What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

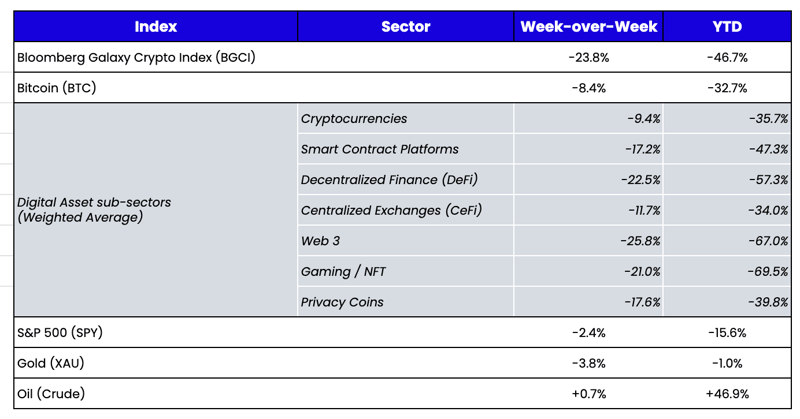

Week-over-Week Price Changes (as of Sunday, 5/15/22)

Source: TradingView, CNBC, Bloomberg, Messari

The Road to Redemption

Last week, the digital assets industry experienced the largest wealth destruction event in its young history. More eyeballs than ever were focused on and affected by the carnage. A single actor initiated a malicious attack during the normally vulnerable, illiquid weekend trading hours, which escalated into a full-blown crisis of confidence and caused an $18 billion “stable”coin, UST, to depeg from $1. Stablecoins have always been a bit of a misnomer, as all types are lumped into one category (debt-backed, asset-backed, algorithmic), but it's safe to say that market expectations were that an instrument marketed as a stablecoin would, in fact, hold its peg.

UST did not.

On Monday, UST gapped down to $0.70, ultimately triggering a death spiral as UST holders rushed to redeem UST for LUNA ($1 of UST can always be redeemed for $1 of LUNA), and then sold the converted LUNA on the open market. Others who could not execute the arb simply sold UST in the market at a discount. Naturally, these simultaneous actions caused both UST and LUNA to come under tremendous pressure and a “run on the bank” ensued. Think of LUNA as the “quasi equity” of the protocol, which backs the UST debt. As LUNA’s market cap fell below that of UST, the “debt-to-equity” ratio exploded higher and a complete loss of confidence followed.

Though investors and partners began earnest attempts at another “too big to fail” bailout, ultimately, no deal was reached. LUNA fell to effectively $0, while UST is now trading based on expected recovery value (currently around $0.15). Just over a month ago, LUNA traded at highs near $120 with a market cap of about $40B; UST had a market cap of close to $20B. Almost all of it was wiped out. For perspective:

Bear Stearns was $25B

Lehman Brothers was $60B

Enron was $65B

Luna / UST was $60B

These “too big to fail” type bailouts had an unintended consequence of creating a moral hazard that has persisted for decades and fueled excessive risk-taking. No one bailed out LUNA, UST, its investors, or the industry. Instead, the attack fueled more polarizing takes and jawboning with no action. Digital asset industry members will have to recover organically, and like many times before, the industry will look to be successful in this quest.

There is a real duality building here. While one market receives perpetual bailouts, another crashes, burns, rebuilds, crashes, burns, and rebuilds. Over time, we will learn which path ultimately leads to better long-term viability. Over the next few weeks, we will start to know the full extent of damage as reports of significant losses and collapses emerge. As our friends at QCP noted:

“In spite of the carnage, however, we are heartened by the resilience we've seen in particular segments of crypto. Firstly, crypto trading infrastructure has been smooth and seamless throughout the crisis. Compared to previous crashes, there were practically zero disruptions in major spot and derivatives exchanges. Secondly, despite the knee-jerk sell-off, BTC and ETH prices have held up surprisingly well. BTC dipped to a 25,340 low but has bounced back close to 30,000 level. ETH dipped to a 1,701 low but has come back above the 2,000 level. The vol markets have been a roller coaster ride as well. Naturally, vols rallied across the curve but the front-end has been particularly wild with BTC rallying from 50% to 186% and ETH from 60% to 195%! But given the resilience shown by the market, vols have now come down significantly with BTC front-end at 75% and ETH at 85%.”

In our opinion, here are some of the most important things to watch out for following last week’s fallout:

1) The probability of stablecoin regulation did not increase as a result of Terra Luna. It was already inevitable that stablecoins would be regulated. But the speed with which new laws and regulations will emerge has undoubtedly increased. This massive event will cause change to come sooner than later.

2. Terra Luna was NOT a Ponzi scheme. Affixing the Ponzi label to anything that doesn’t work in digital assets is incredibly tiresome. The LUNA/UST peg mechanism was experimental but very transparent. It had both strong supporters and harsh critics. Many consumers and investors avoided the risks; others knew the risks and decided the risk/reward was worth it.

The main issue is that many did NOT know the risks, especially retail investors. This is less a failure of Terra Luna than it is the supporting companies, exchanges, DeFi platforms, and backers that allowed unsuspecting consumers to trade these assets without adequate disclosures. For example, when another token, ICP, fell over 90% last year due to a lack of disclosures from exchanges, we wrote:

“Worse, the exchanges themselves did nothing to help new buyers of ICP understand these issues, and while they may claim that they simply provide a platform and not an underwritten investment banking service, it is pretty clear that most would have avoided this ICP token had any of this information been known.”

Every single place where LUNA and UST could be bought, sold, staked, or arbed knew the mechanism, but few, if any, disclosed it. There is no doubt that both the rapid rise and precipitous demise were exacerbated by the lack of a full understanding from unsuspecting participants.

|

|

The resilience of digital assets, standing on its own with no moral hazard or Fed put, will be on display once again. Many were hurt and wiped out. Others were badly wounded. Since the start of April, the total digital assets market cap has declined by nearly $1 trillion, or ~50%. But this is not the first, or likely the last time this will happen. There have been many episodes prior, from Mt Gox, to the ETH DAO hack, to the 2018 and 2020 crashes. Last week, a top 10 token by market cap blew up, and it will likely be yet another footnote in the history books of digital asset adoption. Many other tokens were collateral damage; some will never be heard from again, while others will rise from the ashes spectacularly.

INCEPTION

Written by Arca Venture Capital Principal David Nage

Over the last few years, and especially the last few weeks, I have been coming back to a question of what is real and what is not, and it made me think of the movie Inception. The film stars Leonardo DiCaprio as a professional thief who steals information by infiltrating the subconscious of his targets by using a machine that can stage dreams. These dreams are incredibly realistic so that the thieves and those around them believe it was their reality. The only way for DiCaprio and his crew to test that they aren’t still dreaming is to spin a top; if the top doesn’t eventually stop and fall to its side, they are still dreaming. A tweet from Bill Gurley, a prominent venture capitalist from Benchmark, has me wondering if, for the last twelve years, we were all stuck in one of those dream loops in the form of Quantitative Easing (QE):

DREAM MACHINE

QE is when a central bank buys bonds to drive down longer-term rates. As it creates money for those purchases, it increases the supply of bank reserves in the financial system, and the hope is that lenders go on to pass that liquidity along as credit to companies and households, spurring growth.

The Federal Reserve implemented the first QE measures on November 25th, 2008. At the time, the Fed announced “the purchase of the direct obligations of housing-related government-sponsored enterprises (GSEs)—Fannie Mae, Freddie Mac, and the Federal Home Loan Banks—and mortgage-backed securities (MBS) backed by Fannie Mae, Freddie Mac, and Ginnie Mae. Since 2008, major central banks have pumped over $25T into the economy through QE, with over $9T in response to COVID-19 alone.

'

As seen in the last ten years of the S&P 500, there has been a continuous debate that much of the performance, e.g., “bull market,” went hand-in-hand with QE:

Source: Fred Chart

A few years ago, Brian Barnier, a principal at ValueBridge Advisors and founder of FedDashBoard.com, analyzed the Fed’s activity with their several trillion-dollar programs to buy bonds. That quantitative easing policy, he said, meant the Fed was essentially responsible for more than 93% of the market’s movement.

“UNLEARNING”

Bill Gurley predicts a painful “unlearning” process for founders, and it stuck in my head for days after he wrote about it. For over a decade, a mighty machine (the Fed) has been keeping us in a state of euphoria, or a dream-like state, to the tune of $25T. This is important because equity markets and venture have connective tissue—specifically when it comes to the evaluation of potential future outcomes:

- Equity markets, specifically IPOs and M&A, have historically been viewed as the potential success (“exit”) of private companies

- In evaluating early-stage, private companies, comps are derived by reviewing relative equities (review of multiples, cash flow, revenue, and other metrics)

Quantitative tightening (QT) appears to be waking us up from this dream and speeding up this need to unlearn.

TOUGH PILL TO SWALLOW

If you ask any parent what it’s like to be woken from a deep sleep by a crying baby, it’s not pleasant. There’s a period—sleep inertia—during which the body and brain need to adjust and acclimate to the new issue at hand. For founders—both in traditional venture and digital assets—there’s a bifurcation in the data that could cause a delay in their “awakening.”

On the one hand, as discussed, we are seeing what could be a period of QT that could bring the equity markets to a new normal. On the other hand, founders in traditional and digital asset venture see data that points to a robust M&A and fundraising market in the last twelve months.

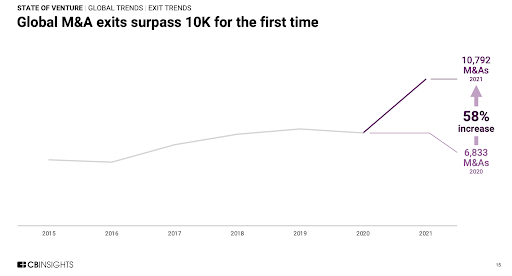

According to CB Insights, global mergers and acquisitions crossed the 10,000 mark for the first time in 2021, increasing 58% compared to 2020. M&A has gone up the last 6 straight quarters, leading to a record high of 2,938 in Q4’21.

Source: CB Insights

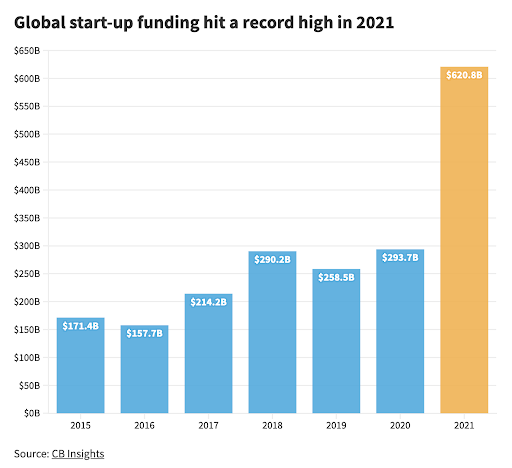

This, plus one of the biggest years on record for start-up funding in 2021 as seen below:

When Gurley speaks of an “unlearning,” he suggests that for the first time in over a decade, founders do not have the dream machine behind them this year. While the last year has been tremendous in terms of supportive activity for them, it was on the heels of a machine that is no longer operating under the same conditions as before. The game is changing—the top has stopped spinning and has fallen to its side.

EFFECTS ON DIGITAL ASSET VENTURE CAPITAL

By now, most people know that 2021 was a banner year for capital deployment in digital asset venture to the tune of approximately $30B-$33B. In Q1 of 2022, this trend continued, as highlighted by TheBlock, Crunchbase, Dove Metrics, and Pitchbook data:

It’s a rather important time for early-stage digital asset founders. There are more money chasing opportunities today than ever before and more billion dollar funds in digital assets than in its entire history. However, as we see from a macro perspective, tides are changing. If equity markets continue to feel the pain of a new era of tightening with an increased cost of capital for companies, inflationary pressures hitting housing markets and the consumer, there is a higher probability that it will trickle down to founders in this space sooner rather than later. So now is the time to not just “unlearn,” but learn practicality, manage monthly burn, and be mindful of excessive overhead. If you’re raising a Seed round, with a proof of concept and some early backend coding complete, it may be increasingly difficult to get a $100M pre-money valuation today.

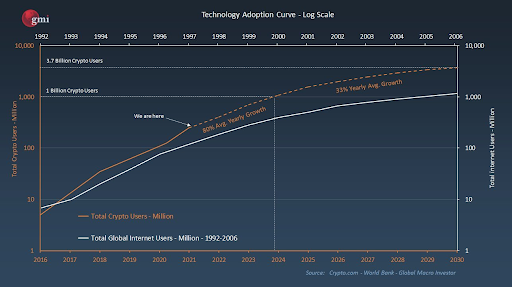

This chart from Garry Tan of Initialized Capital says it all as it relates to where we are in the cycle of growth and maturation in digital assets:

While the world is on fire with war, pandemic, and economic issues at home here in the states, seeing this chart so clearly represents that while things may get a bit tough here for the next few quarters or more, we are still early relative to the growth of internet users - VERY early. Founders will build and create amazing innovations, they just have to do it in a new paradigm where the dream machine is unplugged.

What We’re Reading This Week