What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

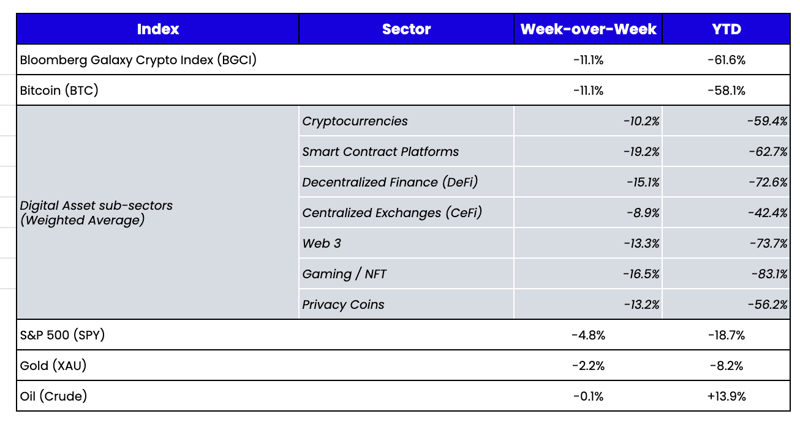

Week-over-Week Price Changes (as of Sunday, 09/18/22)

Source: TradingView, CNBC, Bloomberg, Messari

The ETH Merge Was a Smashing Success

By now, most of you have read about the success of the Ethereum Merge from proof-of-work (PoW) to proof-of-stake (PoS). It is an outcome we had nearly 100% confidence would happen without a hiccup, but admittedly had little idea how ETH would trade in the immediate aftermath. Even though we and others trusted the Merge would complete seamlessly, getting to a point of certainty was no small feat. Let’s take a minute to reflect on just how significant this technological achievement was. As Galaxy Digital explained:

“Never before has a public blockchain of Ethereum’s size radically upgraded its consensus mechanism to a new model and done so without sacrificing network liveness. At no point were Ethereum decentralized applications (dApps) and user transactions halted on-chain to allow time for this upgrade to occur. While there were off-chain service providers such as exchanges that preemptively did not offer trading services during the Merge, the upgrade itself did not trigger an extended period of network downtime. Switching from a PoW to a PoS consensus protocol was by far the riskiest code change to date on Ethereum. It required the longest period of research and testing relative to other code changes on the network. In many ways, the completion of the Merge affirms the powerful potential of open-source software development and the abilities of Ethereum core developers to coordinate complex upgrades even with billions of dollars at stake and an exponentially growing ecosystem of stakeholders operating on the network.”

Well said. This historic achievement became a foregone conclusion because of how much work developers dedicated to ensuring a successful outcome over the past several years. In terms of price action, ETH fell roughly -25% week-over-week. This outcome was much more surprising, but not entirely unexpected. We always believed the ETH Merge was a 3-step investment.

Step 1 (Completed): Long ETH once an official Merge timeline was announced. This part of the trade largely ended two weeks ago.

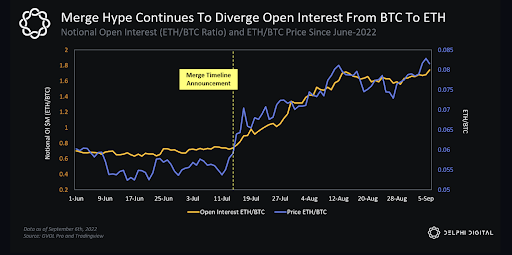

Source: Delphi Digital

Step 2 (Active): Price action in and around the Merge, which includes a lot of arbitrage unwinds from those that purchased (or borrowed) ETH to receive an airdrop of the forked PoW chain (ETHW). This outcome had the most uncertainty, as there were various factors influencing direction (arb unwinds, “sell the news” event price action, macro hiccups). Ultimately, it appears the Merge itself did not immediately attract new buy interest, or new buyers are about to get a nice discount courtesy of momentum traders with itchy trigger fingers.

Before the Merge, newly minted ETH (e.g., inflation rewards) were split between miners and stakers. Daily, about 13,000 ETH (~$20M) were distributed to miners, and only 1,600 ETH (~$2.5M) were distributed to stakers on the consensus layer (Beacon chain). After the Merge, ETH issuance falls 88% as PoW mining goes away, but staking will remain unchanged at 1,600 per day. On top of this, via the EIP-1559 proposal implemented earlier this year, a portion of ETH transaction fees—which dwarf any other blockchain or application—are burned, creating the equivalent of a continuous buyback program. As a result, the daily ETH burn may sometimes exceed the net daily emissions, potentially placing ETH in a very small category of tokens that both produce revenue and have amortizing supply schedules rather than inflationary supply. It’s worth noting that the other amortizers (CHZ, BNB, LEO, and FTT, for example) consistently outperform both bull and bear markets.

Amortizers Outperform in Good Markets

(Apr 2020-Nov 2021) |

Amortizers Outperform in Bad Markets

(Dec 2021-Present) |

|

|

Source: TradingView

And finally, after years of punishing the digital assets industry over high energy usage, the anti-ESG campaigns that have plagued Bitcoin have now declared ETH as the victor in this category.

As we await to see how the next few years play out, one thing is (somewhat) certain. While Bitcoin may be the face of digital assets, Ethereum is now the backbone of DeFi, NFTs, DAOs, Layer 2s, and so on, with 3,500 active dApps. This is a big deal and won’t show up in a week’s worth of price action.

Let’s Get the Crypto Analogies Right, People

For years, we’ve been fighting a losing battle as we continuously paint a picture that digital assets are unique and complex. In contrast, the media generally paints all of “crypto” with one broad brush stroke. Whenever a reporter asks me “how crypto is trading,” I immediately respond, “How are ETFs trading? Are ETFs up or down today?” Of course, that’s an unanswerable question. ETFs are simply a wrapper that house many types of assets, often completely unrelated other than the package in which they are offered—the ETF. Similarly, blockchain-based digital assets are simply a wrapper in which a variety of assets now reside.

Fortunately, the ETH Merge has further separated Ethereum from Bitcoin. So perhaps now we can finally get the message across that most other digital assets are also very different from each other. To do this, let’s use some analogies:

- Bitcoin is gold. Like gold, Bitcoin has a fixed supply in the world but an inflating schedule of circulating supply as it is mined from the earth. It has no intrinsic value, but it has hard properties, thus making it a store of value. You can spend it if someone is willing to take it, but mostly, it is just there to exist with a conversion ratio back into other currencies that are more spendable. While there are some Bitcoin copycat tokens, for the most part, Bitcoin stands alone.

- Ethereum is the Apple app store. The app store opened in July 2008 with 552 apps. Before its launch, Apple laid out the roadmap for iOS development. It included a software development kit (SDK) for programmers to write apps, and Apple announced it would provide a storefront through which developers could sell their software. As a result, the App Store has made some developers fabulously wealthy, given many a new and stable career, and seen others fade away with broken dreams and disappointments. Today, the app store has well over 2 million apps.

Similarly, before the Ethereum smart contract protocol launched in July 2015, the whitepaper was released (November 2013) and the ETH token was sold (summer 2014). Like the Apple app store, blockchain developers were given a roadmap to build dApps, and many developers made fortunes while others crashed and burned. Some apps were ready to go upon launch (MakerDao was one of the first Ethereum dApps), while most others were built years later. Today, there are over 4,000 dApps built on Ethereum.

Both iOS and Ethereum started as blank canvases reliant on the creativity of outside developers to find success. At the same time, both Apple stock and the ETH token had speculative value in anticipation of future success. Today, both are thriving ecosystems where the growth of apps, users, downloads, and transactions create revenue (Apple) and fees (Ethereum) that accrue to AAPL shareholders and ETH tokenholders, respectively.

- Layer 1 Blockchains (Solana, Fantom, Avalanche) Are Android, Microsoft, Ubuntu, etc. Of course, the success of Ethereum spawned competitors, much like the success of the Apple iOS brought out competitors (you can argue that Android was built before iOS, but iOS seemed to hit mass adoption faster). Some of iOS’ competitors started to scale aggressively, others have cult audiences, and some have crashed and burned. Similarly, some of ETH’s competitors are finding real product-market fit (like Solana with NFTs). Those blockchains that are starting to see real success are attracting developers who are building dApps, and some dApps are now offered across multiple blockchains, just like most apps are offered on both iOS and Android. The iOS and Android app stores contain gaming, healthcare, banking, media, and e-commerce apps. The Ethereum and Solana protocols offer gaming (NFTs) , healthcare, banking (DeFi/stablecoins), and e-commerce (Web3) dApps.

- Binance is JP Morgan Chase. Binance Coin (BNB) is the 5th largest token by market cap behind Ethereum and Bitcoin. Binance is a one-stop shop for digital asset trading, lending, borrowing, and asset management. The exchange produces an estimated $20-30B in revenue each year (JPM produced $128B in revenue last year). The BNB token is a pass-thru token; it provides utility in the form of member benefits/rewards (e.g., reduced fees if you own BNB and trade on the Binance platform) and financial benefit in the form of profit-sharing (Binance burns BNB tokens, akin to a stock buyback, using profits generated by Binance). JPM has a $343B market cap; Binance has an estimated enterprise value of $250B, which includes the equity of Binance (estimated at ~$200B) and the BNB token ($43B). In essence, the BNB token acts as a form of quasi-equity and a member reward card, like a Chase credit card holder or preferred banking partner. Binance looks nothing like Bitcoin or Ethereum, just like JP Morgan looks nothing like Gold or Apple. Note that this analogy would make FTX similar to Goldman Sachs.

- Stablecoins are currencies. Tether (USDT) and USDC are the #3 and #4 largest tokens by market cap ($67B and $50B, respectively). Both are proxies for cash and credit in the banking system, with USDC seen as the more regulated banking cash (like the Fedwire Funds Service), whereas USDT is used in the same way but is seen as a more global yet less regulated version (like eurodollars). Both are used exclusively as a medium of exchange and are owned for price stability rather than price growth.

We could keep going: Helium (HNT) is a telco infrastructure play like American Tower or SBA Communications. Chainlink (LINK) is computing infrastructure like Intel or Advanced Micro Devices. Chiliz (CHZ) is a sports and entertainment company like DraftKings. The Sandbox (SAND) is a gaming platform like Take Two or Activision Blizzard.

The point is that for the first time, the Ethereum Merge is forcing the regular digital asset talking head to think and speak about the uniqueness of these assets. And once you start, you realize just how much depth this market offers.

You wouldn’t ask a long/short equity fund manager to comment on gold, so let’s stop asking every digital asset participant to comment on Bitcoin.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.