What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

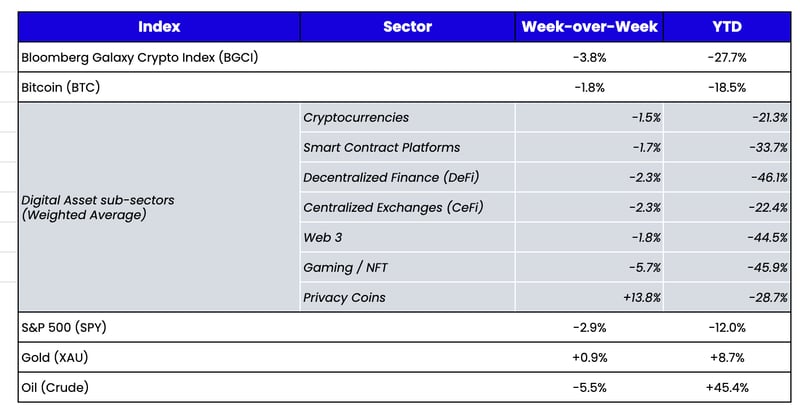

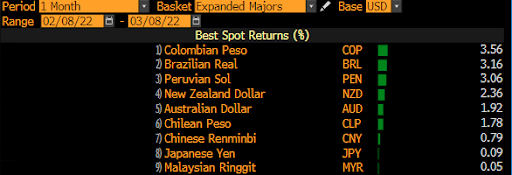

Week-over-Week Price Changes (as of Sunday, 3/13/22)

Source: TradingView, CNBC, Bloomberg, Messari

We’ve spoken with institutional and individual investors about digital assets for almost five years now. While everyone’s journey is different with regard to timing, most have a similar basic path—from “complete dismissal” to “lukewarm but willing to learn” to “I get it, and I want to invest.”

Contrary to what you might expect from the negative price action over the past three months, our meetings have never been more constructive. When I casually tweeted about our bullishness on expected new entrants and inflows, we were met with a lot of responses asking us to elaborate further. So we did elaborate, in the third section of today’s writeup, diving deep into the main analogies, one-liners, and concepts that we use in meetings with new investors that often lead to that “aha moment.” But first, let’s discuss the macro and micro market conditions weighing on prices today.

Relative Value

Digital assets declined last week, broadly, in line with continued equity weakness. The “it’s all one risk trade” train continues amidst endless war headlines and a looming recession (as predicted by rising energy prices and a flat yield curve). While it’s felt like “down only” for most of the year, the broader digital assets market is pretty close to unchanged since the crash (week ending January 24th), while equities, bonds, and most currencies have fallen further over this period. Digital assets acted as a leading indicator in November and December before the bond and equity markets really suffered any damages, and their current resistance is potentially acting as a leading indicator again. Bond, equity, and currency indexes are simply playing catch-up.

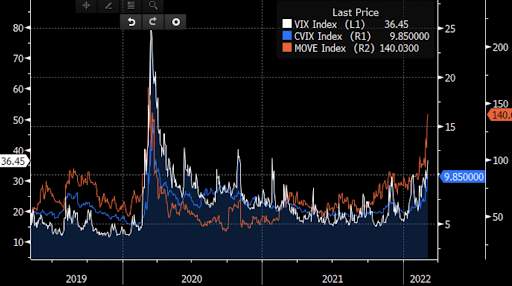

Volatility markets are urging risk reduction everywhere

Source: Jon Cheesman, FTX, in an email to clients

Source: Jon Cheesman, FTX, in an email to clients

Amidst broader carnage, it's interesting to look at what influenced the pockets of relative strength. Bitcoin is now down roughly the same amount as the Nasdaq YTD (-18%), though Bitcoin’s annual returns of +93%, +300%, and +60% the last three years dwarf the gains of the Nasdaq over the same period (+38%, +47%, +26%). High up capture with similar down capture is a metric that will undoubtedly be noticed by investors, even if correlations remain stubbornly high in the near term. Said another way, if two “assets” have the same downside risk, but A has much more upside risk than B, you’d want to own A. Simple.

Similarly, in past episodes of stress in financial markets, you would not have expected these emerging market currencies to outperform the majors, but with the Ruble, the Euro, and the Canadian dollar showing weakness as their monetary and government policies are thrown into question, it’s become harder to identify a true safe haven.

Source: Bloomberg

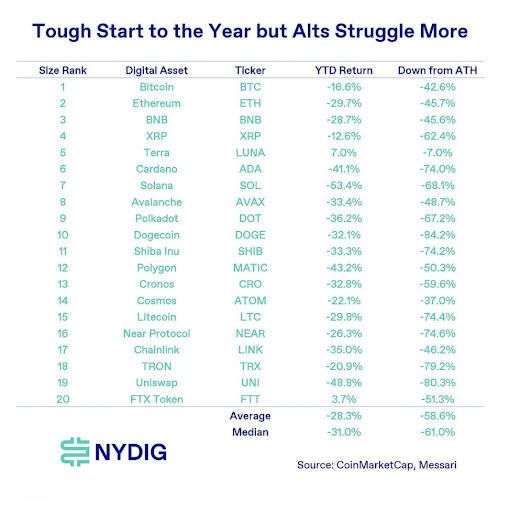

And of course, it’s no secret that Bitcoin and privacy tokens have outperformed Layer 1 protocols, gaming, Web 3, and Defi this year. It's also not surprising that amortizing tokens like LEO, LUNA, and FTT have significantly outperformed all other digital assets. In a year where gains (outside of commodities) have been very hard to come by thus far, these “relative winners” take on even greater importance. Dispersion is back, and digital assets investing has once again shifted back into what you own, not if you own.

Looking ahead, there are three larger factors that likely matter most for longer-term US equity and digital asset investors:

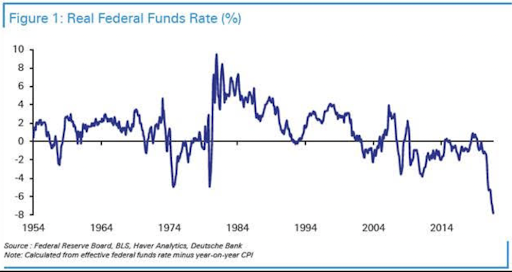

- No matter how much the Fed and other central banks raise rates, real rates are still incredibly negative, making holding cash and investing in fixed income challenging.

- Following the sanctions against Russia, most of the global investing world is spending a lot of time determining which regions are investable or not; that means money is likely to pour into US equities, real estate, and digital assets.

- Per 1 and 2 above, cash levels are at the highest in history; when investors decide to put that cash back to work, there are far fewer places to reasonably invest than usual. This will put added upward pressure on the few investable areas.

Another Overhang Removed: Washington

Last week, President Biden released the long-awaited digital assets executive order. Many are calling this a pivotal moment for the industry, even though it will undoubtedly lead to more questions than answers and certainly won’t lead to any action in the short-term. Perhaps most importantly, it indicated a clear future for digital assets in the U.S., which removed another barrier to entry and another overhang for institutional investors.

Galaxy Digital best summed up key takeaways from the EO:

“The existing regulatory framework has been fragmented and disorganized, with states, the CFTC, SEC, IRS, and US Treasury Department each implementing different and sometimes contradictory approaches. As a result, both market participants and policymakers have been calling on the government to provide more regulatory clarity with agency responsibilities better defined. In light of the lack of clarity in current laws, the SEC and DOJ, for example, have been approaching regulation through enforcement actions and fines. FinCEN considers cryptocurrencies to be money considering and thus subject to money transmission rules under the Bank Secrecy Act; IRS considers it to be property subject to capital gains taxes. The CFTC says Bitcoin and Ether are commodities, but the SEC chairman believes that many cryptocurrencies are securities. While all these issues surely will not be sorted by this process, Wednesday's EO nonetheless marks an important step towards a more cohesive, coordinated approach for government policy on the growing cryptocurrency industry. Most importantly, the framing of the EO struck a surprisingly balanced tone that acknowledged the wide adoption and the potential benefits of digital assets. It suggested for the first time that the Administration was accepting of the technology, recognizing its importance in our economy as a new asset class and its potential to improve on the global positioning of the US. The EO calls to examine the differences between different crypto assets which is meaningful because not all crypto assets should be regulated the same way. With acceptance coming top-down from the Administration and bottom up with growing adoption among Americans, policymakers can then direct their attention to more productive and conducive discussions on how to best harness the technology and unlock its potential for the best interests of the nation and its constituents.”

The tone of the executive order is constructive; it acknowledges that digital assets are significant enough to warrant a high level of attention from the U.S. government. The market braced for bad news that did not materialize, which made this announcement a net positive.

The “Aha Moment” for New Digital Asset Investors

As previously discussed, a fly on the wall in our meetings with institutional investors would come away extremely bullish on the future of digital assets. Below are some of the one-liners, analogies, and explanations we use in investor meetings. With an almost 100% hit rate, these discussions lead to an “aha moment” for someone in the meeting.The light bulb goes on; they begin to truly understand why digital assets have immense value and why this is an investable universe in which they need to have an allocation.

Stakeholder alignment:

- Digital assets are the greatest capital formation and customer bootstrapping mechanism we’ve ever seen that fully aligns all stakeholders from customers to founders to passive token holders.

- Customers and shareholders are often mutually exclusive in the traditional debt and equity world. For example, McDonald’s (MCD) customers are rarely MCD shareholders, and MCD shareholders are not McDonald’s target demographic. However, in the digital assets world, this gap is bridged. All customers are encouraged and incentivized to be token holders, thereby sparking motivation to help the company grow because they are being paid (via quasi-equity) for their efforts. This creates full stakeholder alignment, sticky customers, and evangelists.

- DoorDash and Airbnb are examples where this is NOT the case. DoorDash only exists because everyday people cook, eat, and deliver food, but only a handful of venture capital investors share in DoorDash’s financial success. Similarly, Airbnb only exists because of people who own houses and people who like to vacation. Yet none of the people who make Airbnb and DoorDash successful have any economic incentive to see these companies succeed. Had these companies been recapitalized with tokens sold or given away to early customers, their success may have been even faster and more remarkable; it certainly would have resulted in more wealth equality.

Token structure – hybrid instruments that are part quasi-equity with financial upside and part utility or member benefits program:

- Imagine if Amazon Prime’s customer loyalty and utility functions (free shipping, Whole Foods discounts, free movies and music) and Amazon stock (financial upside via profits) were combined into one entity: members would receive benefits that continue to improve over time in addition to 20% of top-line revenue.

- This is, effectively, what Binance did with their BNB token. BNB holders received member benefits (starting with discounts for trading and evolving into the ability to use BNB as collateral to trade derivatives and being first in line for new IEOs), but also got financial rewards in the form of 20% (loosely) of profits being used to pay down tokens in the form of a “buyback.” This made BNB a hybrid instrument—part utility, part financial. There is strong reason to believe that Binance became the fastest growing unicorn in history (enterprise value now over $300 billion) largely due to this incentive structure.

- Soho House, Equinox, and Netflix are good examples of where this model will head in the future. All are membership-driven, but members don’t get any equity, nor do they have a say in governance. Soho House could probably start owning its real estate if it issued tokens to members and gave them upside in real estate-backed tokens. Equinox could expand internationally if it gave its members some kind of ownership. Netflix could convert membership into tradeable tokens that could be freely traded or redeemed for service. In this model, every company, university, municipality, and entity will soon find a way to introduce a token into its capital structure.

Yields in digital assets come from 2 places:

- A shortage of working capital in the ecosystem - Digital asset pipes and workflows are still largely walled off from the traditional bank/brokerage system, and there is no prime brokerage in digital assets. This means all of the money printing and reverse repo that has led banks and lenders to be flush with cash has not yet trickled into the digital asset ecosystem. This industry is essentially cash-starved despite cash being abundant. Further, with fragmented exchanges and liquidity, market makers are always looking for capital to make deeper markets. This shortage of working capital leads to demand for assets to borrow (high lending rates) as well as steep curves in the options and futures markets since both are capital-efficient ways to increase risk.

- Rewards - token issuers reward early participation in a network, usually with “equity-like” rewards in the form of their token for performing some action (providing deposits, liquidity, or other actions). Two decades ago, Facebook famously tried to get all of its customers to like 10 posts and follow 10 friends as they learned that these actions would lead to sticky customers. They did everything they could to get customers to perform these actions, but Facebook did not reward users for these actions; instead, Facebook essentially tricked people into action via growth hacks. Today, those actions could be incentivized by giving power users Facebook “shares” (tokens). Rewards like these provide yield to investors and explain why digital assets are great customer bootstrapping mechanisms.

Valuation:

- Digital assets can be valued using traditional financial methodologies (cash flow analysis, dividend yield models, relative value) as well as newer techniques unique to digital assets and technology (Metcalf’s law, supply/inflation sinks). We always start our valuation processes with roots in traditional finance but adjust and adapt along the way. Our recent analysis of Layer 1 blockchains as both businesses (BaB) and nations (BaN) is a good example of our creative thought process.

- Think of Layer 1 smart contract blockchains as an “app store.” On day 1, they have no value other than the speculative value of what might one day be built upon it, but over time, as apps are developed and released, real transaction value and revenues accrue to the app store. These apps can be in various sectors—for example, on your iPhone, you have banking apps, games, maps, and more. On Ethereum, you have DeFi, Gaming, NFTs, and Web 3. Once an app store (Apple iOS / Ethereum) begins to succeed, other app stores pop up (Solana, Avalanche, Fantom, BSC, Terra Luna / Samsung Galaxy, Google Android). This trajectory highlights that a multi-chain world is inevitable.

- Rather than waiting for 10-Qs, 10-Ks, and 8-Ks that are 3+ months late, we can actively monitor KPIs in real-time due to the transparency of blockchain. The majority of digital assets have revenues and cash flows that can be used to derive value.

- Digital assets are redefining what “equity” means. Equity is a claim on cash flows/profits, whereas tokens are a claim on customer growth.

Tokens we frequently use as examples of how digital assets work:

- Binance Coin (BNB) due to the simplicity of the buyback and burn model combined with the customer utility.

- Sushiswap (SUSHI) and Uniswap (UNI) as examples of decentralized versions of the same basic company with clear cash flows—one of which pays a dividend and the other doesn’t.

- Nexus Mutual (NXM) as an example of an asset-backed token and a very easy to understand business model (insurance). The tokens are backed by the capital pool, and the tokens trade at 50% of book value.

- Chiliz (CHZ) because it is a real-world application of blockchain; fan tokens are issued on behalf of teams, but CHZ itself acts as the underwriter and broker/dealer for the fan tokens, generating revenue for these services.

- Axie Infinity (AXS) due to the simplicity of gaming and an easy-to-understand cash flow generative business (in-game asset transfers).

- All of the above can be valued using traditional metrics and are simple business models to understand. We often talk for hours without ever mentioning Bitcoin or Ethereum—not because they aren’t good assets, but because they are much more difficult for traditional investors to understand.

Market parallels to traditional finance:

- Bitcoin (BTC) and Dogecoin (DOGE) are two examples of cryptocurrencies that have very few (if any) properties that can be valued and thus tend to move at random. But the media focuses so much on these two tokens that most newcomers think that all digital assets are similar. Imagine if every new entrant to the stock market learned about AMC and GME first—almost no one would invest in stocks because AMC and GME are not trading based on value. The difference is that everyone in the equity markets knows that AMC and GME are sideshows, so they can dismiss them as outliers rather than extrapolate those events to the broader market. Digital asset investors would be wise to do consider BTC and DOGE in the same vein so they can focus on other types of digital assets (pass-throughs, asset-backed tokens) that have different properties than cryptocurrencies. We recently constructed a taxonomy to help investors understand the different types of digital assets.

- There are many parallels between digital assets and traditional markets. Still, digital assets are more similar to fixed income than they are to commodities, currencies, or equities in that trading occurs with a large, fragmented dealer and exchange community, creating inefficiencies and pockets of high correlation on low volumes.

Inevitably, some of these explanations begin to resonate with new investors. Over the past six weeks, our society has discovered that money and stocks are not an asset—they are liabilities owed to you (typically by a broker or a bank). Whether or not you can ensure these entities pay you back in full is now in question due to recent activities in Canada, Russia, and the London Metals Exchange. This uncertainty has become a wide-reaching advertisement for ownership of bearer assets like digital assets.

We hope this sneak peek behind the curtain was helpful.

What We’re Reading This Week