What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

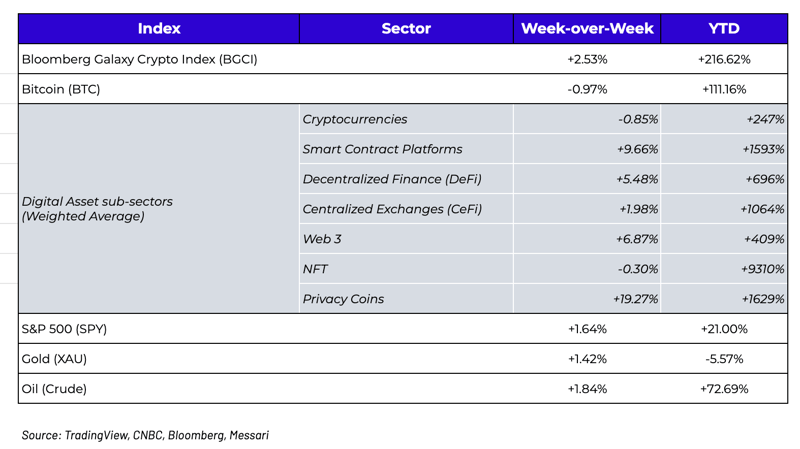

Week-over-Week Price Changes (as of Sunday, 10/24/21)

Is Inflation or the Bitcoin ETF driving prices?

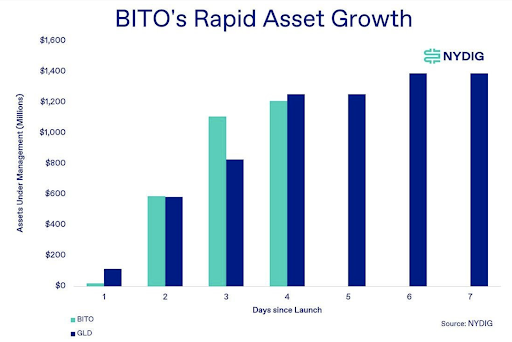

The SEC approved the first futures-based bitcoin ETF, propelling Bitcoin to an all-time record just north of $67k on Wednesday before losing steam and ultimately ending the week down 1%. The ProShares Bitcoin Strategy ETF (BITO), which gains exposure to Bitcoin through futures contracts on the CME (and all of its flaws), saw near-record volumes and asset growth. The fund has raised $1.2 billion in assets thus far, and seems to be on pace to do exactly what the GLD ETF did for Gold. It’s worth noting that almost all of the ETF demand has been via small trades, not large chunky blocks that are more typical for institutions, which would indicate that most of this new demand is coming from retail investors. This is both surprising and not surprising. The ETF was supposed to open up a new channel of institutional demand from those previously shut out of the market, but instead, it appears that the over-saturation of Bitcoin products in the last few years may have already met the demand. My best guess is that most of the demand for the new ETF is coming from investors who already own Bitcoin in some fashion, but may have excess cash sitting in brokerage accounts sitting idle, and pouring it into this ETF is easier than transferring it to Coinbase or elsewhere.

Source: NYDIG

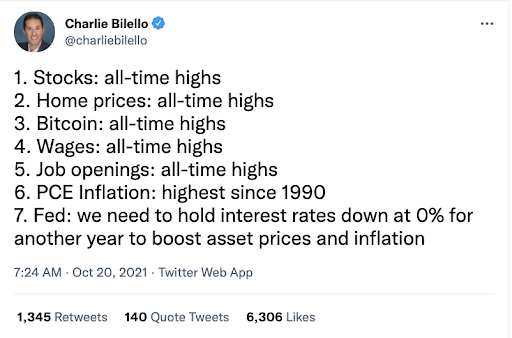

While the Bitcoin ETF gets the credit for Bitcoin’s 40%+ increase MTD, it may not actually be the cause of the rising demand. While Bitcoin correlations are almost always changing, it’s hard not to notice what else has happened this month:

- US equities once again set new all-time records.

- The Vix has retreated to a near six-month low, reaching its lowest since before pandemic lockdowns began.

- The entire US Treasuries curve has sold off again amid expectations that the Fed will hike rates sooner than expected, as inflation pressures mount.

It’s been exactly 18 months since Paul Tudor Jones famously released his inflation thesis, which included for the first time a recommendation for owning Bitcoin (as one of many inflation-based trades). Just last week, Tudor Jones said inflation could be worse than feared, that it is the biggest threat to markets and society, and that it is time to double-down on hedges. Like PTJ, other fund managers have found plenty of ways to play the inflation trade:

- Short bonds

- Treasury curve steepeners

- Long bank/energy stocks

- Long floating-rate notes

- Long real estate

- Long Gold

- And of course long Bitcoin

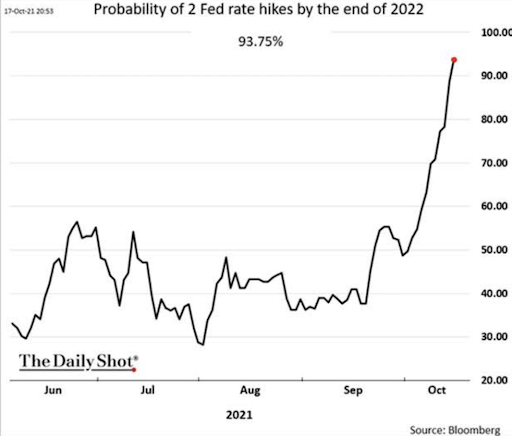

These trades largely failed during the 2Q and 3Q when the market began to believe Fed Chairman Powell’s “transitory” thesis. But in the past few weeks, the market has begun to express concerns that inflation is far from transitory. These renewed inflation fears are resulting in futures markets predicting Fed rate hikes with 95% certainty that the Fed will be forced to hike twice next year.

Source: Cliffwater

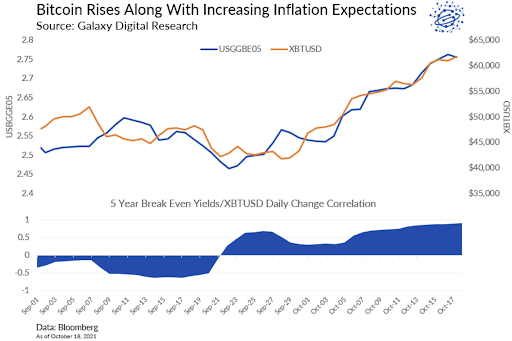

Notably, inflation expectations have moved in tandem with Bitcoin.

Source: Galaxy

While the ETF is a huge win for Bitcoin investors, its effects on the market were probably short-lived, as evidenced by the “buy the rumor, sell the news” reaction in price. Inflation, however, might be the real catalyst.

Mt Gox Resolution and Distributions Are Finally Moving Forward

[Written by Arca Funds COO, Mike Dershewitz (former Head of Research at Distressed Firm, Brencourt)]

Last week was the beginning of the end of one of the most infamous sagas in the history of digital assets: the hack, insolvency, and seven-year bankruptcy of Mt Gox. It was announced that over 150,000 victims creditors totaling 99% of claimants and 83% of claims voted in favor of the estate’s rehabilitation plan. This approval sets distributions of the remaining Bitcoin, Bitcoin Cash, and yen on or around November 20th.

First, some background. Mt Gox was founded in 2007 as a Magic the Gathering card exchange, after which it pivoted to Bitcoin in 2010 (fun fact, Mt Gox stands for “Magic: The Gathering Online EXchange). In 2011 the French developer Mark Karpeles bought the site, moved the company to Tokyo, and grew it into the world’s largest Bitcoin exchange by 2013. Mt Gox accounted for nearly two-thirds of all Bitcoin volume during those formative crypto days. Behind the scenes, however, the exchange lacked functioning security and became a hacker paradise - between 2011 and 2014, a series of hacks stole over 850K Bitcoin, worth $55B today. As a result, Mt Gox became insolvent, shut down its website, and filed for bankruptcy in Japan in February 2014. Over the following seven years the trustee worked through the courts to manage the claims pool, subordinate supplier claims, and most importantly, trace the stolen Bitcoin. Over 200K Bitcoin were located in old wallets in 2014, but 650K Bitcoin ($42.5B) still have never been found to this day.

Approval of the bankruptcy plan this week was certainly aided by Bitcoin simultaneously hitting all-time highs. The creditor estate today totals $1.7B worth of JPY, 142K Bitcoin (worth about $9B), and 143K Bitcoin Cash obtained in the 2017 fork (some of the recovered BTC and BCH were previously sold to fund expenses for the estate). Using Bitcoins as units, creditors will disastrously only recover ~20% of their original holdings. However, from a fiat point of view, creditors are celebrating a windfall as recoveries are 42x their February 2014 claims, driven by Bitcoin moving up from $300 to $65K. Distressed debt specialists, especially Fortress, purchased significant amounts of claims from customers at a discount throughout the proceedings and stands to realize even greater returns.

Given the long-awaited creditor liquidity as well as the distressed investor dynamic, some in digital asset markets expressed fears of selling pressure upon the November distributions. We believe that these fears will prove overblown. While $9B of Bitcoin is not insignificant, it is just 25% of average daily trading volumes and should therefore be ingestible by normal markets. The Bitcoin Cash recovery is an even lower percentage of average daily trading volume at just 6%. Additionally, we believe that many retail creditors will ride their windfall and “hodl”, this time happily and voluntarily. Perhaps even more importantly, the $1.7 bn in cash distributions (Yen) will likely be poured back into the digital markets, likely into new types of assets that weren’t around when Mt Gox first became insolvent, like DeFi, Gaming, NFTs and more. This has the potential to create much more of a tailwind for non-BTC assets than any potential downward pressure caused by selling of recovered BTC and BCH.

It is important to reflect on the lessons of Mt Gox now that the end is finally in sight. First, hacks continue to this day, including a $600M hack of the Poly Network in August 2021 that exploited code vulnerabilities. On the other hand, investors today have numerous options to protect against exchange hacks and smart contract failure, for example purchasing counterparty and principal insurance from decentralized insurance mutual, Nexus Mutual. Third, advances in wallet security makes it less likely for a Mt Gox hack to occur at a properly vigilant exchange, and improved custody options now safeguard private keys. Finally, this market has become so saturated and fragmented that even 10 minutes of due diligence would likely help an investor avoid some of the more vulnerable counterparties, and gravitate towards those that have proven track records.

It is somewhat remarkable to witness where the digital assets market stands today after such a tumultuous beginning. But the large creditor recoveries here once again prove Baron Rothschild’s maxim that when there is blood on the streets, investors should always be buyers, not sellers.

The Digital Asset Community Enters the Wu-Tang Web 3.0 Clan

[Written by Arca Senior Macro Analyst, Nick Hotz]

With digital asset investors rightly transfixed on the bitcoin ETF and subsequent all-time highs, other news flew under the radar. But a cover story from the Rolling Stone caught our eye, which highlighted the purchase of Once Upon a Time in Shaolin, a unique album by legendary hip-hop group the Wu-Tang Clan. Only a single copy of the 2015 album exists, as the release of the album served as a protest over the low value assigned to music, and to artists under the current streaming business model. Additionally, it comes with a legal stipulation that the album cannot be resold (except, hilariously, if a member of the Wu-Tang Clan or actor Bill Murray steals it). The album was originally purchased for $2.2 million by former hedge fund manager Martin Shkreli (the controversial figure behind the 56x price raise of the AIDS drug Daraprim from $13.50 to $750/pill). Shkreli was notably stingy in letting others listen to the album and even threatened to potentially destroy it. Once Upon a Time in Shaolin was eventually seized by the US government after Shkreli's arrest and conviction for securities fraud.

The new purchaser, PleasrDAO, is a decentralized autonomous organization (DAO) that comprises builders and investors in the digital asset space. The DAO owns a portfolio of nonfungible tokens (NFTs) associated with crypto and meme culture such as a work by Edward Snowden, and the original Doge meme (which was incredibly innovative with regard to fractionalization and resale, making almost 100x overnight). Through some complicated legal measures and a third-party intermediary, the DAO managed to have the Wu-Tang album turned into a non-fungible token (NFT) and purchased the NFT and the album from the intermediary for $4 million in stablecoins. In contrast to Shkreli, PleasrDAO head Jamis Johnson says it intends to attempt to distribute the album to the public as best as it can under the legal circumstances.

While the Rolling Stone article framed the purchase as a feel-good tale of the democratizing heroes pulling one over on a notoriously unscrupulous villain, there is another story to be told here: the story of how blockchain technology and digital assets solve the very problem Once Upon a Time in Shaolin was created to protest.

The transformation of the music industry from one driven by sales of CDs or individual tracks directly to fans to one where streaming services stand in the middle was an incredible boon to listeners, who are able to access nearly unlimited music for around the cost of a single CD per month. However, this shift left all but the most popular artists in a tough position. Spotify, for example, pays artists about $0.0033 per stream, with artists requiring around 250 streams to earn a single dollar (or a quarter million streams to earn $1,000). While famous artists like Taylor Swift and Jay-Z have in the past lamented and even tried to subvert the existing system, the network effects accrued by middlemen like Spotify have by and large overpowered single players trying to change the system.

The new business models enabled by blockchain and digital assets have the potential to disrupt the powers that be in the music industry. Fractionalization, for example, is one avenue PleasrDAO could take towards publicizing the Wu-Tang album. Fractionalization is the process of breaking up a unique NFT into a fungible asset represented by tokens to distribute ownership. For instance, the DAO could create 1 million tokens and specify that each whole token would entitle the holder access to an event where they could hear the album. Not only would fans be able to finally listen to the famously secret album, but unlike owning a CD, they would also receive an equity-like partial ownership over it. The current business model of streaming creates a fundamentally competitive dynamic between fan and artist (paying the artist more for streams requires charging fans more in subscriptions). A fractionalized NFT however serves to align the fan’s interests with those of the artist.

Electronic artist and long-time digital asset enthusiast Justin Blau (better known by his stage name 3Lau) has taken a slightly different approach, launching a platform for artists to share streaming revenues with their fans, even more closely aligning their interests with those of the artist. Blau sees the platform as a way to cut out record labels, which notoriously monopolize promotion and distribution for up-and-coming artists in exchange for a large portion in the artist’s future, already diminished, earnings. Add in social token platforms like Rally and Socios that allow fans to gain even greater access to artists and create micro-economies of supporters to the mix, and we begin to see an entirely new musical creator economy emerging. This new music economy fundamentally aligns the interest of creators and their fans and returns the profits of streaming middlemen to these groups. While we’re only in the early stages of the music industry renaissance currently, it’s starting to resemble something like what the Wu-Tang Clan might have hoped for when they released Once Upon a Time in Shaolin almost 7 years ago.

By aligning incentives of previously competitive actors in the economy, digital assets can democratize access to goods and services previously only available to the wealthy few. This innovation certainly isn’t limited to the music industry. Axie Infinity, the blockchain-based monster battling game, has become incredibly popular in the Philippines, where banking services don’t reach a good portion of the population but mobile phone and internet penetration rates are relatively high. Axie’s creator, Sky Mavis, stated that 25% of its players have never had a bank account before. This means that in addition to players earning assets for playing the game, Axie wallets are the first financial service many have ever had access to. With the recent release of staking for yield on the native Axie token AXS, a brand new mobile game has delivered a high yielding savings account to hundreds of thousands of players where the entire existing government and banking infrastructure failed to do so.

Let’s go even further. Long have we heard experts in the telecom industry extoll the paradigm shift that 5G technology will bring to the wireless landscape and even to geopolitics. There’s again one major problem with this: a lack of alignment of interests. Unlike previous iterations’ cell towers, 5G relies on companies distributing tons of nodes throughout the service area, including likely on privately-owned property. While distribution may be possible via government coercion in more authoritarian regimes, in democracies, 5G suffers from a severe case of “not on my lawn syndrome”. We seem to be at a fundamental impasse, with the public good of 5G signal being highly desirable, but neither the private nor public sector able to produce a favorable outcome. Enter Helium, which financially incentivizes people to run nodes and last week accrued its 250,000th hotspot for a long-range signal and is rapidly rolling out 5G capabilities. The result -- hundreds of thousands of happy service providers, one extremely complex and beneficial public good in development, no coercion in sight, high alignment of interests.

Web 2.0 at the most basic level was about creating markets (of music, of goods, of social information, etc.). The companies facilitating these markets became fabulously powerful, shifting economics away from market participants and towards the companies themselves. Enabled through the power of digital assets and communities, Web 3.0 companies turn markets into public goods by aligning their own interests with those of market participants. Instead of playing competitive games with their users, Web 3.0 companies play collaborative ones, creating even more value that can be returned back to those users. Whether it's gaining access to basic banking services, receiving 5G signal or listening to a rare hip-hop album, we’re just starting to see the incredible value users receive from public goods created by decentralized organizations. If PleasrDAO can finally bring Wu-Tang back to the people, there’s no telling what else blockchain-enabled organizations can achieve.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM

Alex Woodard - Research Analyst

Andrew Stein - Research Analyst

Nick Hotz, CFA - Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Trading Operations

David Nage - Principal, Venture investing

Michael Dershewitz - COO of Arca Funds

To learn more or talk to us about investing in digital assets and cryptocurrency