What happened this week in the Crypto markets?

Staking was the Theme of the Week

The Bloomberg Galaxy Crypto Index rose 3% last week, its 7th positive week out of 8 this year. For those checking price once per week, or even once per month, it’s been a pretty fun and profitable year. In the trenches, however, February has been one of the more difficult months to assess, as we have had numerous sharp moves in both directions, with a fair amount of jockeying at critical technical levels. Further, most digital assets have moved somewhat irrationally in February, compared to January, where each sharp move higher had a well defined catalyst.

This past week was no different. Following a sharp selloff over President’s Day weekend, the market shot back to YTD highs mid-week, only to once again get rejected and come crashing back down. Even as we write this, the market has gyrated in a 5% range (on a Sunday night no less).

Thematic Investing in Crypto

But as always, there is a maturation process happening beneath the volatility, one which we’ve discussed many times in the past. Thematic investing in crypto. The biggest winners this week were tokens that offer a yield via staking. Many top crypto exchanges, like Binance and Coinbase, are becoming “one-stop shops”, and their latest offering is to make staking processes easier for investors by doing it for you. This is a form of prime brokerage that the market desperately needs, and is not (and arguably cannot) be filled by niche up-and-comers who are focused on single service offerings (for example Staked, which will arguably be acquired or simply left for dead as the 800 pound gorillas take over).

There are many developing themes happening in 2020 (in fact “Staking” was one of our top picks), and we’re happy to see the market beginning to recognize this.

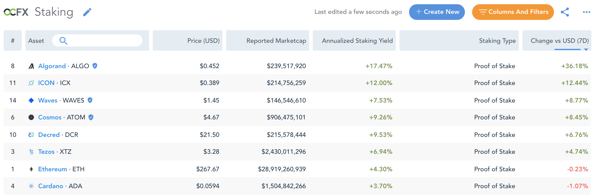

Week-Over-Week Price Change for Staking Tokens

The Bitcoin Auction -- US Government sells ~$40mm BTC to two investors

As we discussed a few weeks ago, the US Government auctioning Bitcoin was neither bullish nor bearish from a price standpoint, but it was incredibly powerful from a narrative standpoint -- this is a backdoor way of saying that “Bitcoin isn’t going away”.

However, some of last week’s intra-week volatility may have been created by the auction, by way of interesting game theory.

Of course, $40 million is a drop in the bucket in traditional asset classes. For context, in the 4Q of 2019 alone, $9.3 billion in IPOs priced in the US, with the average 2019 raise equal to $279 million. The corporate debt markets

issued almost $1.5 billion of bonds in 2019, plus hundreds of millions, and sometimes billions, of dollars in BWICs (“Bid Wanted In Comp”) clearing nearly every week in the secondary market. Bitcoin itself has a $175 billion market cap, with average daily volume (ADV) in the $1 billion range. Additionally, miners create 1800 new BTC per day (~$18mm USD), and while they don’t necessarily sell it immediately, this can certainly be considered new daily supply that is absorbed by the market.

So a $40mm auction by itself isn’t super meaningful. But the dynamics of the auction were. Bidders had to submit their bids prior to 2pm EST on Tuesday, Feb 18th. Thereafter, from 2pm to 5pm EST, no individual bidder knew if they were going to win, until 5pm EST when the auction results were announced.

Let the game theory begin!

- Let’s say only $40mm worth of bids were entered -- this would be entirely efficient, every dollar submitted would be used to purchase, and any bidder could sell before, after, or not at all after receiving their Bitcoin.

- But let’s say there were $400mm worth of bids, and 90% of bidders would therefore not receive what they bid for. Of course, they (and the market) don’t know the outcome.

As a result, from 2pm to 5pm EST, some amount of capital was tied up bidding for Bitcoin, with no guarantee that it would actually be used to purchase Bitcoin. However, we knew for sure that $40mm was ultimately being sold.

If there were $400mm worth of bids, even though that's ultimately bullish (more demand than supply), for a brief three hour window, it becomes bearish because none of that potential demand could be used to buy more Bitcoin while their bids were tied up. If a large player in the market was short, and assumed there would be more demand than supply, they could drive down the market during the three hour window knowing bids would be sparse while demand is locked up in the auction. Conversely, it would be incredibly bullish if very few bidders actually won in the auction, as they would presumably have to buy in the open market after finding out that they didn’t get filled in the auction (perhaps that caused the run-up in price prior, and during the auction). In fact, the most bullish scenario would be that virtually NO ONE in the crypto markets won the auction, because a non-crypto investor (like a Bridgewater, Blackrock, or Millennium) came out of the bleachers to take down supply sold directly by the US government, thereby bypassing many of the crypto OTC and Exchange dealers in the process). Perhaps this government issued block could have even been taken down at a premium since this was a chance to buy crypto “legitimately”.

Then again, those who won in the auction may have sold it quickly after winning, or may have even had synthetic exposure prior to the auction just in case they did not win (and would therefore reduce risk upon winning). Perhaps that led to the decline in price the following day.

Bitcoin Price Volatility around the US Government Auction

Source: TradingView

A Guide to "Ethereum Not ETH"

An investor's guide to Ethereum not ETH. Frequent readers of “That’s Our Two Satoshis” know that we purposefully avoid getting technical -- we are investors, therefore we focus on relevant investing themes, not code. There are plenty of other great blogs out there for those that want to get into the development weeds (Hat tip to some of our favorites: Coinmetrics, the Defiant, TowerWatch, VeradiVerdict, OurNetwork).

But we may not have a choice when talking about Ethereum. Ethereum is the #2 digital asset by market cap (ETH currently stands at $29 bn), the #1 protocol in terms of value and relevance to the digital asset ecosystem, and arguably the #1 ranking in terms of “most annoying crypto twitter community”. Ethereum has undoubtedly become a critical, yet confusing household name in digital assets.

But what is Ethereum? Unlike Bitcoin, which is (relatively) easy to understand since its value proposition is well-defined (immutable, store of value, censorship resistant money that allows for incredibly fast and cheap global asset transfer), Ethereum does a little bit of everything. The ability to write smart contracts using the Ethereum protocol has opened the door to a variety of innovations, from non-fungible tokens (NFTs), to Decentralized Finance (DeFi) to decentralized applications (dApps). Ethereum’s success has also paved the way for tens (if not hundreds) of “Ethereum killer” copycats, none of which have proven any real success to date, but all of whom claim to solve for some sort of problem that Ethereum has not (or cannot).

From a non-technical perspective (the extent of my coding experience is writing a few macros in Visual Basic Editor for Microsoft Excel), Ethereum allows you to write if/then statements. This basic logic is extremely powerful -- in modern finance alone, everything from bond coupons, to equity dividends, to legal contracts and debt covenants use human functionality that can be replaced more efficiently by code. There’s a reason why so many financial firms are now experimenting using the Ethereum blockchain (HSBC, Santandar, JPM, SocGen, Wells Fargo and even Arca itself).

Ethereum is truly amazing, but is the ETH token that powers the Ethereum blockchain actually “investable”? ETH is no doubt valuable (if you use Ethereum applications or develop on the protocol), but it remains to be seen if valuable as a utility in the ecosystem translates to valuable as a stand-alone investment. Unlike other digital assets that are more easily quantifiable, the value capture mechanism for ETH is much more nuanced. The fat protocol thesis seems outdated, and the bull case is somewhat untested.

Vision Hill, the leaders in making sense of digital assets for institutional investors, articulate this well:

“... we are seeing that ETH is not (directly) capturing the value of all the assets launched on its platform; instead, value is getting captured in the applications. There are likely to be several reasons for this, but we think one theory summarizes it best: most applications and tokens (e.g., ERC-20, ERC-721, etc.) built and issued atop Ethereum may, in a large sense, be parasitic to Ethereum. ETH token holders, by holding ETH, are paying for the security of all these applications and tokens, via the inflation rate of ETH that is currently given to the miners. Therefore, ETH token holders are being diluted slowly, but the ERC-20, ERC-721 and other application token holders are not. Such token holders that are building and using systems launched on the Ethereum blockchain benefit from the security that comes from the dilution of ETH holders, but do not currently pay for any of it. As these token holders and smart contract developers utilize gas for transaction fees in order to interact with the base Ethereum blockchain, it does drive demand for ETH, but the problem (currently) is it drives demand for just one block, and then those transaction fees go straight to the miners (who are generally the largest sellers in proof-of-work systems).”

Of course, I’m stepping right into a trap here. A common fallacy that we hear is “I like Blockchain, not Bitcoin”, which can be refuted fairly easily. Ironically, however, I’m essentially saying “I like Ethereum, not ETH”. That too will be shot down by many in the Ethereum community, perhaps for good reason. In fact, this is probably the best explanation of ETH’s value proposition that I’ve ever read.

But the argument here has little to do with whether or not ETH’s price will go higher (ETH is +46% MTD, +105% YTD, and over +86,000% since inception). Rather, the argument is “do you need to own ETH as an investor who does NOT use anything in the Ethereum ecosystem?” If you don’t play dApps, you don’t take out DeFi loans, and you don’t need ETH to power your day-to-day online life, does it still make sense to own ETH in your portfolio?

In some ways, ETH has become an “altcoin ETF” -- so highly correlated to all other non-Bitcoin tokens, that it is no longer impactful. I fully expect ETH to go higher, so in absolute terms, ETH of course is very investable. But in relative terms, since so much of the digital asset ecosystem is now driven by Ethereum’s success, it’s possible to capture ETH’s upside, and avoid ETH’s downside, without ever owning ETH itself. For example:

- If you’re bullish specifically on DeFi, you can buy pure play DeFi tokens (like SNX or MKR)

- If you’re bullish specifically on Decentralized trading, you can buy DEX tokens (like ZRX or KNC)

- If you’re bullish on smart contracts, you can own price oracle tokens (like LINK or TRB)

- If you’re bullish on dApps, you can own individual application tokens (like BAT, FOAM or MANA)

- If you’re bullish on overall growth of digital assets, you can buy exchange tokens that facilitate in trading (like BNB, HXRO, FTT or HT)

Notwithstanding the merit of any individual token mentioned above, the point is ETH is now the “generic” investment, whereas skilled researchers can pick winners that capture more leverage to ETH’s upside.

The flipside of course is that picking winners is difficult (very difficult), ETH is the “safer bet”, and ETH is much more liquid (though liquidity is a crutch -- good risk managers can navigate around illiquidity like they do in other asset classes like corporate bonds, distressed debt, emerging market equities, and reorg equities). But investing is about finding the best way to express a view, and as a result of Ethereum’s success and subsequent spinoffs, there are now hundreds of different ways to express more tailored individual views besides owning ETH.

This is naturally an unpopular opinion in the crypto world. Many will read this as “anti-ETH”, which it is most definitely not. Owning AAPL stock does not make you anti-S&P 500. But as we stated earlier in today’s writeup, the digital asset industry is maturing, and this maturation process brings intelligent debate and differences of opinions. We look forward to rebuttals.

Notable Movers and Shakers

Welcome to the 9th week of consecutive Bitcoin Dominance decline (50bps), the longest recorded consecutive decline since the metric was tracked in March of 2014 (BTC.D). While much of this can be attributed to Ethereum rallying (and the rest of the market following suit), it is a noteworthy development nonetheless. Historically, Bitcoin tends to leech dominance away from the market (if you nullify the stats prior to 2018, which were obfuscated by the rise and fall of the ICO craze). This week, the notable movers came from a very specific subsection of digital assets - stakable assets:

- Kyber Network (KNC) has been gaining momentum, as noted by an update they sent out showing that over $100m in on-chain trading volume has happened on the network in February alone. Kyber also announced details on their upcoming Katalyst upgrade (Q2 2020), which will feature the KyberDAO and staking on the Kyber Network. To top it all off, KNC got the nod from Coinbase and is expected to list sometime next week. KNC rallied 42%, marking its 6th consecutive positive week.

- Aion (AION) has been a benefactor of the resurgence of staking, announcing last week that over 100m AION ($14.5m) has been staked to secure their hybrid PoW/PoS network since it went live 3 months ago. This combined with the new trading pairs available on Binance, sent the coin 37% higher last week.

- Algorand (ALGO) spent much of last year in the red, falling precipitously from its first public listing price of $2.40 down to $0.20, but may have finally bottomed this month. ALGO rallied 49% on the week as part of the staking theme, as well as renewed interest in news that came out 3 months ago which limits selling pressure from equity investors.

What We’re Reading this Week

Last week, payments giant Visa granted crypto exchange Coinbase principal membership, allowing the exchange to issue debit cards without the expense of using a middlemen. This membership is the first awarded to a cryptocurrency business. Coinbase can now issue debit cards for its users to spend Bitcoin, Ethereum and XRP anywhere Visa is accepted and the rollout will start in 29 countries later this year. This marks an important step for retail users of cryptocurrency to be able to spend their crypto on everyday goods and services.

Sweden’s Risibank last week announced that it had begun testing its Central Bank Digital Currency (CBDC), the e-krona. As a country that is the least cash-dependent country in the world, the introduction of a CBDC could be beneficial for commerce and an excellent litmus test of how countries can adopt digital currencies. Risibank envisions that the e-krona will be used for everyday banking activities and will have a mobile phone app wallet to facilitate these activities. They expect the pilot to run until February 2021.

JP Morgan released a 74 page report last week covering blockchain, digital currency and cryptocurrency and most importantly the question of whether it is finally moving into the mainstream. The report explores topics of mainstream adoption, the rise of alternative payments and whether stablecoins are a scalable alternative to cryptocurrencies. While it highlights the progress that has been made in the areas of payments and digital money, there are still many issues to be addressed such as network scalability.

The Internal Revenue Service has invited a number of crypto firms to participate as panelists at a summit in March. The panelists will focus on technology, issues faced by exchanges, tax returns, and regulatory compliance. The purpose of the summit is to better inform the “IRS’s thinking”, although many hope it will aid in the development of a better regulatory framework around cryptocurrency. Last fall, the IRS released new tax guidance around hard forks and calculating gains, but does not provide clarification on hard forks and small transactions.

The Paxos Settlement Service launched last week, marking the first time equities were settled on a blockchain-based system. The system received a no-action letter late last year from the SEC and was built in conjunction with Credit Suisse and Société Générale. The current system will run as a pilot for 24 months and will include 7 participants who are limited to 100,000 trades per day. Paxos also intends to apply for a clearing broker-dealer license with the SEC this year, enabling it to offer the blockchain settlement service to any broker-dealer settling US equity securities.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)