What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

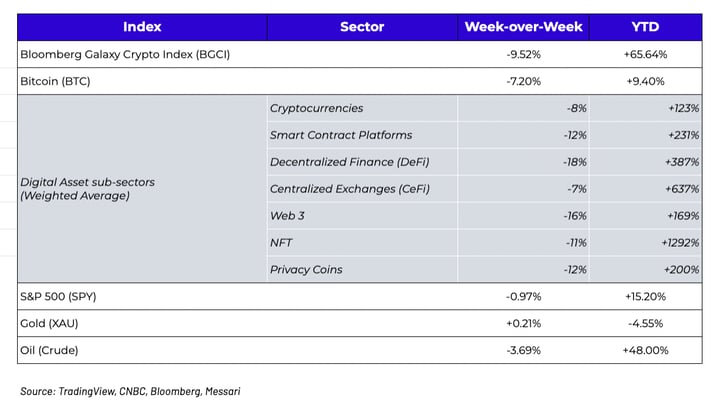

Week-over-Week Price Changes (as of Sunday, 7/18/21)

Hedge Funds Shorting Tether is a Great Trade -- that Most Likely Won’t Work

The U.S. data continues to be in focus, with CPI, PPI, Univ of Michigan, retail sales and jobless claims numbers all exceeding expectations. So naturally, risk assets had a rough week and Treasuries rallied. After reaching new all-time highs earlier in the week, the S&P 500 (-1.0%), Nasdaq (-1.9%), and Russell 2000 (-5.1%) all finished the week lower following another higher CPI print, as the market turned generally defensive. The Russell 2000 fell for its fourth week in a row, which looks similar to the constant selling pressure we’re seeing in digital assets and “crypto stock” counterparts. That said, a quick look at the table above shows you all you need to know. Gold is still down YTD, BTC is marginally higher YTD, yet all other risk assets (commodities, stocks, and digital assets) are still having a great year (despite what journalists will try to tell you).

But with the 10-year Treasury almost back to YTD highs (low yields), and the Fed doing its best song-and-dance to indicate no changes are on the horizon, markets still need real negative catalysts to force real money to leave risk assets. With digital assets specifically, we’ve discussed why we think this “bear market” is nonsense and will be short-lived, but if we’re wrong, it’ll probably be due to us being wrong about Tether -- everyone’s favorite “negative catalyst on the horizon.”

For those who have been following Tether and digital assets for years, there is literally nothing new to discuss. The next three paragraphs could have been written 3 months ago or 3 years ago (and in fact we did write most of this 3 months ago, and 3 years ago). The only new part of this story is how large USDT has become ($64 bn), and how many new people are now aware of Tether and feel the need to voice their own strong and uninformed opinions. We get more questions about Tether than any single topic. From the completely nebulous, to well-informed but inconclusive, to straight facts from the source itself… it seems this Tether saga will never end unless Tether’s USDT stablecoin completely unravels, or it ends up being the world’s reserve currency. So here’s yet another Tether hot take.

I think Tether is the biggest (and only) systemic risk to the digital assets ecosystem. It is simply too large, and too heavily utilized on exchanges and in DeFi for it not to cause major hiccups and ripple effects should USDT lose its peg and cause a run on the bank. That said, there are perfect substitutes for all stablecoins, and all exchanges, so none of these issues would be long-term. That’s actually the beauty of a truly global asset class with little to no barriers to entry. It’s flat out impossible for one problem in one part of the world to be a death blow -- which is why I think there are so few (if any) systemic issues, and also why recent events out of China will have short-lived impacts as well. But short-term, if you’re looking for a real negative catalyst… if USDT lost its peg, it would cause major short-term structural issues given how much of exchange trading, loan collateral, and decentralized finance relies on Tether.

But I'd also put a high probability on the fact that Tether is fully backed by enough real, safe, and liquid assets that none of these problems will ever actually materialize. We speak to traders all day every day who redeem and create Tether constantly, in the billions of dollars, and have had no issues whatsoever transacting. Further, Tether's reserve report, while not as detailed as the market wanted, is not any different than the reserve makeup of banks and other financial institutions.

The difference now is that Wall Street seems to have caught wind of Tether. We are hearing that several macro and credit funds are trying to short USDT right now, and it's a smart trade even though it almost assuredly won't work. If you can short an asset at par, that may go to 20 cents on the dollar, and only costs you 5-10% per year in negative carry to borrow and short, you should do that trade all day long if you're a long/short manager or credit fund. Back at previous credit funds where I worked, we would short every short-duration subordinated bond that was callable at 1-2% yield-to-worsts, just in case for some reason the capital markets dried up and the bond wouldn’t be refinanced. About 99 out of 100 times this trade failed, but once in a while it worked (I recall shorting Kwiksilver 7.125% sub bonds once that ended up falling 30 pts or so after a refinancing deal fell through). It doesn't mean any of these were good trades, but the risk asymmetry was good -- very little downside to the short, and very high upside.

So the USDT short from non-digital asset native funds is low risk, and is a fun trade to put on if you just heard about Tether and think you’re onto something new. Unfortunately, you’re not. While everyone wants to play George Soros and break the Bank of England, actually making money doing this is nearly impossible and highly unlikely.

Sushiswap Governance (G) and Social (S) prowess is Flat-Out-Awesome

We’ve consistently looked beyond Bitcoin to the other more exciting sectors of digital assets, and the ESG discussion is no different. We even released a white paper talking about “GSE not ESG”, as it pertains to looking beyond Bitcoin’s environmental short-comings and towards the evolutionary advances in social responsibility and public governance using digital assets. This past week, Sushiswap gave us a real-time example of how powerful these concepts really are.

If you’re not familiar with Sushiswap (SUSHI), it’s the 2nd largest Decentralized Exchange (DEX), it has a fascinating and convoluted inception story, the token has over $1 billion in market cap, it trades publicly and actively on many exchanges, and generates hundreds of millions of dollars of revenues and dividends. Sushiswap is currently involved in the most active social and governance discussion in the young history of digital assets. If you have a few hours to spend, I highly recommend diving deep into this very public and transparent debate, but under the assumption that you don’t have that time, we’ll provide the cliff notes as well.

In short, Sushiswap is now in the envious position of having a bidding war over who gets to invest tens if not hundreds of millions of dollars in their project… a project run by a passionate group of young but tenacious developers, many of whom are volunteers. A few months ago, the lead developers tried to do a private round of financing (initially soft-marketed as an opportunistic $10-20mm raise), which eventually morphed into a potential $60mm PIPE at a 30% discount AFTER the token had already fallen 70% in line with the recent swift market selloff. The Sushiswap community, including Arca, voiced significant concern about how this deal was value destroying and unnecessary, and we offered a counterproposal which saves Sushiswap $22mm and reduces dilution. We are now headed to a significant comment period, multiple governance calls, and what we believe will ultimately resolve itself with a very strong solution that makes most (not everyone) happy and excited to keep working on this project and investing in it. But keep in mind, Sushiswap has no CEO or board of directors… it has a passionate, democratic group of SUSHI token holders who ultimately have to approve every major decision that the protocol makes, including how and when it sells more SUSHI tokens to the market.

We are witnessing an amazing debate happening in real-time, and in the public eye, about how valuable venture capital investors really are, and how or why they are still involved in projects after they already have publicly traded tokens with large market caps and liquid floats. Before we get into the details of the debate, let’s pause for a second to appreciate that we’re seeing the promise of a decentralized, more democratic financial system in play.

- On one hand, you have the strategic Venture Capital investors who are trying to do what they know best...offer their expertise in return for a super sweetheart discounted deal with liquidity lockups, in an effort to help grow this project to a point where they can exit profitably.

- On the other hand, you have Arca and many others who are saying “wait a minute, why would we gift wrap this to you if this is already publicly traded, it’s already a flourishing project, and the whole point of digital assets is to democratize ownership, equally distribute the equity-like returns, and grow this project with active participants rather than passive checks.” Worth noting, the SUSHI token jumped over 20% after Arca’s proposal was released.

- And on the… third hand… you have a passionate group of retail investors / customers / developers / stakeholders all trying to figure out how best to vote, while in some cases trying to understand a capital markets process that they have been largely left out of in the debt and equity markets for centuries.

We are in awesome and uncharted territory here, and regardless of how it ultimately concludes, and there are already a few takeaways:

- Venture capital firms are under siege to demonstrate their actual value and plans, not just read from a generic marketing deck. They are sitting on warchests of cash with limited opportunities to meaningfully deploy, but they have little experience with public markets and transparency, and may be burning the most important people (customers/retail) if they don’t quickly get on the same page.

- There is an insanely passionate group of people from all walks of life who are all trying to put money into, and ultimately help grow, a pretty amazing and profitable project.

- It’s demonstrating a real evolution from the old “corporate boardroom”, as the decisions are not made unilaterally by a small group of elites, but rather by a large group of heavily incentivized stakeholders who actually show up to vote and discuss. This is the first governance token that seems to actually care about governing, and has something worth governing.

There is a real gap in the market - what does a growth stage digital assets fund really look like? What does "adding value" from investors entail after you’ve already reached a massive scale? This industry is plagued by a fallacy that every investor is either a 5-minute candle trader ready to sell the second they make 5%, or a 7-year locked-up venture fund with a long-term exit strategy. The reality is, these are liquid public markets that should have long-term liquid investors, but because the mutual funds, traditional hedge funds, financial advisors and educated high net worth investors are not here yet, and because we have no investment bankers helping to guide these young projects, we have a very strange dynamic where Venture Capital firms are playing in a liquid sandbox with which they have no real expertise. How long will it take for the rest of Wall Street to stop talking about Bitcoin and start investing in the fastest-growing asset class, and the highest revenue-generating startups?

Whether Arca’s proposal is successful or not, the fact we have the ability to flag issues and create a counter-proposal is highlighting the truly democratic nature of decentralized projects. And ultimately, nothing is going to happen without the most important stakeholders having a say in the outcome.

Deep Dive resources:

What’s Driving Token Prices?

- Helium (HNT) -17% after its first full week post Validators consensus group upgrade which has resulted in material blockchain performance improvements with transaction rate, block time, and election time all showing better consistency since the upgrade. The network also announced a partnership for asset tracking coverage with one of the largest device manufacturers in Europe for a US launch. Taken together, the blockchain consistency and network’s growing scale should promote underlying network use which is the catalyst for a material appreciation in the token price.

- Thorchain (RUNE) -37% after an attacker exploited a bug in Bifrost (a defi protocol that connects to other PoS chains), essentially tricking the pool into thinking that 200 wrapped ETH had been deposited (many times into various pools) and then swapped for RUNE and other ERC-20 assets. In reality, no ETH was deposited and the pools were just distributing RUNE / ERC-20s thinking ETH was being swapped. This also had the impact of changing all the pool prices. 4000 ETH worth of ETH / ERC20 assets were taken ($8M) but attacker paid $1.4M in slip fees and an additional $1.4M in trade fees paid to LPS, whereas net loss was $5M. The loss was suffered by ETH - RUNE LPS (LPs) but will be covered from the Rune Treasury.

- Aave (AAVE) -16% after a governance proposal was put forth to add AXS as collateral on Aave. So far the proposal seems to have majority support within the governance forum. Aave was also listed on Binance.US.

- Chiliz (CHZ) -6% after holding two FTOs for $POR and $LEV (both sold out) and listed three new tokens that began secondary trading on the app ($UCH, $FOR, $LEG). Finally, Chiliz pulled an FTX and bought the naming rights to the Argentinian soccer league renaming it "Torneo Socios.com" for the upcoming 2021-22 season, which should raise awareness about Socios and Fan Tokens.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency