What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 3/14/21)

Rotation, Rotation, Rotation -- and More Terrible “Crypto” products

The S&P 500, Russell 2000, and Dow all hit record highs last week, the VIX fell 16%, and Treasury yields extended their rise amidst reopening optimism, increased inflation expectations, and a $1.9 trillion COVID-19 relief bill. While all risk assets are doing well at the expense of fixed income, cash and gold, there is a clear rotation happening within these broad-based gains. As Deutsche Bank recently pointed out, since the November vaccine news, anything related to banks and energy has done extremely well, while anything that went up post-Covid but pre-Vaccine has begun to struggle (Tech stocks / FANGs).

And then there’s Bitcoin, which has outperformed everything in both market environments.

Returns from March 2020 to Nov 2020 vs Returns from Nov 2020 to Present.png?width=727&name=unnamed%20(78).png)

Source: Deutsche Bank

Bitcoin doesn’t seem to be slowing down either. Five out of the last six weeks have produced double-digit returns (week ending):

- 2/7/21 +16%

- 2/14/21 +25%

- 2/21/21 +18%

- 2/28/21 -20%

- 3/7/21 +13%

- 3/14/21 +17%

Given this backdrop, it’s hard not to focus on Bitcoin. Yet rotation is happening within digital assets as well, as every single unique sector of digital assets has vastly outperformed Bitcoin and cryptocurrencies YTD. These other sectors have nothing to do with “purchasing power” or “inflation protection” or “digital money”, and instead are equity-like investments in companies and projects that are utilizing blockchain technology in completely different forms. This rotation makes sense, yet the majority of investors don’t even know these other areas of digital assets even exist, nor understand how different they are from each other. While there are plenty of advisors, brokers and asset managers in the traditional financial world that will happily help their clients make changes regarding their equity exposures as investment theses and outlooks change, in the digital assets world, gaining exposure to NFTs, smart contracts, DeFi, CeFi, Web 3.0, and other types of digital assets still remains challenging for anyone who isn’t invested in an actively managed hedge fund.

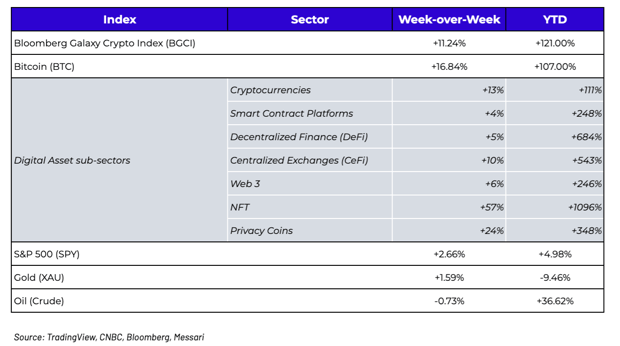

Returns by Sector in Digital Assets -- Bitcoin is lagging YTD

Source: Messari

Worse yet, even if you were purposefully and happily trying to own just Bitcoin, as NYDIG highlighted, most of the products dedicated to Bitcoin aren’t even coming close to accurately tracking the underlying asset. One of the worst offenders this year has been Grayscale’s $35 billion GBTC trust, which is trailing Bitcoin’s return by over 3000 bps YTD as the trust now trades at a significant discount to net asset value. This collapse in the premium has prompted Grayscale’s parent company, DCG, to announce a buyback of $250 million of GBTC in the open market in an effort to push the premium back into positive territory, else Grayscale will have difficulty raising new money at NAV (and has already halted new subscriptions). The Grayscale arb trade isn’t even a secret -- Grayscale’s own sales people used to pitch the arb to prospective clients openly at conferences, and with this free money now gone (and several arb investors underwater), Grayscale needs to make changes. There’s nothing wrong with this -- Grayscale is a very good business, and DCG has the balance sheet and the wherewithal to do whatever is necessary to stave off competition and to entice new buyers. The problem, however, is deeper than simply a lack of demand. The problem is almost every business in this industry has too much leverage and exposure to Bitcoin, and almost none to the other areas of digital assets that are actually growing.

.png?width=1262&name=pasted%20image%200%20(17).png)

Source: NYDIG

Fortunately, JP Morgan is here to rescue investors with an even worse product. JPM isn’t going to sit back and do nothing while trading fees and assets are exploding around them, so they introduced a “cryptocurrency exposure basket” filled with stocks of companies that have almost nothing to do with digital assets (Hint: JPM can bank all of these firms, and trade all of these stocks). At best, these companies are VERY loosely tied to Bitcoin’s fate, and this product will siphon even more money away from other Bitcoin products, but will likely do nothing to capture the real growth of this industry.

What we’re seeing here is an old-fashioned Wall Street land grab, resulting in an incredibly oversaturated and overly competitive market for Bitcoin-related growth. And unfortunately, that leads to excessive risk-taking in order to stay competitive.

Excessive Risk Taking → Shadow Banking in Bitcoin

First, congratulations to our friends at BlockFi for completing a $350 million Series D equity raise at a whopping $3 billion valuation. This is a very good company, with a strong management team, and a lot of growth potential. However, big headlines also result in increased scrutiny.

You can sign up for a BlockFi account in seconds to earn interest on your Bitcoin with “no hidden fees”, and they now have 225,000 clients who have deposited over $10 billion in assets on their platform. Presumably, that means you deposit Bitcoin, BlockFi pays you a yield, and they must be lending that Bitcoin out 1-for-1 to others who want to borrow Bitcoin at a higher rate --- a simple Net Interest Margin (NIM) business right? There’s certainly nothing on the website that indicates anything differently, or anything that suggests there may be hidden risks involved in this process. Then again, you may wonder why a company in such a simple business line that should be immediately profitable has needed to raise over $500 million since inception from investors, and is, according to a Coindesk interview, just now “operating profitably for several months.”

Here’s a riddle: What’s a bank called that isn’t actually a bank and doesn’t offer FDIC protection?

Answer: A secretive hedge fund

And BlockFi to date has been a very good, successful hedge fund. Whatever their secretive risk management process is, it seems to be working very well - there have been no defaults and customers are happily being paid. But recently some of their practices have come under the microscope. The dirty secret is that there really isn’t that much demand to borrow Bitcoin. Plenty of customers want to earn a yield by lending their Bitcoin -- but very few need or want to pay money to borrow Bitcoin. What happens if, for example, you have depositors giving you 50 BTC and you pay them 5% per year, but you can only lend out 10 BTC for 8% per year? You make a fat 3% on 10 BTC, but have 40 BTC leftover that creates a revenue shortfall, and you now have to put that BTC to work to earn a return large enough to pay your excess depositors. Worse, most of the interest to borrow digital assets comes in the form of US-dollar stablecoins and ETH. As a result, you now have a very lopsided asset / liability mismatch (people lend BTC, but borrow USDT, USDC and ETH), and this mismatch needs to be managed very carefully to ensure that all interest can be paid and all principal can be repaid. Anyone who has seen BlockFi’s external capital raising deck has known for a long time that some of that yield shortfall has been filled using risky practices, including the very same Grayscale (GBTC) arb trade mentioned above that used to be a cash cow (when GBTC was trading at a large premium), but just recently started to become a loss leader (with GBTC at a steep discount to NAV). This didn’t become broad public knowledge though until BlockFi’s Form 13G was filed at the end of last year, showcasing that of BlockFi’s $10 billion in customer deposits, over $1 billion of this was invested into GBTC (BlockFi is the 2nd largest holder of GBTC).

.png?width=699&name=unnamed%20(79).png)

Naturally, some competitors are now trying to knock BlockFi down with smear campaigns, and BlockFi itself had to go on the PR offensive by speaking on a variety of podcasts (often hosted by their own investors) to defend their practices. In fact, in a recent episode, CEO Zac Prince even said “I don’t want to reveal all of our risk management secrets because this is a competitive industry”. He also said they don’t put any of these risks on the website itself because no one wants to read that, and instead offer transparency through podcasts and other mediums. That would be the equivalent of a food company not putting FDA-enforced sugar, fat and sodium details on the actual package (where people make buying decisions), and instead talk about their ingredients three months later at a tupperware party. Sounds a lot more like a private hedge fund than a bank paying safe, stable interest to depositors.

Now, here’s my actual take. I think BlockFi is a very good business, and I wouldn’t be scared at all to deposit assets with them. In fact, Arca is a client. BlockFi simply used external funding via large equity capital raises to subsidize losses in the early days (like just about every early stage business), then prioritized growth over profits to crush their competition (successfully), and is now in the enviable position of being able to offer other lines of business (credit cards, trading) using their strong brand and balance sheet to generate real revenues that can easily offset any losses coming from risky investments in their core business. Very smart, very savvy, and likely a great long-term equity investment.

However, there are risks when you invest (or lend) assets, and it probably takes longer than a 30 second sign up form to understand what these risks are. Not a single investor on the planet would invest in a hedge fund without speaking to the CIO or the risk management team, yet how many of BlockFi’s 225,000 customers have had a conversation with BlockFi’s risk team? There seems to be a disconnect in the way a borrow/lend FinTech firm can operate versus the way traditional asset management firms operate, even though they end up making a lot of identical investments on behalf of their clients in the quest for returns. Asset managers have to be very careful with how they invest client money - we have a fiduciary duty to our investors. But borrow / lend desks get to take deposits in seconds and market to whomever they want, however they want, and are under no obligation to disclose the risks they are taking.

It’s very hypocritical for certain people to voice opinions on one issue, but to then pretend that BlockFi is doing something totally different. We understand the motivation to protect and grow their equity investments, but that’s one of the problems. We’re looking to champion transparency with participants using digital assets platforms, and yet some are fighting against that transparency when it’s convenient and self-motivating.

At the end of the day, all borrow/lend businesses have more people who want to lend (earn a yield) than they do who borrow (pay a rate), therefore, they have to make up that yield shortfall somehow. In order to earn additional yield, they have to make risky bets using practices that are no different than what highly scrutinized hedge funds do for their private investors. That’s perfectly acceptable… it should just be disclosed. The difference is these private investors who invest in hedge funds spend 18-24 months doing due diligence, and get frequent investor letters and LP calls explaining their practices, which is a tad bit more information than what the average depositor gets signing up for BlockFi, Celsius or others before depositing assets.

Is DeFi really more risky than a centralized borrow/lend desk? The reason people hate Wall Street is because it’s non-transparent, they lie to us constantly, and when things go bad, they cover it up until it’s too late, and then you get a crisis of confidence that results in defaults or a recession. The digital assets revolution was supposed to change the way the system works, not recreate it with the same hidden risks and shadow banking systems. If we want to change the system — then let’s actually change the system.

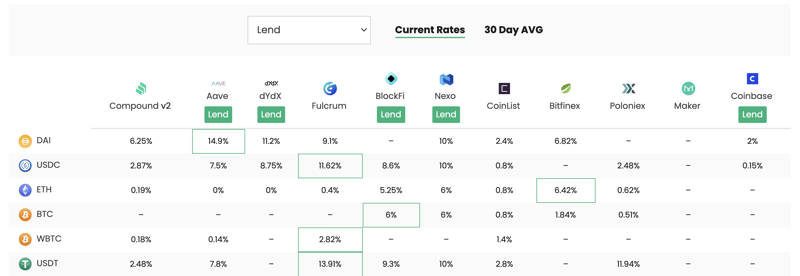

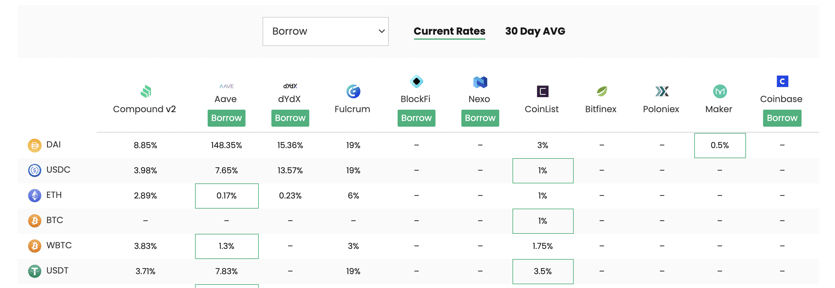

One of BlockFi’s competitors in the DeFi space is Aave.

Aave offers similar services to Celsius and BlockFi, only it’s 100% on-chain, and you can see exactly what is happening in real-time, including weekly transparency reports. Here’s what we learned from this past week’s report:

- Total Deposits = $5.3 billion

- Total Borrows = $1.3B (over 50% of this was stablecoins)

- Utilization = 24% ($1.3 bn borrowed for every $5.3 billion deposited)

- Interest Income -- Because stablecoins (USDC / USDT / DAI / BUSD) were over 50% of the total borrows, depositors of stablecoins earned ~75% of the weekly revenue

- Wrapped Bitcoin (wBTC) is 10% of the total liquidity but accounted for just 1% of the income, which tends to show exactly what we said above -- that everyone wants to deposit BTC for yield, but no one wants to actually borrow BTC.

That’s a lot of transparency, and also sheds light on what the true demand is for borrowing. We won’t need a form 13G to figure out what is happening on this platform -- Aave adjusts rates in real-time to balance the amount being lent versus the amount being borrowed. And you can look at the rates published across all lenders and borrowers (both DeFi and CeFi) to see how vastly different these rates are --those that look out of whack versus competitors are not tapping into some mysterious new demand that others don’t have, but rather, are subsidizing those yields in another way.

Do hacks happen in DeFi? Sure, sometimes (though Aave itself has not been hacked). But when they do happen, you know immediately. There are no cover-ups, and there is no additional risk taking to try to dig themselves out of a whole. Generally, a plan is developed quickly by tokenholders / governance members and the capital shortfall is filled, and many depositors are insured against hacks via Nexus Mutual anyway.

Meanwhile, most people in digital assets have probably never heard of Cred Capital. Cred Capital was a centralized competitor to Celsius and BlockFi, until they abruptly filed for bankruptcy late last year. For those distressed nerds like ourselves who actually read the entire bankruptcy Docket, you’ll know that Cred Capital looked like they had a pretty simple business model once too -- borrow Bitcoin for X, lend it for X plus a spread, print money. Only Cred Capital also had an asset / liability mismatch, and invested the excess Bitcoin horrifically, got in trouble, doubled down, got in more trouble, and eventually every depositor got completely wiped out (current claims are trading for under 5 cents on the dollar). In DeFi, this mistake would have been caught and rectified in days if not hours. With centralized lenders like Cred Capital, this cover up went on for months while new depositors had no idea that they were lending their money into a black hole. Now, to be perfectly clear, I don’t think BlockFi’s $350 million equity round was a cover up or a bailout, nor do I think BlockFi or Celsius or any other lender is in any financial trouble whatsoever. I am also not comparing the fraudulent business practices at Cred Capital to the seemingly strong business models at their centralized competitors. However, I also can’t with 100% confidence assume that their risk management practices will definitely work. And that’s the problem. Why do the equity investors who gave BlockFi $350 million know way more than the $10 billion worth of depositors who are taking substantially more risk relative to the expected return? Investors and depositors should know what they are getting into, and be willing and able to assess those risks - in real-time, not on a podcast. All companies (including but not limited to BlockFi) should be more transparent. We even publicly called out a company (Gnosis) last year for inappropriately and non-transparently investing investor capital -- they were actually quite good at investing, but no one knew they were doing it. That’s a problem.

This industry already has enough issues gaining trust and building solid reputations… it is incumbent upon all of us who are trying to build a better system to demand that the companies in this space be more transparent. The whole point of using blockchain technology is to create a public, immutable and transparent ledger to avoid the problems that caused the 2008 great financial crisis. Let’s follow this lead and demand the same transparency from the best centralized companies that are building great products in this space.

What’s Driving Token Prices?

With the whole market trading up (BTC +17%, ETH +7%) market movements tend to get lost in the shuffle. Bitcoin is pushing new all time highs, Ethereum is dominating conversations with EIP-1559, and Beeple’s auction with Christie’s created quite the buzz. However, this week the biggest moves came from isolated projects with strong performance indicators:

- Chiliz (CHZ) has exploded on the scene this month, posting extreme month to date gains (+1120%, +1850% peak) while their fan tokens have exploded in market cap (+128%, $395M). In a blog post from the team on Thursday, they attributed the frenzy to PSG advancing to the Champions League quarter finals, with the $PSG token reflecting that sentiment (+130% MTD, +230% peak). The CHZ token benefits from the increased uptick in trading volume in the fan tokens, as it operates as the sole trading pair and CHZ token burns are tied to the trading fees (20%), Fan Token Offerings (FTO, 10%), and net proceeds of NFTs and collectibles (20%). CHZ finished the week up 406%.

- Axie Infinity (AXS) has been the largest benefactor from the rising interest in the NFT sector - their marketplace has done 2635.54 ETH (~$4.65M) in volumes MTD, generating 139.94 ETH (~$245k) in revenue. Revenues from the platform will be sent to a community treasury which is governed by the DAO (voted on by AXS holders). This, in combination with the generic interest in NFT exposure, proved beneficial for the token, which finished the week up 116%.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.png?width=632&name=unnamed%20(75).png)

.png?width=1600&name=pasted%20image%200%20(18).png)