What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

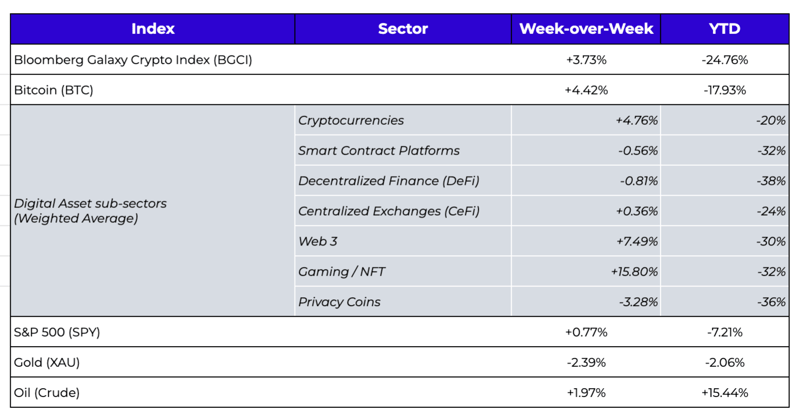

Week-over-Week Price Changes (as of Sunday, 1/30/21)

Source: TradingView, CNBC, Bloomberg, Messari

Drawing Parallels to Past Sell-Offs

Macro concerns have dominated returns across most risk assets year-to-date, and last week was no exception. Fears of inflation-induced profit margin declines, Powell’s hawkish testimony, and the increased geopolitical conflict in Ukraine dominated price action. Yet a late Friday equity rally bucked the directional trend, giving markets some much-needed relief even as the U.S. Dollar rallied for the 5th straight week (+1.7%), closing at its highest level since July 2020.

Still, broadly, equities are having one of their worst starts to a year in decades. Naturally, investors are now digging into the historical vaults, attempting to draw parallels to prior market and macro environments similar to today. For example, earlier this month, the VIX rose +50% in a single week, leading to this beautiful chart that suggests the equity market tends to rise substantially following short-term volatility spikes. This chart shows that allocations to tech stocks are at the lowest level since December 2008, which just happened to be the bottom of the global financial crisis and preceded a 1400% gain in the Nasdaq over the next 13 years. The interconnectedness of tech stocks and digital assets starts to shine through as well, with some eerie similarities to the tech bubble of the early 2000s. In an internal Arca discussion this weekend, these parallels were revealed:

“On January 30, 2000, 12 of the 61 ads for Super Bowl XXXIV were purchased by dot-coms (similar to today’s Crypto.com and FTX ads). In 2000, Fed Chairman Greenspan raised interest rates several times, which many believe caused the dot-com bubble burst (similar to today’s forthcoming tightening regime by Powell and company). That same time, MicroStrategy (MSTR) announced a revenue restatement due to aggressive accounting practices—MSTR stock price, which had risen from $7 per share to as high as $333 per share in a year, fell 62% in a single day (similar to today’s MSTR issues with Bitcoin accounting). On Friday, April 14, 2000, the Nasdaq fell 9%, ending a week in which it fell 25%, as investors were forced to sell stocks ahead of Tax Day (similar to this month’s 10-15% slide).”

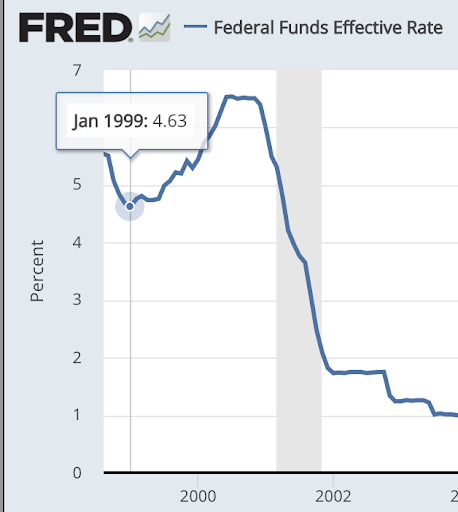

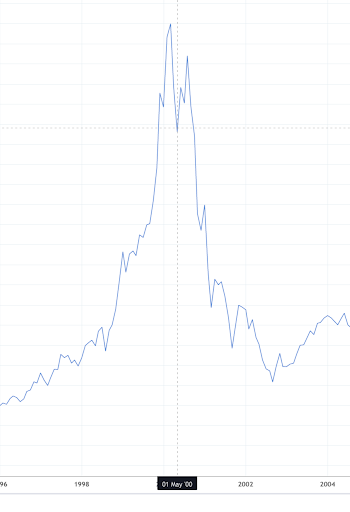

Of course, the main difference is that the Fed started raising rates in early 1999. The Nasdaq rallied over 100% more over the next 1.5 years, while the Fed raised rates before equities finally crashed in late 2000. The recession (Gray box) started in 2001 when rates were already heading back down, and the yield curve was already inverted. Today, the yield curve is still steep, GDP is still growing, and the Fed hasn't even begun to raise rates yet. So it would be historically unprecedented for risk assets to go down this year, let alone at the pace it is happening. Moreover, even once the Nasdaq did start finally sliding in April 2000 per the above, the Nasdaq then rallied almost back to the highs from May 2000 to Sept 2000 before finally dipping again for good in late 2000, nearly 2 years after the Fed began raising rates.

Source: Fed Funds Rate via FRED / Nasdaq (NDX) chart via TradingView

Regardless, the point remains—investors are on edge, tech investors are really on edge, and digital asset investors are on suicide watch. And in today’s market, every reaction happens at exponential speed. For example, courtesy of our friends at Galaxy Digital, almost 90% of the top 200 non-stablecoin digital assets by market capitalization are down more than 50% from their all-time highs, with the average –73% and the median –77%. Most of these all-time highs were achieved in the past few months. That’s quite the sell-off for an industry that grew 300-1000% across most metrics last year. Similarly, 40% of NASDAQ-listed stocks are also down more than 50% from their 52-week highs. Markets have never been so short ahead of a Fed tightening cycle.

It seems clear at this point that one of our 2022 predictions is about to get tested. We stated: ”We will NOT see a broad-based ’end-of-the-cycle’ decline in digital assets,” with a heavy emphasis that, “We may continue to have steep, quick, highly correlated corrections, but as we’ve seen throughout 2021, certain assets and sectors will bounce back faster and stronger than others.”

Well, we got “steep and highly correlated” right; whether or not we get ”quick” and “thematic bounces” remains to be seen.

DeFi’s Beauty Shines In the Face of Wreckage

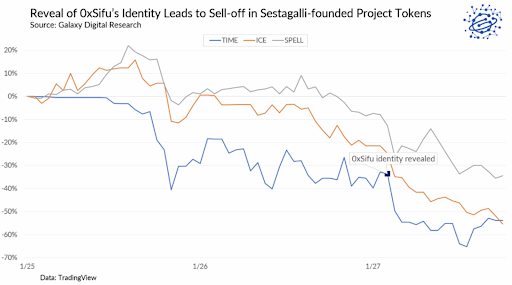

The Chief Financial Officer of popular decentralized finance (DeFi) protocol Wonderland was revealed as a convicted scammer and former executive of Quadriga. Michael Patryn, who went by the pseudonymous handle “Sifu” and worked directly with prominent DeFi founder Dani Sestagalli, had oversight over a treasury of nearly $1 billion. Though this story is about one individual and one DAO, the ripple effects were felt across DeFi because of the interconnectedness of DeFi applications and the immense influence of a handful of really successful DeFi developers and founders (like Sesta).

In a very abridged summary, MIM, the asset-backed stablecoin of the Abracadabra protocol, has a massive MIM-UST pool on Curve—the decentralized exchange that focuses on stablecoin trading. These incentivized Curve pools accounted for most of the minting of UST (the stablecoin of the Terra Luna/Anchor protocol ecosystem), whose rapid growth ($11 bn outstanding) helped drive the price of LUNA higher over the last several months. As LPs pulled assets out, TVL across Terra Luna dropped, as did the price of LUNA, and Curve’s TVL dropped as well, while all of the tokens in the Abacadabra/Sesta ecosystem (SPELL, TIME, ICE) fell 30-70%. Meanwhile, prediction markets popped up, betting that UST will lose its peg. Dealers were inundated with UST put buyers, and FTX even spun up a UST perpetual future market so traders could short UST. SUSHI, a completely unrelated DEX that was in the process of integrating Sesta and his team (but had not yet begun), also became part of the collateral damage. A historical chain of events that led to billions in losses started with the doxing of an individual. He indeed committed terrible crimes, but as of this writing, he has not been accused of any wrongdoing concerning all of the assets/projects mentioned above.

Source: Galaxy Digital

Now, this sounds bad, and the media has had a field day talking about the risks of DeFi. In fact, it's not dissimilar to a story from last year when Mark Cuban was “rugged” on another high flying, super risky, and experimental DeFi token, even though Cuban admitted to not doing any research before engaging with this protocol. And then there’s Congress, doing its best to shine the light on the tiny corners of digital assets that pose the most risk.

But here’s where it gets positive. Bad things occasionally happen in digital assets, just like corporate fraud in traditional markets (Madoff, Enron, Worldcom, Theranos, etc.) The difference is that corporate scams are usually elaborate and go on for years before being uncovered. By contrast, in digital assets, most of these events rise and fall within weeks, and any wrongdoings are discovered immediately by amazing DeFi onchain detectives (like those that identified SiFu’s misdeeds). That cannot be understated: the onchain detectives of DeFi are doing exceedingly more positive and real-time self-policing of this industry than any regulator will be able to do. As a result, most of the issues within DeFi are either very easy to avoid with even a shred of due diligence or discovered immediately due to the public records of blockchain. Thus, simple rules of thumb can be:

- Don't buy things you don't understand

- Understand who the founding teams are and their motivations

- Be careful engaging with super early-stage products without a long track record

- Listen when someone uncovers some important data

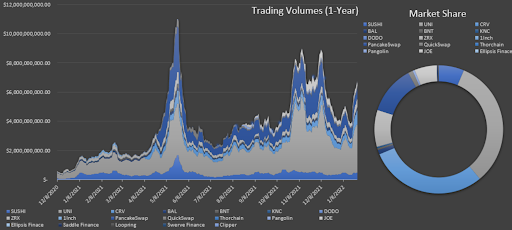

For those who ignore 1-4, you can make a lot of money or lose a lot of money, but it would have nothing to do with blockchain or digital assets—it pertains to human gambling psychology. For those who aren’t here to gamble, DeFi simply works. DeFi’s beauty was further on display with yet another violent stress test caused by deteriorating market conditions where DeFi applications not only performed brilliantly without hiccups, but thrived. While traditional markets are still a government-sponsored house of cards, DeFi is left to sink or swim all on its own—and the protocols and applications are swimming effortlessly amidst the storm. Total Decentralized Exchange (DEX) volumes grew 67% week-over-week to $52 billion. This growth had a lot to do with the volatility of the markets and MIM/UST concerns. Curve had its highest volumes to date last week, with $2.2 billion in volumes (Curve's largest volume month to date). The rest of the sector also performed well, with Sushi, Uniswap, Balancer, and Curve's volumes all up 41%, 78%, 138%, and 150% respectively WoW. Remember in May 2021 when DEX volumes dipped from all-time highs and everyone (mostly the media) freaked out about the end of growth? Well, the last four months have seen double the volumes of last summer’s “dip,” yet there don’t seem to be any sensationalist headlines about the recovery and renewed growth.

Similarly, total decentralized derivatives volumes grew 72% WoW to $22 billion with dYdX up 78% WoW.

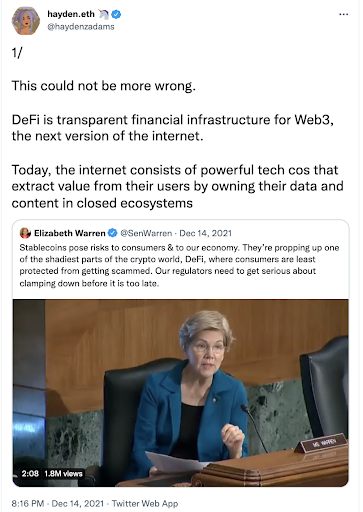

Yet you’ll never hear about the growth, the flawless execution without downtime, or the amazing ability for these protocols to run uninterrupted even amidst drama from founders/developers and declining asset prices. But this should be the focus. There is a thriving underlying ecosystem despite one-off scams, hacks, and ousted bad actors. So instead of celebrities crying foul and calling for more regulation when they, in fact, messed up, we should be celebrating how amazing this technology is. Hayden Adams, the creator of Uniswap, said it perfectly in a Twitter thread:

“Web3 empowers artists, gamers, writers, builders, journalists, and other creators. It gives them the tools to coordinate, own, monetize and exchange the value they create directly, removing their dependency on harmful, captured ecosystems we see on the internet today…DeFi is the backbone that makes this all possible. Unsurprisingly, entrenched interests that profit greatly off extracting value from closed ecosystems would love to see it fail. Misinformed attacks on Web3 and DeFi will ultimately be on the wrong (and losing) side of history.”

The world of DeFi will only get bigger and stickier as off-chain assets are integrated. Soon, individuals and companies will plug cash flows and real-world assets into DeFi ecosystems as a routine part of financial transactions. Predatory pay-day lending will go away in favor of daily loans and micropayments. Receivable financing for businesses will move on-chain as sellers borrow against their inventory to unlock working capital. Every owned asset will become more productive. So while DeFi prices are under siege at the behest of a fun media story, this too shall pass, and DeFi will continue to grow stronger in the face of these constant stress tests.

What We’re Reading This Week