What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

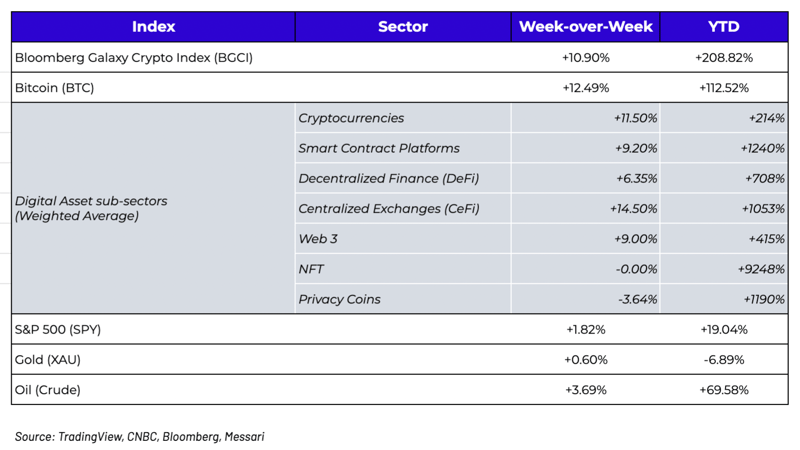

Week-over-Week Price Changes (as of Sunday, 10/17/21)

The Bitcoin ETF is Coming With All Sorts of Pros and Cons

As our friends at Cliffwater pointed out, the logos of the remaining four teams in the MLB playoffs spell “BLAAH”. This seems appropriate, since not a whole lot happened last week other than continued upward price action driven by further speculation about the seemingly inevitable approval of Bitcoin Futures ETFs. Last week, we wrote about the market effects of a Bitcoin ETF, an increase in centralized failures, and Tether, but with all three coming to a head, we’ll spend one more week diving deeper into the bigger picture at hand.

After a decade of Bitcoin ETF efforts, the market is now pricing in near 100% certainty that a select few of the dozen Bitcoin ETF applications will get approved by the SEC, potentially as early as this week. This is bittersweet. On the positive side, this was a long, arduous road for many, and becomes yet another indication that digital assets are crossing into mainstream. Perhaps the silos between traditional finance and digital assets are slowly starting to merge. But on the other hand, this is yet another terrible version of a good underlying product, where somehow along the way, we severely lost the plot. Bitcoin’s 40% MTD rise on the heels of an “exchange listing”, despite a lot of Bitcoin transaction and usage metrics heading south, just turned Bitcoin into the equivalent of a 2017 ICO reacting to a telegraphed Coinbase listing. While having the ETF based on futures gives the SEC comfort from a regulatory standpoint, the product itself has material negative costs for investors. Coinbase wrote, “After the initial euphoria wears off, will the premium for investors be worth it?”

Arca CEO Rayne Steinberg summed up the mixed feelings, taking both a pro regulatory stance and an anti-terrible product stance:

We are pleased when more products addressing our space receive regulatory approval. But we do not think a futures ETF is a good way to get Bitcoin exposure. Futures based ETFs work for short term trading, but have massive tracking error issues over long periods, which is what most investors are looking for when it comes to Bitcoin exposure. Is it that hard to put out products that give investors a good experience?”

Unfortunately, it appears it is that hard. We’ve been writing about this for years. From poorly constructed index products, to “hotel california” trusts where you can check in but can’t check out, to Wall Street land grab ETFs with the word “blockchain” in them that don’t provide investors with any real exposure to digital assets… we seem to be stuck in the unenviable position of “great recipe, terrible cook”. Even “crypto stocks” soared last week despite none of them directly benefiting from a Bitcoin ETF, showing that the majority of the world continues to use inefficient vehicles to gain exposure. If for whatever reason you still don’t have access to the actual digital assets themselves, the substitutes available are simply sub-par.

Matt Levine of Bloomberg wrote what is perhaps the most succinct two paragraphs to date (buried in a non-succinct article) discussing this unfortunate siloed dynamic.

... my basic thinking on crypto is often that there is a crypto financial system and a traditional financial system, and they run on different rails, and there are costs and frictions in switching between them. If you are a crypto trader, it is irritating enough to transact in U.S. dollars that you’ll go use a weird stablecoin in order to send dollars using crypto rails. If you are a traditional-finance hedge fund, it might be irritating enough to transact in Bitcoins that you’ll go use a weird ETF in order to buy Bitcoins using traditional rails. Someone (the ETF provider, the futures arbitrageur, the stablecoin entrepreneur) is making money from those products; you are paying them that money for the service of doing the rail-switching so you don’t have to. I suppose that could last forever.

But doesn’t that seem unlikely? Certainly crypto enthusiasts have grand plans for taking over the traditional financial system, for making stocks and bonds and interest-rate derivatives and mortgages trade on the blockchain. For that matter, the traditional financial system also tends to express a lot of enthusiasm for blockchains. It just seems implausible to me that in 10 years crypto will still be big and we’ll still be talking about how hard it is to switch between your brokerage account and the blockchain, or that there will be big lucrative businesses of “putting dollars on the blockchain” (stablecoins) or “putting Bitcoins into your brokerage account” (Bitcoin futures ETFs). Eventually crypto will take over traditional finance or traditional finance will take over crypto or everyone will just be comfortable transacting in both, and an ETF of synthetic Bitcoins will look sort of quaint.”

He’s right. This cannot last forever. One of the two silos has to ultimately win out, or a third option must be created where the two are separate but the ability to move freely between worlds is easy and painless because they function cohesively. Though I can’t help but notice the irony when Bitcoin marches back to all-time highs on an ETF listing during the same week that the ETF of bank stocks hit new all-time highs following record bank earnings, despite being disrupted left and right by FinTech and digital assets. The CME stock hit all-time-highs as well, which is not surprising since they are being hand-picked by regulators. Perhaps the market is giving us a clue as to who the ultimate beneficiaries of regulation really are... as long as you are an investor in bank and brokerage stocks, you are very well protected.

The Tether Saga is Finally Over

Of course, it will never actually be over until every last macro hedge fund bleeds to death on negative carry trying to short USDT. But for all intents and purposes, last week’s $41 million settlement between the CFTC and Tether is about as clear as it can get. While the press releases and articles were littered with bias, the actual CFTC settlement itself and Tether’s own statement should put an end to an annoyingly persistent and factless story about Tether that has been ongoing for years. There is no question that Tether made questionable decisions earlier in the lifecycle of the company, some of which may have been due more to a lack of choice than intentional sleight of hand, but those mistakes were uncovered and disclosed years ago. The 2021 version of Tether is far superior from a transparency and business standpoint than 2017-2018 Tether. While that doesn't excuse or forgive past wrongdoings, as it stands today, Tether is transparent, highly utilized, works well, and is an important part of the digital assets ecosystem. More importantly, any go-forward issues related to stablecoins are industry-wide, and not Tether specifically. We, as an industry, should be holding ALL stablecoins to the highest level of scrutiny about their underlying holdings, rather than give one company a free pass while vilifying another despite nearly identical products and disclosures. Stablecoins are under the microscope in Washington, and for good reason, but not because of uneducated fear about a single bad actor that fessed up years ago.

Time is Money -- the Parallel Universe

Despite all of the issues related to HOW this industry is currently being regulated (or not), at the end of the day, there are trillions of dollars on the edge of the pool waiting to jump in if we can get this right. In addition to Arca’s efforts, there are numerous well-resourced companies heading to Washington with ideas of their own. As Messari pointed out, a16z dropped its full lineup of policy proposals as well as a phenomenal deck they are using to educate policymakers and regulators. Coinbase and FTX also dropped thoughts of their own regarding how centralized digital asset services might be effectively brought into a smart and cohesive policy framework, improving upon an outdated 90-year old framework.

At Arca, we strongly believe in the need to bridge the gap between the two systems. Currently, the digital assets ecosystem is set up in such a way that institutional and professional investors have a hard time putting money into the space due to the lack of safeguards and systems. It is incredibly important for institutional money to enter the space. As Luis A. Aguilar, Commissioner, U.S. Securities and Exchange Commission wrote in 2013:

“It is clear, however, that professionally-managed institutions can help ensure that our capital markets function as engines for economic growth. Institutional investors are known to improve price discovery, increase allocative efficiency, and promote management accountability. They aggregate the capital that businesses need to grow, and provide trading markets with liquidity – the lifeblood of our capital markets.

In doing all this, institutional investors – like all investors – depend on the assurance of a level playing field, access to complete and reliable information, and the ability to exercise their rights as shareowners. That is why fair and intelligent regulation is necessary for the proper functioning of our capital markets.”

While one can argue that there is a free flow of information in the digital assets market, it’s difficult to decipher what information is real and what is misleading. Like the SEC suggests above, we need access to unbiased education, knowledge, and resources to make informed decisions-- and very few companies in the space are offering these resources.

All that said, it is an interesting thought experiment to think about the alternative. What would it be like if we were able to keep these two silos completely separate, and operate two parallel and competing financial systems, one with regulation, and the other without? Could digital assets successfully grow and operate in a world with no rules, where the industry and its participants self-regulate, and customers opt-in while acknowledging and knowingly accepting the risks? Rarely do we get these real-life experiments… a choose your own adventure story where we get to see how both stories end. When we choose a specific route in life or while driving, we always wonder “what would have happened if we had taken the other path?” Like the movie Sliding Doors, there are two versions of a story depending on minor nuances in path function.

This world is littered with centralized failures and wrong versions. Just last month, the

entire NYC subway shut down, costing New Yorkers 5 hours of their lives due to a single human error. If time is money, how much collective production and output were lost during these 5 hours, and are the cost savings of regulating digital assets higher than the losses caused by this highly unregulated outcome? When Facebook and WhatsApp went down, how many billions of dollars of economic throughput were lost for good, where no amount of regulation was going to prevent this?

It seems like we have a rare opportunity to build from scratch and avoid some of these same mistakes, and let individuals opt into the system they prefer best. There’s a great book by Daniel Pink called “To Sell is Human”, which makes the argument that “caveat emptor” (buyer beware) no longer exists in the internet age because the buyer now has more information than the seller. As a result, salespeople no longer sell, they simply build trust. In the same vein, if all investors have access to ubiquitous and free information, and all they are looking for is trust, isn't it plausible that they will trust computer code more than governments and banks? Perhaps a truly trustless system, with perfect customer information but potential fraud and hacks is a better answer in today’s modern world.

What’s Driving Token Prices?

- BTC (+12%) The SEC seems poised to approve a Bitcoin ETF, with the formal announcement due on October 18th. Since July 19th, CME Bitcoin futures open interest is +125% from $1.6B to $3.6B, much of which was due to expectations of the ETF approval.

- PERP (+15%) A new Perpetual Protocol dashboard was released, which offers investors metrics on trading volumes, fees and numbers of daily and weekly trades. Weekly unique users went from 690 to 935.

- HNT (+13%) Helium announced a new roaming partner, Actility. This partnership will add mass enterprise adoption and usage to the network, immediately unlocking ubiquitous coverage for millions of IoT devices. Like Helium, Actility is recognized as the leader in IoT connectivity solutions and LPWA technology.

What We’re Reading This Week