What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

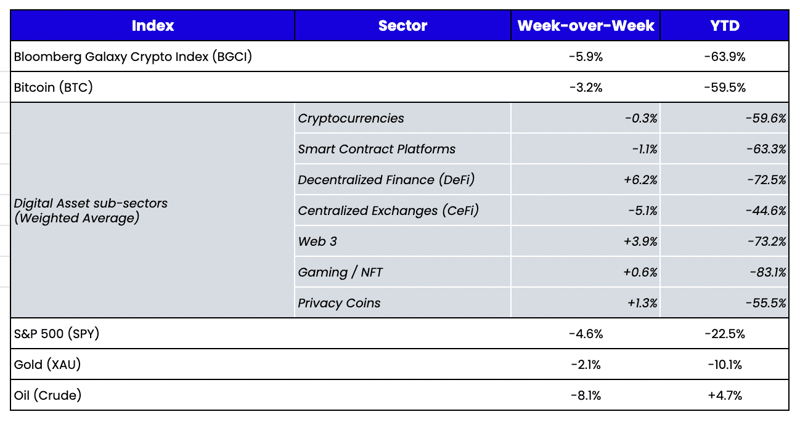

Week-over-Week Price Changes (as of Sunday, 09/25/22)

Source: TradingView, CNBC, Bloomberg, Messari

Powell Slams Markets

Fed Chairman Jerome Powell did not mince words during his Jackson Hole speech a few weeks ago, and he continued the hawkish rhetoric last week following the third consecutive 75 bps rate hike. We knew rates would keep increasing, and we learned from Powell's post-FOMC decision speech that we would get there faster than the market had expected and remain there longer than expected. The revised dot plot indicates board members expect to take rates to 4.625% in 2023, up from the 3.75 projection at the June meeting. This led to:

- Equities posting back-to-back -5% weeks for the second time in the last three months;

- Gold continuing its free fall;

- Oil falling to almost unchanged YTD;

- Credit spreads widening;

- Interest rates rising to new YTD highs; and

- Digital assets generically falling -3-5% (though digital assets outperformed equities on a beta-adjusted basis, and quite a few tokens like XRP, ALGO, APE, and HNT generated substantial gains throughout the week as idiosyncratic events continue to trump macro).

It will never cease to amaze me that trillions of dollars move on the Fed’s new estimates, even though the Fed has been dead-wrong about inflation and rate estimates for over a decade. First, they incorrectly anticipated inflation would rise above 2% post-financial crisis when instead, it was stuck below there for a decade. And then, of course, completely whiffing on their transitory stance once inflation was already out of control. Regardless, they continue to talk tough, and markets are starting to believe them again.

“Dot Cryptos”

While it has become a convenient narrative to assume that digital assets’ fates are tied to macro, the reality is this is a very short-lived correlation that only applies to a few bellwether cryptocurrencies like Bitcoin. The future success or failure of digital asset investments will be more closely tied to user and app growth than to dot plots. But with the ETH Merge in the rear-view mirror and the FOMC stranglehold transparently and clearly stated, what will be the next catalyst to drive digital asset prices? To answer that, we must acknowledge how bad the data is and compare it to data points suggesting trends may reverse soon.

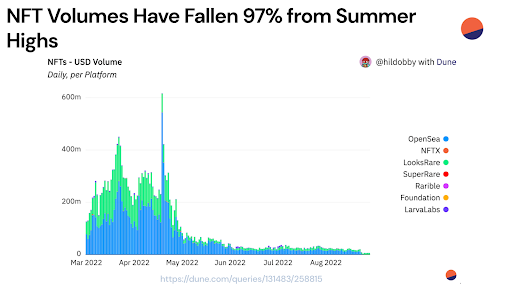

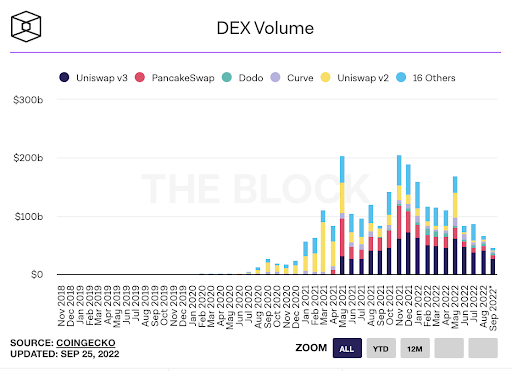

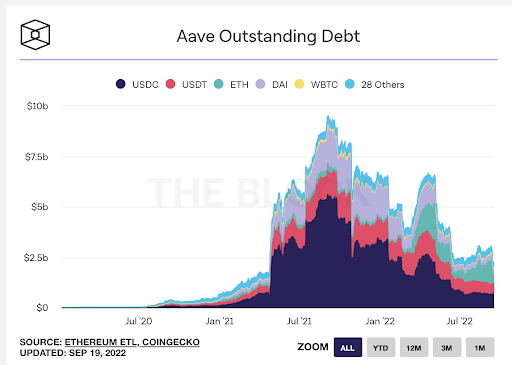

To start, the rise of DeFi, stablecoins, and NFT transactions was the backbone of the 2020 and 2021 rallies. Now, 2 of the 3 are seeing significant declines in usage and transactions.

- NFT volumes are -97% from early 2022 highs:

- Decentralized exchange volumes are back to early 2021 levels:

- Lending activity has all but dried up, mainly due to the failures of centralized counterparts and the lower yields offered in DeFi applications, which dampen demand for leverage.

Overall, this isn’t a great backdrop. Most digital asset projects today are still highly levered to users, transactions, and volumes, and these 3 metrics are down. On the flip side, many data points suggest the end of this decline may be right around the corner.

To start, let’s state the obvious: investment dollars lead to better products, and better products lead to more customers—and there has been a flurry of investment into blockchain-based companies and projects from VCs and public companies.

Seeing investments from non-crypto native investors is extremely important. But, to understand the significance, let’s take a step back.

The dot-com boom was originally fueled by the launch of companies that would not have existed without the Internet. For example, Amazon, eBay, and Priceline were infrastructure companies that did not exist before the Internet made their business models possible. Today, of course, every company is a “dot-com,” including those around decades or a century before the Internet. Domino's Pizza is an Internet company. Disney is an Internet company. JP Morgan is an Internet company. But it would be ludicrous to call your company a dot-com now because it is assumed.

In the same vein, most digital asset protocols and companies today are “dot cryptos,” meaning they only exist because of the advent of blockchain technology and only focus on utilizing blockchain: Chainlink, Binance, Uniswap, Lido, Chiliz, for example. While the organic growth of “dot cryptos” has been impressive (Binance, for instance, has an estimated 28 million daily active users), existing companies experimenting with blockchain usage will likely onboard way more users to blockchain apps and wallets than any organic blockchain project. In the last few months alone, we’ve seen the following examples of adoption:

- Starbucks unveiled a platform to allow employees and members of its rewards program to earn and purchase digital collectibles that will unlock access to new benefits and experiences on the Polygon blockchain.

- Ticketmaster tapped Flow blockchain to let ticket issuers issue NFTs.

- Consumer electronics company LG is building an NFT marketplace as a feature on a range of its TV on Hedera.

- U.S. investment firm KKR has made its Health Care Strategic Growth Fund available to a broader range of investors via representative tokens on Avalanche.

- Sweatcoin, a popular “walk-to-earn” Web 2 app with nearly 100 million active users, tokenized a part of its business on the Near blockchain. On just the first day of the airdrop, Near saw more than 1 million active addresses. It was one of the most active days in the blockchain’s history and more than twice the number of users Ethereum had. As 13 million people downloaded the new Sweat Economy app on Near— likely the largest onboarding of users to Web 3 on record—we're likely to see further heavy usage of the chain going forward.

So while today’s data looks bleak, there is hope—if for no other reason than existing communities of users and customers are much easier to port over to blockchain apps than it is to create organic demand.