What happened this week in the Crypto markets?

What Corona Virus?

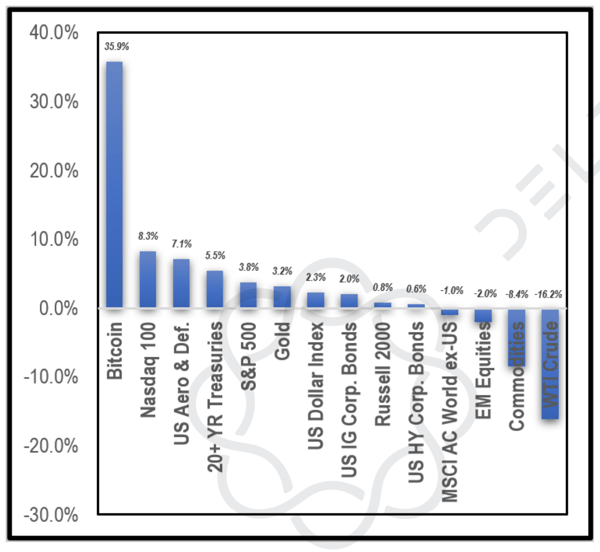

Stocks up...Bonds up...Gold up…Dollar up...

Bitcoin up. Investing in the crypto market is way up.

Here we go again. The “everything rally” continues.

YTD Returns of Major Asset Classes

While we’ve seen this before (2018 every asset class was down; 2019 every asset class was up), there is something different about the start of 2020. At the beginning of the year, most market strategists were expecting a risk-free rally to new highs. Just one month later, everything has changed. Between the Iran conflict, Corona Virus, impeachment and the upcoming elections, there is simply no escaping macro and political events if you’re an investor, regardless of what asset class you focus on.

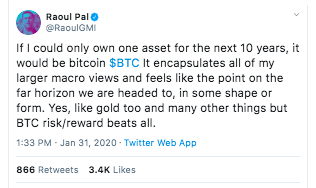

Prominent global macro investor, Raoul Pal, recently made his feelings public:

I predict a lot more prominent investors will be publicly singing the same tune, soon.

Will the Government Allow Bitcoin Digital Assets to Succeed?

US Marshals are about to auction off almost $40 million of seized Bitcoin digital assets. When was the last time US Marshals auctioned off seized cocaine or other contraband? They don’t, because it is illegal.

We often hear from crypto naysayers that “The US Government will never allow Bitcoin to succeed.” We’re quite certain the US Government would not auction off an item that they plan to shut down. We believe that this excuse for not having a digital asset strategy has now become invalidated. There are plenty of reasons to be cautious about a new asset class, but as each fear becomes invalidated, it means there is an increasing number of reasons to educate yourself further. Even the most religious people have acknowledged evolution happened.

In this case, the US Treasury has declared that it wants US Dollars. Buyers of the auction clearly prefer owning Bitcoin. It’s a free, healthy, functioning market.

Is Betting on a Political Outcome Investing or Gambling?

In 2016, every personal investor and professional portfolio manager had a view on the outcome of the Presidential election. These views, naturally, seeped into their portfolios.

If Hillary Clinton won, there were certain sectors and stocks that would benefit most, like Defense and renewable energy. If Trump won, you needed to own coal stocks and gun manufacturers. There are even baskets of stocks offered via ETFs from Motif Investing that specifically tailor the portfolio to these specific outcomes.

No one bats an eye when portfolio construction is shifted to match political outcomes. But elections are binary events -- there is a winner, and a loser. While event-driven investors are used to binary outcomes, and calculate the risk and reward via scenario analyses based on probability-weighted outcomes, most investors are not running models around the election. By making political bets, they are flat out gambling, albeit in a legal yet inefficient format. The only difference between this and a straight binary “winner take all” bet is that the loser will probably only lose 5-10% while the winner may make slightly more.

Most successful investors will tell you that identifying an investment idea, or a theme, is not the hardest part. The real challenge is finding the most pure-play way to express that view. For example, if the Coronavirus threatens global travel, what would you sell/short? Would it be travel sites like Expedia (EXPE), hotel chains like Marriott (MAR), theme parks like Disney (DIS), or niche travel locations (Vegas / Macau) like MGM Mirage (MGM)? The problem is, all of these large conglomerates have other aspects of their businesses that help shield them from a travel recession. Isolating the actual view is quite difficult using the traditional stock/bond/FX/commodities playbook.

So if an investor has done their political homework and believes with high certainty who will win an election, why shouldn’t they have a pure-play way to express that view instead of beating around the bush investing in stocks and bonds that may or may not benefit/suffer? Is it better to invest 100% of your portfolio in an outcome that may yield 5% if you’re right, or bet 5% of your portfolio in an outcome that will yield 100% if you’re right?

An up and coming crypto exchange, FTX, has made this reality possible via a Trump 2020 binary futures product. If Trump wins, this product expires at $1.00. If Trump loses, the contract expires at $0. The price will fluctuate from now until November 2020 based on the probability of Trump’s re-election (currently trading around $0.61 indicating a 61% chance). Not surprisingly, after initial feedback and flows were positive, FTX announced a Bernie, Bloomberg, Warren and Biden contract as well.

Are these President tokens gambling or investing? You could ask the same question when an investor buys a weekly S&P put option that will likely expire worthless -- is that gambling or hedging? Truthfully, it doesn’t matter what it is called...what matters is how an investor utilizes it according to their own risk management principles and individual mandate. The crypto markets are innovating, and blurring lines every day. Via blockchain, investments can now also be payments. Venture Capital can now be liquid. And maybe speculative investing should also contain some gambling.

It’s hard to develop a strong view, but once you do have one, it’s nice to be able to express it cleanly.

Transparency and the SEC

SEC Commissioner Hester Peirce formally proposed a 3-year safe harbor for digital asset projects that are afraid or unwilling to enter U.S. markets due to current securities laws. Read more about Arca's views on the safe harbor framework from Arca Chief Legal Officer and securities lawyer, Phil Liu.

From an investing perspective, the irony is that “The mission of the U.S. Securities and Exchange Commission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.” But by making it difficult for crypto projects to issue tokens to U.S. investors and forcing those who do to hide in jurisdictional shadows, they are actually hurting more investors than they are helping. Most companies utilizing digital tokens want to be transparent with investors, but they can’t because as soon as they do anything that caters to investors, they know they are violating securities laws. Meanwhile, investors can’t do proper due diligence if the companies / projects they are investing in are not able to disgorge timely and relevant information. If companies choose to follow the law and register through proper channels, not only is the upfront cost enormous, but most crypto exchanges won’t allow these tokens to trade on their platforms since they have been unable to obtain broker-dealer licenses.

So the quagmire is as follows: Either issue your token and become a security and then no one can trade it, or you pretend your token is not a security and give out no information. It’s a lose-lose for token issuers and investors.

While this is just the first step in what will likely be a lengthy process, it is still a very good sign for the industry. It is time for digital assets to permeate one of the biggest markets in the world without being fearful of the government's intervention. This should breed more development and growth in the market as a whole. Fortunately there are a few people out there like Commissioner Peirce who understand this, and there are companies out there like Messari who have been preaching transparency for years.

Arca fully supports this initiative.

Notable Movers and Shakers

Once again, Bitcoin’s share of total crypto market cap declined last week (-2.5%), marking its seventh straight declining week. While this is not the sharpest decline in dominance, it has now become the longest period of decline (the last being Sept ‘ 19-Oct ‘19 of six consecutive weeks). This metric, while noteworthy, does not point to the decline in Bitcoin as the leader of the pack: instead, it points to the growing asset class surrounding it, with an ever increasing number of investable assets. As for this week, there were a few that stood out to us:

- Decentraland (MANA), hailed as the “first ever blockchain-based virtual world”, announced a few weeks ago that its product is officially going live on February 20th. At this point, according to the team, “no single agent will have the power to modify the rules of the software, curate LAND content, modify the economics of MANA, upgrade the LAND smart contract unilaterally, or prevent others from accessing the world, among other decentralization features”. With the launch date coming up, interest has been reignited, with MANA finishing the week up 77%.

- Hedera Hashgraph (HBAR) announced a strategic partnership with Armanino LLP, allowing the Hedera ecosystem participants to leverage Armanino’s DLT assurance technology platform (TrustExplorer), as well as their new Trusted Node data service. The market took this news well - indeed this is the first noteworthy news from HBAR in quite some time - finishing up 51%.

- OKB, the utility token utilized by digital asset exchange OKEx, finished the week up 35% following a press release from the team announcing integration with three new wallets, as well as an expanded list of trading channels for the token. OKEx is a behemoth in the digital assets exchange market, capturing a lion’s share of volume in both spot and derivative markets. The growth of their token is indicative of the overall growth of their market reach. It remains important to track exchange tokens as a litmus for overall market sentiment.

What We’re Reading this Week

Blockchain firm ConsenSys last week announced its purchase of broker-dealer Heritage Financial Systems. In addition, the firm outlined how it would be restructuring the firm, splitting its software development arm from its venture arm and cutting 14% of its staff. The purchase of Heritage is part of an initiative to tokenize the municipal bonds, an asset class that is ripe for tokenization since munis are difficult to trade and transparency is sub-par. As efforts to further push Security Token Offerings (STOs) mainstream, this might be one venture that could succeed.

In a statement last week from Federal Reserve Governor Lael Brainard, the Federal Reserve is apparently researching and experimenting with distributed ledger technology to determine if a digital currency or central bank digital currency (CBDC) would make sense. Brainard did note, however, that the benefits of implementing a CBDC must outweigh the costs and potential economic impacts. This recent stance is a reversal from over a year ago when Brainard stated that "there is no compelling demonstrated need for a Fed-issued digital currency.” The Fed’s new stance is driven by the threat of private sector initiatives like Libra and from other foreign governments such as China.

Last week, Mastercard’s CEO Ajay Banga, revealed in an interview why the payments behemoth pulled out of the Libra Association months after launch. Banga cited that the revenue model for the project was unclear and there were questions around data integrity and how customer information would be handled. Finally, the project had originally been pitched as a financial inclusion project but once the idea of Calibra (the Facebook digital wallet for Libra) was introduced, it raised serious red flags. After launching last summer with 28 firms in its association, Libra currently only has 8 remaining as most have abandoned the project.

The US Food Safety and Inspection Services (FSIS) has contracted IBM to build proof-of-concept blockchain to track food export systems. A main responsibility of the FSIS is to track imports and exports of food items and ensure they meet certain standards. The current process requires manual tracking of documents, stamps, and shipping containers which the FSIS believes would benefit greatly from immutability and transparency across the supply chain. For many years blockchain has been hailed for its abilities to revolutionize areas such as supply chain management, and we now might finally start to see that in action.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)