What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

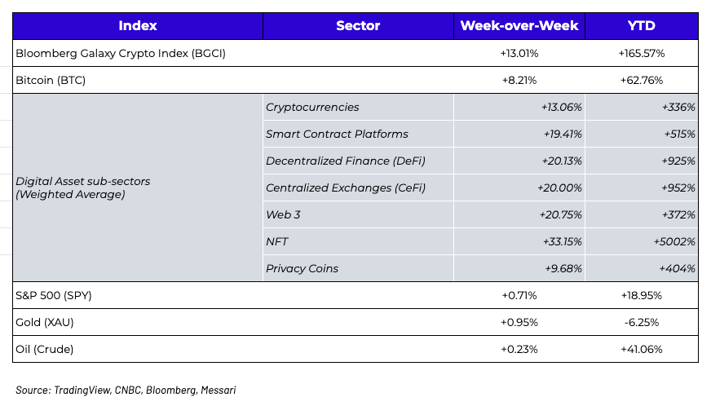

Week-over-Week Price Changes (as of Sunday, 8/15/21)

Four Straight Weeks of Gains

Looking at the table above, it’s almost laughable in retrospect that anyone was calling for a prolonged bear market just because we had a few weeks of (albeit violent) price declines. The digital assets market has now rattled off four consecutive weeks of double-digit gains. In the past few months, we’ve discussed numerous positive factors that have contributed to the fast recovery of the digital assets market:

Despite already diving deep into so many topics, the evolution of this asset class continues to move faster than we can write about it each week. There is so much activity in this space currently that discussing a single topic would be an injustice. So instead, we’ll give you eleven random thoughts that are on our minds heading into the home stretch of the year.

Eleven Random Thoughts Driving the Digital Assets Market

#1 Axie Infinity and OpenSea Are Driving Ethereum Fee burns

Following the recently implemented EIP-1559 upgrade, over 50k ETH has already been burned (~$150mm). Despite all of the talk about DeFi, it’s actually NFTs and Gaming that are driving the bulk of the Ethereum activity currently. The largest NFT marketplace (OpenSea) is the biggest contributor to the fee burn, followed by the Axie Infinity game at #3. DeFi is still a big driver, with the largest Decentralized Exchange, Uniswap, coming at #2, but suffice to say, Ethereum has a lot of diverse activity happening on its platform -- none of which existed the last time ETH hit all-time highs in 2017. Said another way, activity on Ethereum has been booming for years, but now we have a real scoreboard worth paying attention to in the form of ETH burns.

#2 We may actually have real competitors to Ethereum -- enter Solana and Terra

While Ethereum still dominates, it was a big week for Solana, which surpassed an all-time high of $1.8 billion in total value locked across the protocol. More than 10k people waited for an NFT project on Friday night which sold out in 8 minutes, and Mango Markets completed a $70mm raise last week. Meanwhile, Terra has almost 3x more TVL than Solana, and utilizes the inflation of its staking token (LUNA) to collateralize a set of algo stablecoins, which increase its utility as more enter circulation. While most casual digital asset market observers have heard of legacy Layer 1 protocols like EOS and Cardano, it's the new batch of Layer 1s that are attracting real economic activity and application growth. The native tokens, Solana (SOL) and Terra (LUNA), trade at 5% and 3% of Ethereum’s (ETH) market value, respectively, so by no means are these networks operating on the same scale yet. But probability-weighted, these are likely the first blockchain’s that have actually earned their market values.

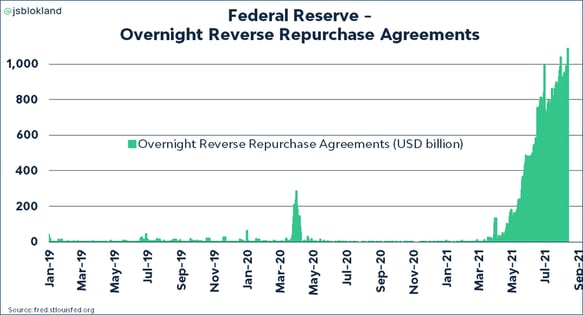

#3 The rally ain’t over if $1 trillion is being parked in reverse repo

It’s fascinating to watch the rationales for why equity prices and digital asset prices are doomed, even while the prices of both keep accelerating and there is simply nowhere else to park your money. The amount of cash parked at the Fed’s reverse repo facility hit a new record last week of $1.087 trillion. As our friends at Cliffwater pointed out, “while money-market funds are flocking to the Federal Reserve’s overnight reverse repurchase agreement facility for the yield, large U.S. banks are using the program to shed unwanted deposits. The facility serves as an investment option of last resort to mop up excess cash, especially with short-term funding rates hovering around zero. Analysts say demand for the Fed’s reverse repo facility could keep rising as reserves remain elevated. Usage of the program could top $2 trillion by the end of the year.” The U.S. equity market just wrapped up one of the best earnings quarters on record, with 87% of companies in the S&P 500 beating 2Q estimates, while the digital assets market is growing in many areas 30-50% Q-o-Q in volumes/users/revenues and other KPIs. It’s quite difficult to see this reversing any time soon with so much wealth sitting on the sidelines.

#4 On-Chain, real-time, blockchain-based data is awesome

We’ll be diving deeper into transparency in a future “That’s Our Two Satoshis”, but what we’re seeing in terms of real-time data analytics is nothing short of spectacular. Our friends at Multicoin Capital wrote a great blog following their recent investment into Dune Analytics, an all-in-one destination to query, visualize, share, and explore smart contract data from public blockchains. We cite data from Dune Analytics constantly, but also from Token Terminal, the Block, Bybt, Glassnode, Skew, Etherscan and many other great data providers. But it’s not just the data aggregators who are making our jobs as analysts easy -- the companies and projects themselves are making it easier than ever by providing real-time dashboards of their financials:

The future of finance is not quarterly reports with stale sell-side research and a reporting lag. The future of finance is real-time reporting and transparency, and we’re seeing the beginning of the end of traditional financial reporting.

#5 Decentralized M&A is going to be interesting

Polygon acquired Hermez Network, a zk-Rollup scaling solution platform, and Polygon is financing this transaction by buying out HEZ tokens with MATIC tokens at a 3.5:1 rate. This will utilize around $250 million, or 2.5% of Polygon's treasury. These are not companies -- these are decentralized networks, yet the financing looks and feels very much like an equity-financed acquisition. Quick merger math -- HEZ ran higher after the news to the exact merger conversion price. Even without dedicated merger-arb funds, we’re beginning to see efficiency of digital assets. More importantly, one of the trickier parts of using discounted cash flow analysis to value digital assets is the terminal value. If M&A picks up, that is no longer an issue.

.png?width=423&name=image%20(41).png)

#6 Follow the data to gauge investor interest

There are a lot of ways to track investor interest in digital assets. CoinShares releases weekly fund flows, Preqin shows the growth in digital asset hedge funds, and there are countless investor surveys detailing institutional interest. But perhaps the most interesting way to track investor interest is to watch the accelerated interest in data collection. Excel-plugin API aggregator, Cryptosheets, pulls in data to excel from pretty much any data provider. Cryptosheets founder, Chris Ware, recently told Arca that he’s seeing legacy customers upgrade their subscriptions, and is spending a lot of time filling out due diligence forms and speaking with compliance teams from large traditional funds, trading desks, and other large Wall Street firms. The interest is greater than the last 2 cycles combined, with sign ups in the past 14 days alone up 500% over the trailing 30-day averages. Larger institutions aren’t going to invest in this asset class without being able to quantitatively measure it, and data collection is the first step. The recent large private financing rounds from Dune analytics and Messari show further evidence in Wall Street’s interest in data.

#7 Tether gave naysayers and supporters what they wanted

The WSJ had a fascinating article about confirmation bias this weekend. In short, whether its gold bugs, bond vigilantes, or Amazon detractors… some will simply latch onto an idea and stick with it no matter what evidence is presented. With that in mind, controversial stablecoin issuer, Tether, released its second quarterly attestation report, and there was something for everyone in there. Tether attests that they hold about $14.5 billion of grade A-1, $14.0 billion of A-2 and $1.7 billion of A-3 commercial paper. Supporters will highlight the improved transparency over the first report three months ago, which now includes a breakdown of underlying assets including commercial paper holdings by rating, and duration. Naysayers will continue to say “Tether is hiding something” by not providing exact holdings reports (even though this level of detail now equals or surpasses the level of detail provided by Paxos and Circle for their stablecoins). As we discussed a few weeks ago, shorting USDT is a great trade on paper that almost assuredly will not work.

#8 The Washington / Congress / Digital Assets showdown was a huge step in the right direction

The infrastructure bill passed the Senate with the initial very vague digital assets language, and is on its way to the House. The House can make adjustments and reconcile with the Senate, so nothing is final. Either way, Senator Portman was clear in the intention of the language, as was Treasury, so the implementation of the end language has almost no chance to be the draconian descriptions that were originally reported.

The developments over the past week were incredibly positive. The digital assets industry is now firmly on the radar of Congress, which means they are starting to dig deeper, and educate themselves beyond the tired narratives of energy efficiency and ransomware payments. It is also one of the only issues that transcends partisanship... Ted Cruz came out in support of a Ron Wyden amendment! Ultimately, U.S. regulators want sensible protections in place that foster innovation and growth. In order for real institutional investment, we need to see regulatory clarity, and this is the first step.

The other positive was the mobilization of the community and lobbying efforts. It was grassroots, and it took everyone by surprise. Yes, there was hyperbole, as there always is in politics and lobbying, but this can serve as a catalyst to strengthen the lobbying efforts in DC. It also served as the catalyst to make politicians aware that they have constituents who care deeply about the asset class, and it is totally non-partisan.

We’ve been dealing with regulatory overhang in digital assets for years, and the question we hear more than anything else is “What about regulation?” While we wait, investors already in this space are not going to be overly cautious based on unenforceable and unactionable political headlines until we get some actual regulation.

#9 Great summary of the BTC vs ETH debate

We wrote a few weeks ago that “Bitcoin is a great asset, but it's no longer representative of the asset class as other sectors are leading the way forward”. Naturally and expectedly, we received a lot of feedback from the digital assets community, who often feel the need to take a mutually exclusive stand on “Bitcoin or everything else”. Perhaps the most balanced response we received came from Dave Weisberger, the CEO of CoinRoutes, who tweeted:

“The dichotomy between Bitcoin and all the fundamental analysis you highlight can be summarized thusly: Bitcoin aspires to be the DENOMINATOR by which ALL assets are measured. NFTs, DeFi & the tech that enable them will be the NUMERATOR of the digital economy. As such, it is absurd for Bitcoiners to dismiss everything going on in the world of DeFi or with NFTs, OR for others to ignore the role of a store-of-value with a fixed supply, and no direct connection to a particular network in the evolving digital economy.”

#10 We need investment bankers, and the Olympics needs a token

Miami is set to launch its own digital asset, but this sounds pretty poorly designed on its surface. In our view, a public city token should be purchased to fund development of certain community projects, and then if you own the token, you’d receive discounts whenever you use publicly funded projects — trains, parks, buses -- and/or you’d get priority (show proof of tokens, get access to certain parts of the park or something). Regardless, the rushed nature shows why we need investment bankers in this space. Every single company, municipality, and project should have a token in its capital structure, but in order for this to happen, we need real advisors who are experts at designing tokens and finding investors.

For example, why doesn’t the Olympics have a token yet? From Axios:

“The Olympics haven't made financial sense in decades. Host cities spend billions, inevitably going deep into debt, with a lasting legacy of little more than venues ill-suited to any other use. The 2008 Beijing Olympics cost $45 billion; its revenues were $3.6 billion, most of which went to the IOC. The 2014 Sochi Winter Olympics came in closer to $50 billion, with much lower revenues. The Tokyo Olympics will cost about $28 billion. The decision to ban spectators means foregoing another $1 billion in ticket sales, not to mention whatever amorphous boost Tokyo might have received to its reputation as a tourist destination. Broadcast rights constitute the lion's share of Olympic revenues, and the IOC has sensibly locked in a multi-billion-dollar revenue stream from Comcast through 2032, when Brisbane, Australia, will host the Games because there were no other bidders. U.S. television rights are more valuable than those of every other country combined. But five years ago, the Rio Olympics — in a perfect time zone for the U.S. market — had very disappointing ratings. The Tokyo Olympics, without a live audience and in a terrible time zone for American viewing, will struggle to do any better.

What if the IOC sold tokens to the fans of athletes, who then receive a cut of future sponsorship rights? Or perhaps tokenholders get 100% of TV revenues. Certainly, someone must be thinking of ways to link fan engagement with profits, much like what Chiliz / Socios is currently doing across the globe by issuing “Fan Tokens”.

#11 Coinbase crushed 2Q earnings, and Wall Street just doesn’t get it

This is fun -- why stop at 10? Arca was more bullish than just about every sell-side analyst on Coinbase’s 2Q earnings, which came out last week and absolutely crushed all estimates, including our own. The company did $2 bn in revenue, with EBITDA margins over 50%. These numbers absolutely dwarf other traditional “exchanges” like NYSE/ICE, CME, Nasdaq and CBOE, yet the stock barely budged (or rather it rose 10%, but then fell right back down). For some reason, consensus estimates for the remainder of the year still have revenue declining by 10% YoY. That is an absolutely wild conclusion by sell-side analysts for a company growing this fast, and quite frankly we can’t figure out what variables Wall Street is adjusting to reach that conclusion. Just about every digital-asset native investor that we speak to disagrees tremendously with the conclusions of Wall Street’s analysts. So how is this happening?First, Wall Street can’t figure out which sector/coverage group should focus on digital assets. Should it be the Banks/Brokerage group or the FinTech group, or maybe a new group altogether? Second, Wall Street continues to dismiss, ignore or flat-out remain ignorant to the growth of digital assets beyond Bitcoin and Ethereum. Third, there continues to be skepticism from the incumbents who are quite possibly being disintermediated by this new industry. In our opinion, Coinbase will likely look a lot like Facebook in 2011. FB stock got crushed following its IPO, and Wall Street couldn’t figure out how to cover social media, and completely mistrusted management. It took 3-6 months for FB to claw its way back as the Street continued to misread the growth trajectory of the company, including the drivers of success and the sustainability of the revenue model. But FB then spent the next 10 years going straight up as the revenue growth never stopped.

.png?width=1600&name=pasted%20image%200%20(22).png)

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Junior Portfolio Manager - Special Situations Analyst

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

Andew Stein, VP of Research

Kyle Doane- Trader Operations Associate

Matt Hepler- VP, Portfolio Manager

Nick Hotz- Sr. Global Macro Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency