What happened this week in the Crypto markets?

What a Start to the Year

Bitcoin and other digital assets rose 8% on average last week, capping off the best January for crypto prices since 2013. As we pointed out mid-month, the majority of the largest gains have been made by last year’s biggest losers, which may indicate that last year was oversold, or that this year’s hot start may be fool’s gold.

That said, a look behind the curtain indicates that most of the digital asset gains made thus far in 2020 were due to real factors. A combination of technology upgrades, UI/UX improvements, partnership announcements and changes in token supply structures were the catalysts for increased enthusiasm, and thus increased buying.

Arca's Rationale on Crypto Tokens

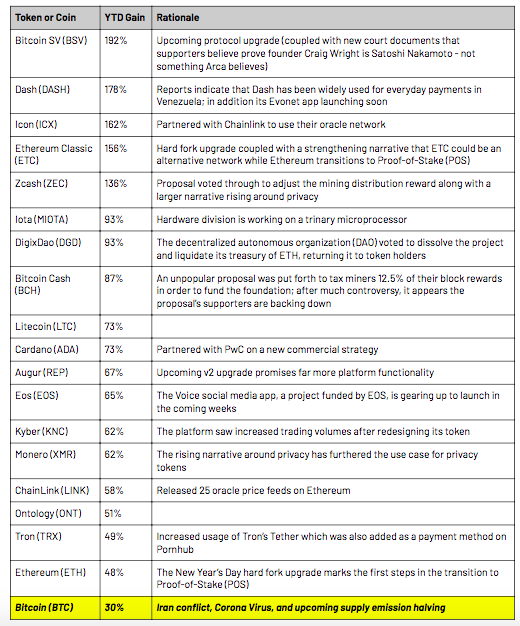

Below you’ll find Arca’s rationale for each of the major crypto tokens that outperformed Bitcoin in January:

Clearly some of these catalysts were stronger and perhaps more sustainable than others, but they were in fact catalysts. For those more familiar with traditional technology startups, these would be considered Key Performance Indicators (KPIs). Traditional startups often raise incremental financing rounds (Series A, B, C, etc) at higher valuations based solely on KPI growth, even if they are far from revenue and/or profitability. Investors reward growth and progress, and this is now happening in crypto. Simultaneously, these upgrades and growth engines increase the utility of these tokens, which forces early users of their platforms to acquire and use more tokens.

Looking back on January, it wasn’t difficult to make money as an investor. Almost everything went higher, even several tokens that had no catalysts. Naysayers will of course point to high correlations as reasons for not looking at anything other than Bitcoin. But once again these numbers remind you that correlation does not take magnitude into account. Two perfectly correlated assets can still have a very wide dispersion of returns over time. So while the whole asset class went up together in January, those making real progress will sustain greater gains than others over longer time frames. And much like traditional startups, some of these projects are wildly overvalued based on more hype than substance, while others have much clearer upside value propositions. Time will tell, but for now, it’s quite clear that Punxsutawney Satoshi did not see his shadow. Spring is here!

Watch Out For Increased Leverage

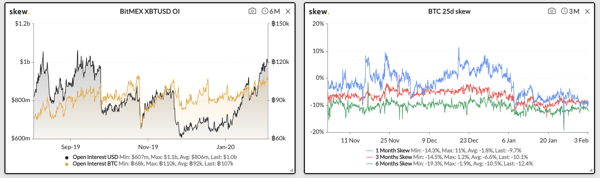

While the first two weeks of January were caused by spot buying and new cash being put to work, the last two weeks of January were certainly influenced more by an aggressive use of leverage. In the charts below, you can see that open Interest on Futures platforms has skyrocketed (indicating borrowed money as these platforms allow for up to 100x leverage), and skew has turned sharply negative (indicating calls are much more expensive than puts due to aggressive levered buying, which puts pressure on market makers to delta hedge, creating even more buying pressure).

Open Interest is rising and Put Skew is Negative

Not all of this leverage is pure speculation. Some of it has been caused by new product launches that attract new investors, like the CME introducing options and Bakkt introducing futures. Further, the inefficiencies in this young asset class often cause massive dislocations that are only exploitable via derivatives. For instance, currently the annualized basis between spot and futures markets is over 20%, making it very profitable to borrow US dollars, buy spot, and sell futures (for those who want to dust off their CFA books, this cash-and-carry trade works extremely well when interest rates are low and storage costs are non-existent). But this arb persists because there just isn’t enough money (and collateral) in crypto yet to fully take advantage of these “risk-less” trades.

Regardless, an increase in leverage and speculation generally doesn’t end well. “Levered unwinds” can occur in a flash, especially when the underlying assets are no stranger to 5-10% daily moves. We’ll be monitoring this closely -- as a tug-o-war is now brewing between real growth and uncomfortable speculation.

Not all Crypto Ideas are Good Ideas

We’re big believers in the growth of digital assets. Bitcoin has a great chance to become a global currency and a store of value, Ethereum is making great strides towards “Decentralized Finance”, and several other experimental applications are showing promise. We love the idea of tokenized contracts and salaries, we’re excited to see fractional ownership of hard assets (like collectible cars), and we’re intrigued by innovative use cases like a lottery that encourages saving instead of being a tax on poor people.

That said, not all ideas are good ideas.

The latest craze is people tokenizing their own time. In short, you can create a digital asset backed by yourself, and have this token trade peer-to-peer via decentralized token exchanges. If someone buys your token, you get money from them, and they can redeem the token at their convenience for a service (i.e. your time). Essentially you’re buying a gift card, where you pay upfront to redeem services later.

Experimentation is great, and Arca fully supports ingenuity. But the mechanics of these tokens simply make no sense. Price, demand for time, and supply of time are just not related at all in this concept. If someone decides to buy up a lot of tokens as an investment because he expects the token issuer’s services to be worth more in the future, that doesn’t reflect actual demand. It is just cornering the market like JP Morgan and Alexander Hamilton did in the 1800’s on actual street corners, hoarding sugar. Further, if actual demand for his services does skyrocket and prices rise, it doesn’t change the fact that the token issuer still only has 24 hours per day in which to offer his services. No one can redeem 1000 tokens all at once just because demand is high.

For free markets to work, supply, demand and price have to move logically. Tokenizing an “asset” like time is a novelty; pretending it is valuable is not how blockchain moves forward.

We applaud innovation. But we’re also realists.

Notable Movers and Shakers

In a week where the whole market trended north (only 12 out of the Top 100 digital assets by market cap had negative returns), it is admittedly hard to discern idiosyncratic movements from a general positive market environment. Bitcoin finished the week up 8%, with Bitcoin dominance leaking (-1%) for the sixth consecutive week. Instead of rehashing the movers (discussed above), we zoom out a bit and look at what is ahead of us:

- Bitcoin (BTC) is estimated to undergo its 3rd block halving on May 12th, which is just under 100 days from now. While the halving is an emission cut (Bitcoin is a disinflationary asset with emission on a decay curve), this will be the third example of the behavioral economics at play in the digital assets market. Regardless of which side of the fence one stands, this event will be on everyone’s calendar.

- Block.one, the parent company of EOS, have announced that the launch date for the beta of Voice on February 14th - the parent company made waves when they purchased the Voice.com domain name for the social media app ($30M), as well as purchasing $20M worth of RAM. Reports came out recently that Voice would not be released directly on the EOS blockchain at first, which came as a surprise to many. Nonetheless, this will be the talk of the town soon enough.

What We’re Reading this Week

In response to China’s digital currency ambitions, a number of central banks have announced plans to create their own national digital currencies. Importantly, however, Japan’s entrance into the foray is a complete reversal from Japan’s Central Bank’s guidance not to pursue a digital currency. The sudden and urgent change are centered around concerns over what will happen if China, who is far ahead in development, succeeds. For years, China has attempted to internationalize the Yuan so it may play a greater role in global commerce. For Japan, who is heavily reliant on international trade flows, a heavily used Chinese digital currency could threaten its sovereignty and strangle its economy.

Saudi Aramco, Saudi Arabia’s oil behemoth, has invested $5m into a blockchain-based trading platform for oil called Vakt. The platform is focused on post-trade processing for physical commodities and was founded by BP and Shell. Although currently only operating in the North Sea BFOET crude oil market, the company plans to expand to additional markets in the near future. The use of blockchain as the backbone of their platform has allowed Vakt to eliminate the paper-based processes and manual accounting practices necessary in the commodities trading space.

In a first for Switzerland, OverFuture filed its IPO prospectus with the intention of tokenizing its shares via IPO on Ethereum’s blockchain. According to the filing, the company is allowed to tokenize its IPO offering, which will reduce the number of counterparties involved and organize more efficient secondary market transactions. Although it is unclear which regulatory body would oversee such a transaction, this marks the start of a trend we believe will continue as crypto businesses seek public offerings.

According to Arcane Research, Google searches for “Bitcoin Halving” have doubled in January from December, and are at the highest level since 2016, during the last Bitcoin halving event. The report credits the increased number of searches to the upcoming halving event, at which time the number of Bitcoin created through mining is slashed in half (disinflation). The uptick in interest makes sense given the approaching event, however, Google searches for “Bitcoin” still far outrank the numbers for “Bitcoin halving”.

Well now you can own a piece of a Ferrari through CurioInvest, a new platform that is tokenizing collectible assets like vintage cars. This idea is not a new one - blockchain technology can allow for the fractionalization of assets such as cars, art, and other collectibles. CurioInvest, which partnered with digital asset exchange MERJ, plans to bring $200m+ worth of collectible cars to the platform, starting with a $1.1m Ferrari.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)