Source: TradingView, CNBC, Bloomberg, Messari

No One Knows What It Means, But It's Provocative

Financial: Free cash flow, dividends, buybacks

Utility: Usage, gas fees, collateral, rewards/points

Social: Brand, or a "cool factor"

Assets that possess all three qualities tend to outperform. Those that have only social value tend to die eventually (with a few exceptions). Many tokens start with 1 and then add the other 2 later. During strong market conditions, no one really focuses on these attributes too much. But during bouts of market weakness, such as today, valuation debates intensify.

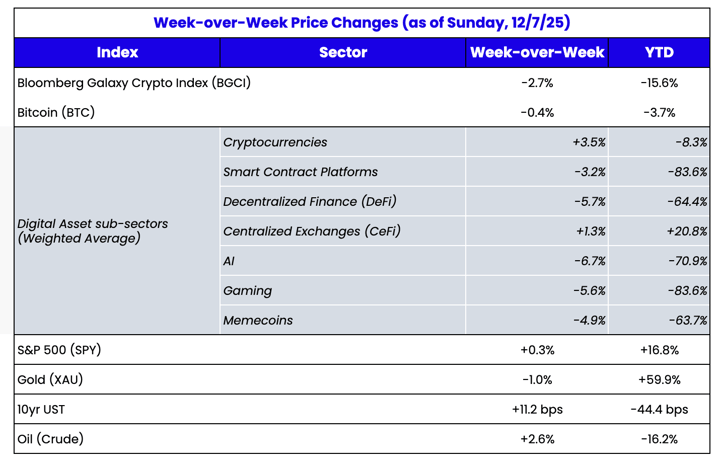

For today’s discussion, we’ll focus on the tokens of Layer-1 smart contract protocols, since they somehow still represent over 90% of the overall market cap of tokens despite most not having any traction,

and on the fact that the majority of all blockchain revenue comes from DeFi applications. ETH and SOL are now down -33% and -44% from the mid-September highs, and numerous other recent L1 token launches like Berachain (BERA), Plasma (XPL), Monad (MON) and Canton Coin (CC) are basically down only since launch. So it’s a good time to review valuations once again.

|

Price of CC

|

Price of MON

|

|

Price of BERA

|

Price of XPL

|

Source: Coingecko

We have been no strangers to these debates. We’ve argued for years that the

“Fat Protocol Thesis” is nonsense, and more recently, we have argued that a

sum-of-the-parts (SOTP) analysis of Layer-1 protocol tokens shows that most are either extremely overvalued or, at best, they derive most of their value from social factors. But we’ve also acknowledged that collectively the value of all L1 tokens is probably undervalued, even if each individual token is overvalued today. This stems from the belief that every asset eventually moves on-chain, which is becoming more and more likely as SEC Chair Paul Atkins and Larry Fink at BlackRock continue to convince the world that

all stocks, bonds, and real estate assets will, in fact, one day be on-chain.

Others, like Tom Lee at Fundstrat, think whichever L1 wins the real-world asset race (think tokenized stocks, tokenized real-estate and stablecoins which is just tokenized debt) will see its token explode higher in value in lock-step proportion to the assets they secure on-chain (he of course thinks ETH will be the winner), while Matt Hougan at Bitwise has argued that blockchains haven’t even come close to full utilization, and when they do, the token of the L1 blockchain will flourish. Both are in line with our views. More recently, Haseeb Qureshi of Dragonfly and Santiago Santos of Inversion

had their own debate on L1 valuations. Truthfully, I didn’t watch it, but I can probably summarize the whole conversation anyway:

Haseeb: “Network effect…. Metcalf’s Law…. Facebook growth… huge TAM X probability of success.”

Santiago: “Blockchain fees are heading to $0… SOTP analysis shows they are all overvalued… Crypto only has 40mm DAUs which is tiny compared to Facebook and OpenAI… apps generate the value, not the protocol”

I’m generalizing because nothing has changed. We’re 8+ years into the smart contract protocol wars, and we still have no idea how to value these assets.

Enter Canton Coin (CC). Without going into too much detail, Canton Coin is yet another new blockchain (because we really need more blockspace) basically owned and operated by major banks, brokerages and exchanges, designed specifically for TradFi firms to manage loans, repos, derivatives, margin, and collateral on-chain. Digital Asset, the company behind Canton Coin,

raised another $50 million last week from Nasdaq, BNY Mellon, iCapital, and S&P to build Canton Network, and have now raised $450 million in total including investments from Goldman Sachs, Citadel, Optiver, Polychain, Binance (YZi Labs), TradeWeb, JP Morgan, DRW, and Virtu. That’s certainly a who’s who of heavyweight titans.

Supposedly, Canton is doing $500K+ in daily revenue. I say supposedly, because this is basically a private chain. Network usage data is intentionally opaque due to Canton’s configurable privacy model, making it difficult to underwrite fundamentals. Unlike Ethereum, Solana and other smart contract protocols, Canton does not broadcast every transaction to every node. Instead, privacy is configurable per contract and counterparty set. Basically, everyone sets their own terms. Privacy is the main reason Canton has been able to attract such massive RWA TVL compared to other chains, since major financial institutions don’t want every single transaction they do to be seen and scrutinized by the world.

Intuitively, this makes sense. And by all indications, the Canton network is doing great (take with a grain of salt, since these indications are coming from massive CC investors). Yet the CC token is going straight down as well. Which, ironically, probably validates my thesis that L1 token valuations are primarily driven by social value rather than financial or utility value. How do I know? Because Canton Coin has NO social value. It’s not cool to be part of a private Wall Street cabal coin, so CC carries no social premium and therefore gets little to no credit for any other successes it may or may not be having.

I actually think Canton has a higher probability of success than most other L1 chains. Since the only point of a blockchain is to move assets, and since 99% of the world's assets are not yet on-chain, any lead one L1 has over another today is meaningless. The winners have yet to be anointed. As I’ve stated before, the made-up crypto assets that run on blockchain rails today are largely irrelevant compared to stocks, bonds, real estate, and other TradFi financial assets that will eventually move on-chain (over $600 trillion in assets). Since most of these assets are controlled by the companies Canton is partnering with, it stands to reason that Canton has a higher probability of success than most other chains.

But I also think that Canton's win may invalidate almost everyone’s thesis about investing in L1 tokens. A major base case for chains these days is having people spend as little as possible to transact. Fees are likely to trend toward $0, reducing financial value. And you barely need to hold or use the tokens to operate the network, which reduces the utility of the tokens.

So that leaves social value as the only reason that these tokens retain value, and that social value declines, or is diluted, every day. Canton will never have meaningful social value. They might as well have called it “Occupy Wall Street coin.”

Again, ironically, fanatics of other L1 chains often celebrate whenever a member of the Wall Street cabal joins their chain, presumably for the reasons above. They control the world’s assets. But the reason these partnerships no longer drive token prices higher is also the same as the reasons above: they don’t create any utility or social value, and the financial value added is minuscule and declining.

From what I understand about Canton Coin (CC), the volume Canton is doing is irrelevant. Canton burns the token based on the fees they take per transaction. So if the burn is based on the blockspace used rather than the volume transacted, then the giant banks aren't really any more valuable to Canton than some random dude putting through 10,000 small trades per day. If it were based on volume, the financial value might grow large enough to warrant the token's valuation.

So let’s go back to the arguments about L1 blockchains having massive TAM, and using Facebook and other social networks as examples. It’s great to have so many people in one room. But the people in that room aren't valuable if they are doing nothing and can’t be monetized. To monetize the network, they have to do something. And what we’ve learned over the past few years is that the only actions anyone does on a blockchain involve stablecoins and DeFi. Yes,

everyone wants their own L1 blockchain, because vertical integration is the only way to survive.

- The L1 blockchain itself controls and organizes the users

- Developing your own stablecoin gives you a high-margin revenue stream

- Developing your own DEX gives you a high-margin revenue stream

What we’ve learned over the years is that it doesn’t matter what order you do this in, but you need all 3.

- Binance, Coinbase, and Hyperliquid started as an exchange, then built their stablecoin and L1 later

- Circle and Tether started as stablecoins, and are currently looking for ways to build their own L1 and DEX

- We’ve yet to see something start as an L1 and then successfully build its own stablecoin and DEX, but we’ll probably see that soon, with the Solana community already talking about it.

The L1 itself isn’t valuable until you control DeFi and stablecoins on top of it to make money, which is why all of these L1 tokens continue to trend lower, even if collectively L1 tokens may be worth a lot more one day.