reward for sticky customer usage (similar to how Uniswap and others have distributed tokens)

The token would have hybrid properties, much like Binance Coin (BNB), which includes both a financial component predicated on the success of the business (BNB uses 20% of profits to buyback and burn tokens), as well as a utility function that acts as a member benefit reward (BNB token holders get fee reductions, can use tokens as collateral for derivative trading, and get first dibs on new token launches). For Netflix, it could look as follows:

- 20% of all Netflix subscriber revenues get distributed to all current NFLX token holders who use the token as a means of payment for the service.

- Essentially, Netflix turns every customer into a quasi-shareholder who benefits from the business’s success, and is more likely to evangelize to future customers on Netflix’s behalf.

- All NFLX token holders can receive discounts on NFLX subscription fees if they pay using the NFLX token

- Upon payment, some portion of these tokens that are spent get burned (therefore decreasing the supply outstanding of the tokens, turning NFLX token into an amortizing token)

- Further, they can incentivize longer-term customer payment plans and upfront purchases of the NFLX token by setting in advance future subscription price hikes and encouraging customers to pay in advance to lock in current prices:

- 10% discount on monthly subscription fees if you pay with NFLX token

- 20% discount on annual subscriptions

- 30% discount on 3-year plans

- NFLX token could also give customers/token holders exclusive access to new content, where you get a 1-week sneak peek on a season finale or early access to new content

- As token ownership becomes more common in society, Netflix could solve its subscription sharing issues by only allowing you to log-in to Netflix if you own the token—the blockchain is a public record-keeping service after all

By instituting these simple changes, Netflix can lock in revenue upfront from the sale of the tokens (booked as revenue for future services) and retain a valuable asset on its balance sheet in the form of unissued tokens. As a result, Netflix customers would become more loyal, sticky customers. Further, NFLX shareholders would give up a just small portion of earnings that they would make back in spades due to growing the overall pie of customers and profits. The demand for the NFLX token would be driven by expectations for future subscription price hikes (front-load purchases), by the dividends distributed to token holders (a simple DCF model could calculate the token’s worth), and by the demand for perks (intangibles that are harder to quantify). While NFLX stock currently has an $86 billion market cap, a NFLX token would likely have a market cap that matches or surpasses that of its share price due to unlocking the intangible value of Netflix’s business that can’t be captured solely by profits.

Peloton (along with every other customer-facing business) could, of course, do something very similar:

- PTON token gives you discounts on subscription fees

- PTON token holders get a share of revenues or profits of the business

- PTON token holders get exclusive access to new instructors, rides or features

- PTON token holders get exclusive access to races or other events that Peloton sponsors

The beauty of these customer-facing tokens is that they can morph as the company evolves. Unlike equity ownership, which only gives you the residual value of the business or potentially a cash dividend, token ownership can tap into all kinds of unique perks to retain and incentivize its members.

Once a few pioneer companies and investment banks start to tap into these additional sources of revenue and customer retention tools, every company will do it—from Disney to Starbucks to your local mom-and-pop store or restaurant. As token issuance grows, so will the ability to trade and monetize these tokens. While equity ownership and token ownership can certainly co-exist, you may even see some companies convert 100% of shareholders into token holders, thereby eliminating the shares of the business and turning token holders into actual equity owners. In some ways, token ownership redefines what “equity ownership” truly means.

We’ve already seen some companies flirt with these ideas: Starbucks has announced plans to issue NFTs, Bakkt has built a marketplace to trade airline miles and other reward points, and some companies have toyed with the idea of tokenizing their equity (rather than creating new hybrid tokens). Of course, all of these ideas can co-exist, subject to U.S. regulators providing a roadmap that allows companies to experiment with big ideas without the fear of breaking rules that don’t actually exist.

In the meantime, I hope some tech executive reads this and realizes that there is a solution besides watching its customers leave and their stock price bleed out.

Comparing LUNA and UST to Equity / Debt Recoveries in a Chapter 11 bankruptcy

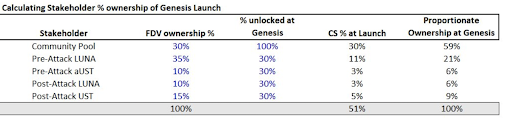

Last week, Terra Luna executed one of the fastest “bankruptcy restructurings” in history. Just weeks after an epic collapse which wiped out nearly $20 bn of UST depositors’ money and $40 bn of LUNA token holder value, Terra Luna 2.0 (LUNA) was released. The new LUNA token distribution is as follows:

Wait, what?

Let’s back up. The Terra blockchain itself was a perpetual machine, with virtually no costs and a structure that could run forever without the risk of running out of money and shutting down its services. Despite the massive loss of faith and value from the implosion, the blockchain still functions. And the applications built on top of this blockchain need to continue to run as well. Now, a blockchain can’t run without validators or miners—all of whom secure the chain and earn fees for doing so, so a new LUNA 2.0 token would need to be released in order to resurrect the chain, but the chain itself (meaning the code that makes it work) is virtually untouched. If you’ve ever heard the term “fork”, that’s essentially what this means. The code can be copied infinite times as long as the miners/validators agree to secure/mine that version of the chain, providing it security that makes users comfortable transacting on it.

In a typical bankruptcy process, there is a defined waterfall structure that determines how a reorganized company’s new equity value will be distributed to different existing pre-bankruptcy creditor groups—with customer claims, vendors, secured lenders, unsecured bondholders, and equity owners all taking part in the bankruptcy court process that determines who gets what amounts of the residual value in the reorganized business. Hats off to Matt Levine at Bloomberg, who beat me to this idea and as usual, articulated this in a way that no one else can.

In Terra Luna’s case, a very simple analogy is that UST holders were the “debt” in the system, and LUNA holders were the “equity”, meaning essentially no value of the reborn blockchain should go to old Luna (Luna Classic) holders until every dollar is repaid to UST holders. But it isn’t quite that simple with a reorg blockchain. UST was "debt-like," but it wasn't debt; LUNA was "equity-like," but it wasn't equity. Ultimately, while the fair thing to do would be to give UST holders most of the recovery/residual value of the new chain, it's actually pointless to do so because the UST stablecoin that thrived on the old Luna Classic blockchain is dead and not coming back. In contrast, the LUNA 2.0 chain may one day have real value only if new validators, stakers and application developers find value in the chain. Said another way, it’s better to resurrect the chain with long-term option value than to strip it of all future value by paying back fake debt. And that’s why only 25% of new tokens went to UST holders, whereas 45% went to old LUNA holders. Of course, this is what bankruptcy court is for—to establish rules to ensure that certain creditors are treated fairly. But bankruptcy court under Chapter 11 law is a painfully costly process that can take years to play out. The current Luna saga, by contrast, took just 2 weeks, and the new LUNA 2.0 token is trading well thus far, indicating that most participants (UST holders, Luna Classic holders, and new speculators) find this to be a somewhat “ok” outcome.

Is this better? Not necessarily. Though I’m not sure it's worse either. For now, it is a case study in the value of community. There are tons of Layer 1 “ghost chains'' with very few (if any) applications built upon them, yet these ghost chains still have tremendous value, often in the billions of dollars (e.g., EOS, ADA, ETC, XTZ, and ICP). These chains have value because they are call options, and if you understand the Black-Scholes options model, 3 of the 5 inputs to option price are:

- Time

- Volatility

- Interest rates

In a low interest rate, high volatility environment, a ghost-chain with no chance of bankruptcy and thus an infinite time horizon has a lot of option value. But most of these other ghost chains start with no prior community or branding, and the onus is on the founders and their marketing teams to build a community and a buzz from scratch. In Terra Luna’s case, this reorg Luna 2.0 chain is starting with an already well-established (albeit tarnished) brand, and a massive community. The new Luna 2.0 token is currently valued at $9 billion (fully diluted). While that sounds insane, and it very well may be, it may also signal what the “base case” value of a blockchain is if it has a built-in community. We can now use LUNA 2.0 to determine what a network is worth, all else equal, which, in a weird and twisted way, may end up increasing the value of all other blockchains as a new floor has been set.

We strive to introduce valuation techniques for different types of digital assets, especially when their value is derived from both financial and utility values. Previously, we’ve discussed how you can isolate the utility value of a token in certain instances, like when futures prices and spot prices diverge due to the tangible value created by physically owning a token (e.g., OMG in 2021 and BNB in 2020). Thanks to Luna, we can now separate a blockchain’s financial value derived from transactions and fees from the “base value of a network” based on community alone. And based on where LUNA 2.0 is trading today, the entire Layer 1 smart contract platform sector is now severely underpriced, relatively.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Director of Research

Hassan Bassiri, CFA - Portfolio Manager

Sasha Fleyshman - Portfolio Manager

Alex Woodard - Research Analyst

Nick Hotz, CFA - Research Analyst

Bodhi Pinker- Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Defi Trader

David Nage - Principal, Venture Investing

Michael Dershewitz - Principal, Venture Investing

Michal Benedykcinski - Research Analyst

Andrew Masotti - Trading Operations

Topher Macpherson - Trading Operations

To learn more or talk to us about investing in digital assets and cryptocurrency