What happened this week in the Crypto markets?

The Shift to Digital Assets

Let’s be honest -- if you're taking the time to read a crypto market recap after watching traditional asset classes fall like a stone last week, you should be invested in digital assets. You’re curious for a reason… a very good reason.

Let’s start with the obvious… very little was safe last week, including digital assets:

- US equities: -12%

- VIX: +250%

- Oil: -16%

- Bitcoin: -14%

- Gold: -6%

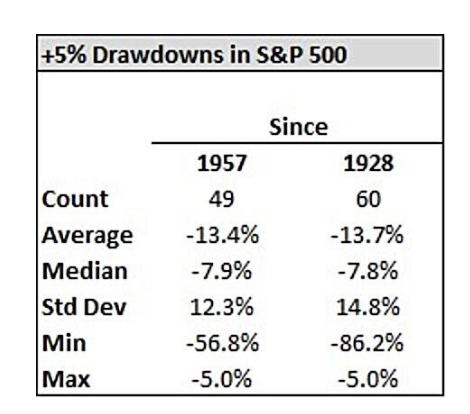

These are frightening losses, but not because of the magnitude or speed of the declines. In fact, our friends at Digital Asset Research (DAR) quantified this:

“Statistically speaking, since the inception of the S&P 500 in 1957, there have been 49 drawdowns of 5% or more. Replicating the index back to 1928, there have been 60 drawdowns of 5% or more.”

We’ve seen moves like this before, and we’ll most certainly see them again. But they are scary not because of severity, but because of trust (or lack thereof). Global markets rallied for 10+ years on trust that central bankers and governments were there when we needed them, and even there when we clearly didn’t (why did we cut 75 bps last year?). Now global markets are selling off due to mistrust of governments. When the repo market breaks down, and when an infectious virus sweeps the world, how do you really know what risks lie beneath?

Of course, by the time you read this, it’s possible governments around the world have already responded, though not necessarily by choice. Equities and Treasuries are now telling the Fed what to do. This is why the markets today are so terrifying. "Surprise" central bank actions are no longer surprises; they are expected. In fact, they are outright demanded.

This is the definition of Moral Hazard.

- If CBs don't act, markets will implode simply because expectations aren't met.

- If CBs do act, bubbles will continue to blow until the next black swan reminds us that risk still exists.

This lack of trust combined with blind faith actually strengthens the already strong crypto narrative. While a black swan event is causing global damage, COVID-19 began as an entirely regionalized event in terms of health risks and subsequent lost production in certain affected areas. Individual plants closed, public stores/events shuttered, conferences were cancelled, and local communities (churches, schools, businesses) were put on lockdown. This is a great reminder for why decentralization is so important. Removing key points of failure (both individuals and geographies) is a central tenet of the digital asset revolution.

In the end, COVID-19 will likely come and go without wiping out humanity. But this wake-up call may accelerate the shift towards the digital medium at the expense of the physical medium (see the price of Zoom Video Communications stock as an example).

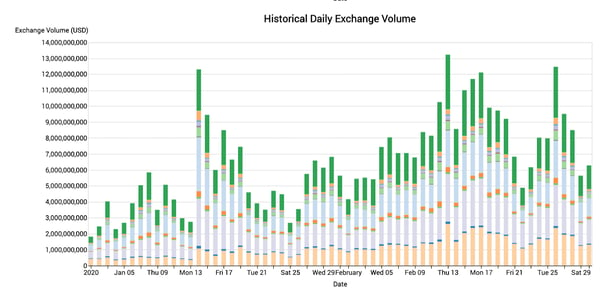

Crypto Volatility Remains Muted

Despite the large declines in crypto prices last week, crypto volatility was actually a fairly amazingly muted and controlled price correction. Prices were lower, but:

- Crypto volumes remained strong

- Futures liquidations were moderate, indicating leverage was being unwound slowly

- Crypto vol barely budged (currently at 9 month lows), even though spot prices fell 20% from the highs and the VIX exploded. BTC Implied Volatility simply is not being priced consistently with “Macro Volatility” and is significantly underpriced, making this a great environment for buying spot vs buying puts.

- Calls remain better bid than puts (negative skew)

Crypto Volumes Remained Strong (Spot Exchange Volumes YTD)

Source: Digital Asset Data

Bitcoin Volatility has Barely Budged

.png?width=1064&name=pasted%20image%200%20(6).png)

There just wasn’t a real “panic” at all. One could argue that crypto is officially operating completely outside of the traditional markets, which is definitely long term bullish regardless of near term price action.

Lowering Guidance --- Umm, So?

Here's the problem. Earnings growth was ~0% last year too, and stocks still rose 29%. The PEG chart below illustrates the stock market growth in 2019 based on literally nothing.

Regardless of whether or not stocks are overvalued (they are), we point this out because a common excuse investors use for why they have not yet allocated to digital assets is that "crypto lacks fundamentals."

First, that is wrong. Some digital assets have no fundamentals, but many others can be modeled using revenue or free cash flow, while others can be valued using newer techniques like Metcalf's law (which incidentally is the same model that was used to value Netflix, Facebook, Uber and other new technologies pre-revenue).

Second, the fact that the equity and corporate debt markets are reacting to "declining fundamentals" this year, but were immune last year, shows that markets trade on narratives more than fundamentals anyway. As we argued last year, what difference does it make if there is "Intrinsic value" underneath a stock or a bond if the market is trading 5-10x above intrinsic value anyway? That's quite a lot of risk premium above intrinsic value that is supposedly "protecting" you.

Cantor Fitzgerald wrote this a few weeks ago (before the meltdown):

"It's not our first rodeo. We've seen markets trade on sentiment and momentum well beyond fundamentals on more than one occasion. This instance reminds us most of 1999. We pointed to the action in Virgin Galactic. It made us wonder how many other no revenue or cash flow negative companies with over a billion in market cap existed. Well, it's over 200 based on our screen using Bloomberg data. While a number of those are biotech pipe dreams (pun intended) others look and feel much more like companies we saw in 1999 or during other periods of speculation. As much as it pains us, our initial concession (in our Outlook) for a rally to 3,300 just wasn't enough and, who knows, perhaps a melt up to 3,500 is in the cards. Let's be clear. There's sometimes no fundamental reason for it. It just is based on perception - a perception based on narratives that run only an inch deep. Based on data we’ve seen, much of the speculative activity in tech (of the above variety) is retail driven. Let's see how much longer it persists. This kind of activity often unwinds much faster than the wind up.

Congrats to Cantor for sticking with their call, and finally being validated. Everything in investing stems from a narrative. The narrative right now is that equity valuations are incredibly stretched relative to fundamentals, propped up by share buybacks and cheap money. Meanwhile, the narrative on digital assets is that this is the future of finance and banking. It wouldn’t be advised to stay fully invested in equities when the narrative is shifting, in the same way that it wouldn’t be advised to fully dismiss a technological and societal revolution simply because you haven't figured out exactly how to value each digital asset. Thousands of analysts from academia and Wall Street (including those at Arca) are working on developing these valuations techniques.

But remember, agreed upon valuations typically come AFTER narratives are already built.

Is the Bitcoin “Safe Haven” Narrative dead?

We don’t believe so. Despite this past week’s large declines, Bitcoin can still be a hedge to the risks in the financial system. Again, from DAR:

The saying “Bitcoin for safety” evokes strong imagery for those of certain viewpoints - safety from central banks, profligate governments, inept politicians, currency debasement, greedy bankers, and anything else presently bothersome. For many others, however, like financial institutions, institutional investors, and asset allocators, the matter is more practical than philosophical. While Bitcoin is presently pitched by many as “digital gold” for features like its fixed supply cap and declining supply growth rate, the question remained unanswered as to how Bitcoin behaved in real world "risk off" scenarios. The conclusions from our analysis are concise, but multifaceted. On multiday stock market drawdowns, Bitcoin exhibits slight daily positive returns, but ones that are well below normal average daily returns. Bitcoin only works as a hedge (generates positive returns) 54% of the time, while US Treasuries work 85% of the time, and gold works 69% of the time.

It’s clear Bitcoin is a hedge of some sort, over some time frame, without being a perfectly negatively correlated "flight to quality” asset. Its safe-have status may be defined in decades relative to the loss of purchasing power overtime, not in seconds via trading algos. More importantly, over longer-time frames, digital assets remain completely uncorrelated to all other asset classes. We don’t judge Gold over daily or weekly time frames, and we’d be wise not to measure Bitcoin that way either.

.png?width=512&name=unnamed%20(13).png)

Notable Movers and Shakers

Bitcoin Dominance finally posted a green week, stopping the skid just shy of double-digit weeks (9). Last week was a flushout across the board, with Bitcoin showing much better downside performance (-15%) than the rest of the market (-20%) . There wasn’t much in terms of notable movers, but the following are worth mentioning:

- Kyber Network (KNC), which was discussed in this section last week, was among the top performers following their listing on Coinbase Pro (and Coinbase a few days later). Exchange listings have been a catalyst for quite some time in this market, especially with the regulatory clamps placed on U.S. customers as of late. The listing propelled KNC to a +33% finish on the week, which marked its 7th consecutive positive week.

- Bitcoin (BTC) hash rate just posted an all-time high of 1.38E+20 hashes/second (138 EH), with the previous high occuring on January 17th, 2020. With the Bitcoin Halving around the corner (70 days!), it will be interesting to monitor how hash rate and price interact. The current metrics suggest that miners are net bullish into the halving, as hash rate has not dropped off thus far in anticipation of the block reward halving in May. It is worth noting that in 2016 (the last halving, July 9th), hash rate fell momentarily for a few weeks before picking back up and creating new all-time highs. Game theory is still largely at play with this next halving (as this is only the third time it will have happened), but the net trend doesn’t lie: the energy to secure the Bitcoin network has been on the up and up since the Genesis block, and doesn’t look to slow down any time soon.

What We’re Reading this Week

According to Square’s Q4 earnings report, the payment app sold $178m worth of Bitcoin in Q4 bringing its total sold to purchases to $516m for 2019. Although the volumes on Square are dwarfed by larger exchanges like Coinbase and Binance, the app has seen 20%+ quarter-over-quarter growth. Bitcoin is offered on the app alongside the ability to purchase fractionalized tech shares in a bid to broaden financial access. The uptick in Bitcoin purchases is a positive sign of the growing interest in gaining exposure to Bitcoin and digital assets as an asset class.

According to insider reports, research into the implementation and distribution of DCEP, China’s Central Bank Digital Currency, could be slowed due to the Coronavirus outbreak. The outbreak has caused delays in workers going back to the office at institutions such as the PBOC. A potential benefit of DCEP could be that it reduces contact between individuals - a much needed benefit in a time when banknotes from hospitals, wet markets, and buses are being burned in an effort to combat the spread of the virus. Despite the delays, insiders say the launch should go on as scheduled simply due to the amount of manpower the Chinese government is dedicating to the project.

In an unsurprising move last week, the SEC rejected Wilshire Phoenix’s application for a Bitcoin ETF. After a string of rejections of other ETF applications, Wilshire had hoped that its ETF would be approved as it invested in both US Treasury bonds and Bitcoin and would rebalance depending on the volatility in the price of Bitcoin. The SEC’s rejection is based on the grounds that they did not feel the Bitcoin market was resistant to manipulation, an argument it has made to reject the prior ETF applications.

According to the submitted US government budget, U.S. agencies are requesting millions in additional funding to hire those with crypto and blockchain expertise to help oversee various initiatives. The agencies requesting this budget are no surprise - the IRS, FBI and CFTC - but it seems that these groups now desire to bring talent in-house. It is uncertain if the budget requests will ultimately be approved, but this is yet another sign that the US government is realizing the importance and permanence of digital assets and blockchain technology.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

.png?width=512&name=unnamed%20(12).png)

.png?width=600&name=pasted%20image%200%20(7).png)

.png?width=600&name=pasted%20image%200%20(8).png)