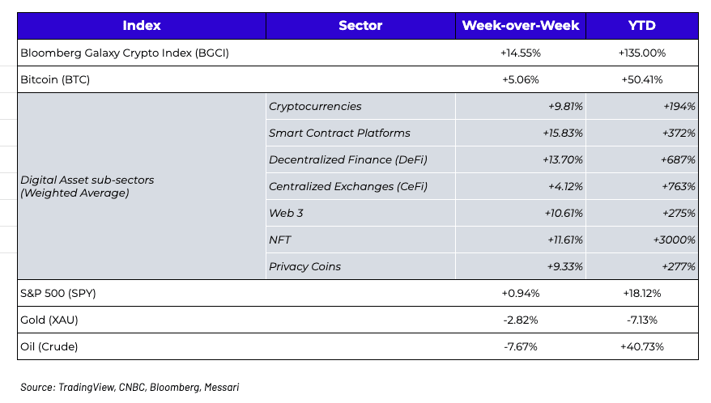

What happened this week in the Digital Assets market

Week-over-Week Price Changes (as of Sunday, 8/08/21)

Digital assets and crypto stocks caught fire last week, but only two topics mattered.

- The infrastructure bill in Washington, which included an amendment battle about a provision related to taxation of digital assets.

- Ethereum’s upgrade via the long-anticipated London hard fork, which included EIP-1559

To discuss these issues, we brought on Arca experts, Peter Hans and Nick Hotz

Digital Assets are on the Main Stage in Washington - What it means for regulation

Written by Arca Managing Director, Peter Hans, former director of research for a Washington policy research firm

For the first time in its relatively short history, digital assets got the full attention of Capitol Hill. While this process is new to digital assets, it’s not unique, though the past week did have some fairly unique and monumental developments. I’ve been tracking regulatory policy changes as catalysts in equity and debt markets since 2005, and this is the first time I’m seeing:

- This much grassroots opposition for a package. Digital assets advocates are generally aligned that there is a need to regulate the decentralized currency, but not by rushing to pin it to an infrastructure package with language they say is far too broad for this nuanced technology.

- A disconnect between what is actually being legislated and how these policies are realized in practice. This is due to a lack of understanding of digital assets by policymakers, and a lack of understanding of policy implementation by digital assets participants.

- A Democratic President aligning himself with a Republican-led amendment (Portman R-OH), while openly opposing a competing Democratic led amendment from the sitting Chair of the Senate Finance Committee (Wyden). Further evidence of this unusual situation, Ted Cruz, staunch Repulican, openly came out in support of the Wyden amendment (D-OR).

For those not glued to CSPAN over the past week, here’s what transpired:

- Democratic leadership was unable to use a pay-for that added incremental funding to the IRS, which is notoriously under-resourced. As opposed to raising taxes, Congress sought other pay-fors and viewed “taxing digital assets” as somewhat of a simple solution.

- As is the case with the language written into many bills, the text surrounding digital assets was, at best, overly vague, and at worst, so far-reaching that it theoretically threatened the digital assets industry in the US.

- The language sought to force digital assets “brokers” to report client activity to the IRS so that it could collect taxes from American tax-payers. What the bill also did was to define “broker.” However, the language was so vague that one could interpret miners, validators, software developers and peer-to-peer DeFi protocols as being brokers. This is when the lobbying efforts stepped in.

- Despite the proposed rules being difficult to enforce, and that they wouldn’t even begin to be implemented until 2023 (at the absolute earliest), the digital assets community mobilized leading to two competing amendments. Both were bipartisan, and both carved out miners/validators, as was the initial intent of the rule, but the Wyden (D-OR) amendment went further to support the industry than the Warner (D-VA) amendment.

- While the Warner amendment was being lobbied by Treasury Secretary Janet Yellen, the Wyden amendment was lobbied by the people. For days, both sides went back and forth, but for every step of progress that was made by the asset class, there seemed to be a counter. Things got a little heated at times, and at times seemed a little crazy, though that is understandable given the gravity of this technology and the fact that its many use cases are new to the majority of Congress.

All that said, nothing has been decided. Neither amendment saw a vote, and if I had to guess why the Wyden amendment never saw a vote, it’s because of political risk. As a Democrat, if you supported it, you were going against the Treasury Secretary’s wishes, and if you voted against it, you were potentially facing a large and unquantifiable backlash from constituents. I believe that most members of Congress are confused. They are used to dealing with strictly partisan issues, and digital assets/crypto blurs the lines. In some ways it’s ultra-libertarian, in others it’s so democratic that it borders on socialist. While longer-term I think that’s very positive, in the immediate term, it creates confusion.

My main takeaway from everything is that the lobbying efforts for the digital assets space were incredibly effective in exaggerating fear to the masses. Early last week, I was somewhat critical of the hyperbole on Twitter, and there is no doubt that it was hyperbole; however, I was very wrong. What these lobbying efforts did was to signal to Congress and the Administration that this is not some meaningless issue, but a massively growing asset class that represents the future of global technological innovation. This ‘sky is falling’ mentality brought this to the forefront, and Congress got the message. I’ve been following events like these for over 15 years and last week I called both of my Senators FOR THE FIRST TIME EVER. I’ve never done it because it usually doesn’t work, but this time it did. This time it was different.

What’s Next? While I don’t know exactly what will happen in the next couple of days, here’s what I imagine we will see. The Senate bill will pass as is. The House will accept it and it will be signed into law. The lobbying groups will continue to be loud in order to raise funds to increase their efforts on the Hill. I believe there is bipartisan desire to learn more about digital assets and that elected officials realize the impact of this technology and asset class spans both parties and all types of people in the US.

Between now and when the law goes effective in 2023 there will be considerable debate and clarifications made. This is not new nor unique. If you see anyone talking about this law being final, they’re completely wrong. Laws are passed all the time but often followed with formal fixes. I strongly believe that will be the case here. This will not be a draconian scenario for the asset class. Instead, it was the start of the regulatory process for digital assets- a process that will be a huge positive catalyst for the asset class.

EIP-1559, Ethereum 2.0 and the Road to Ether Becoming Money

Written by Arca senior macro analyst, Nick Hotz

Though it may dismay the legions displaying bat signals in their Twitter handles, ETH is not money. Good examples of modern money possess four features: you can spend it, you can earn interest on it, you can store value in it, and you can pay taxes with it. ETH currently meets one and a half of those, and that’s being generous. However, I’d argue that with the recent EIP-1559 and upcoming 2.0 upgrades, it will get much closer, perhaps even closer than Bitcoin, to what sound money should look like.

What EIP-1559 does for the you and me

Previously when making a transaction on Ethereum, users were forced to bid a gas fee, essentially guessing what the fee will be for a block and their transaction will either be included or rejected based on that guess. This so-called first price auction led to users consistently overpaying in gas fees to ensure they would be included in the block. EIP-1559 replaces this auction with a fixed price sale in which you are quoted a fee and can choose whether to accept the fee or not. In most cases, accepting the fee will get your transaction included in the block.

Instead of just the gas fee, EIP-1559 introduces two new components – the basefee and the tip. The basefee is what most users will care about. This is what the user pays to be included in the block and the component that is burned. The tip on the other hand is only paid by users who want to move towards the front of the block. Users willing to pay the tip are usually profit seekers searching for Maximum Extractible Value (MEV), arbitrage opportunities within DeFi for doing things like aligning prices between decentralized exchanges or liquidating underwater loans on Compound or Aave.

What EIP-1559 does for ETH

EIP-1559 is a key step towards ETH becoming a viable currency. It gives Ethereum a monetary policy that not only is credible, but also adaptable. Whereas many cryptocurrencies achieve credibility by hard capping their supply, Ethereum arguably does even better, adjusting its net issuance in response to current conditions. Like an apolitical, algorithmic Federal Reserve, EIP-1559 will tighten monetary policy by allowing fewer ETH to circulate in the ecosystem when transactions are filling up blocks and gas is high, but will loosen policy by burning fewer ETH when the opposite is true. And despite many people's reservations about the Fed, effective monetary policy is critical to stabilizing the burgeoning Ethereum economy and turning ETH into a viable store of value.

A lesser known but also extremely important characteristic is EIP-1559’s cementation of ETH as the reserve asset of the Ethereum economy, doing away with the potential for “economic abstraction” (don’t worry it’s not as scary as it sounds!). Before EIP-1559, technically people could pay miners whatever they wanted to get their transactions included in a block. Despite browser wallets like Metamask automatically forcing users to pay for transactions with ETH, this was not a requirement. With the introduction of the basefee, all transactions require a non-zero ETH burn to take place, meaning users will always need liquid ETH on hand to make transactions.

Looking at it from another perspective, the basefee essentially introduces a sales tax into the Ethereum economy, a tactic as old as time for strengthening a currency. One of the major reasons the U.S. dollar has value is because U.S. taxpayers are constantly required to spend it out of circulation in a variety of economic circumstances, and they cannot substitute any other asset – even other U.S. government liabilities like Treasury bonds – to do so. By crowning ETH as the sole asset able to pay the basefee tax and allowing users to spend ETH out of circulation, EIP-1559 greatly enhances the economic value of the asset supporting a burgeoning economy of DeFi, NFTs, DAOs and much more.

Nikhil Shamapant (aka Squish Chaos) made the case for a decoupling in correlations between BTC and ETH, writing:

“Most of the attention is being paid to whether the fees offset new issuance. I want to focus your attention instead on the mechanism of the tailwind. In the history of Ethereum’s price action, there was no direct connection between increased network activity and increased price. The price always rose purely as a result of the same investor activity as on the Bitcoin network, and so Ether has had a very high degree of correlation to Bitcoin. From this point on, however, if the Ethereum network’s activity is uncorrelated with Bitcoin’s price, we should begin to see Ethereum’s long term correlation with Bitcoin deteriorate as ETH price is no longer tossed around by the winds of speculation but grounded instead in its own network’s value creation”.

Ethereum 2.0: What’s at stake?

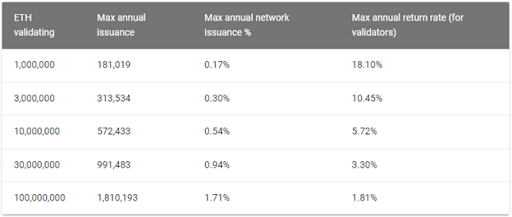

The final checkpoint on ETH’s path to money-ness will be the Ethereum 2.0 merge, expected early 2022. After the merge, Ethereum may start to look a lot more like the credit-based economy we know and, um, love today. The main economic difference between the current iteration of Ethereum and ETH 2.0 is the switch from proof of work (PoW), where miners validate the blockchain, to proof of stake (PoS), where users lock up ETH with validators to do so. These validators maintain the risk of being “slashed”, having a portion of their funds destroyed for noncompliance or inactivity. This slashing mechanic helps make PoS much more economically efficient than PoW. In an attack on a PoW network, a hacker must simply maintain a majority of the hash rate to allow block reorganizations, double spends, and all sorts of bad stuff. In Ethereum 2.0’s PoS, a would-be hacker must gather 51% of the ETH validating the chain (potentially around 10-20%+ of all ETH in circulation). Upon realizing the network was under attack, the community would fork (duplicate) the chain and slash the attacker’s funds on the new chain, forcing them to start all over again.

.png?width=1600&name=pasted%20image%200%20(21).png)

Source: Glassnode

This increase in efficiency will mean drastically lower issuance is required to secure the chain, on the order of 65-90% less. Running at just 0.5-1.5% annual issuance, ETH will likely see fees burned from transactions per EIP-1559 exceed issuance most of the time. Instead of Bitcoin’s disinflation (supply increasing at a decelerating rate), Ether over time will be outright deflationary (supply decreasing).

ETH issuance will no longer be paid to miners, but to ETH holders locked up in a staking contract. This variable yield, dependent on the amount of ETH staked in the contract, may set a sort of “risk-free” rate for the DeFi ecosystem, similar to the Federal Funds rate set by the Federal Reserve Board of Governors (more algorithmic monetary policy!). Most ETH holders will likely not deposit directly to the staking contract, but instead do so through intermediaries, both centralized (e.g. Coinbase) and decentralized (e.g. Lido). These parties will act like money markets for holders, providing the ETH depositors proxy assets that sacrifice liquidity for yield. The proxy assets like Lido’s stETH will become composable in DeFi and may even achieve near-level status with ETH for payments, deposits, collateral, etc.

However, because of ETH’s centricity in terms of liquidity in the ecosystem and its knighting from EIP-1559 as the only way to pay gas fees, we will never have to worry about ETH being supplanted by derivative assets. When liquidity dries up, like it did in March 2020, liquidity-sensitive investors sell Treasury bonds to buy dollars because dollars have special status as a medium of exchange and tax-payment asset within the U.S. economy. With its upgrades in place, ETH gains that same privilege.

The flows into the staking contract also serve to artificially reduce the supply of ETH available. When assets are locked up in staking, they are unable to be sold, which has the potential to increase the perceived value of unstaked ETH. If demand flows remain the same or even increase, we may see what amounts to a supply crisis for ETH as investors scramble to obtain the increasingly illiquid asset to store value in and pay fees with.

A final, perhaps obvious point is that despite having liabilities to pay out to stakers, Ethereum will retain what economists call its “monetary sovereignty”, meaning it only pays out liabilities in the asset it is able to print. Monetary sovereigns in the world like the U.S.A., Japan and Australia are in a powerful position since they can never voluntarily default on their debts. Since Ethereum is a currency issuer that only spends ETH, it can never default. Compare this with a typical U.S. company or even Greece in the early 2010’s which accrued liabilities in a currency (USD and Euros, respectively) which it could not issue. In this situation, default is always a risk weighing on the mind of an investor, but never a risk for ETH holders.

Currencies hold a powerful status in modern society as the only assets you can spend, store value in, earn interest from, and pay taxes with. While ETH is currently only used as a medium of exchange in its ecosystem, over the next 12 months it will gain many of the other properties of money. EIP-1559 and Ethereum 2.0 establish a powerful, adaptive monetary policy via basefee burning, cement ETH’s role as the central asset in the ecosystem by ensuring it will be preferred liquidity asset, create an algorithmic risk-free interest rate for DeFi, and make ETH dramatically scarcer. With these features in place, the case for Ether as a reserve asset for the age of decentralized digital money looks much clearer.

What’s Driving Token Prices?

Ethereum (ETH) was the talk of the town last week, as noted above, and the token followed suit with a +15% week-over-week gain. Elsewhere, a few other tokens had idiosyncratic events leading to price action:

- AAVE (+18%) - Aave's borrow outstanding recovered, rising +8.5% WoW, outpacing MKR and COMP. At Chainlink's smart contract summit, Aave announced it was exploring/working on expanding Aave to Solana, Avalanche and L2 solutions, Optimism and Arbitrum. The move would be great for Solana and Avalanche and would allow Aave to utilize liquidity across multiple protocols. Finally, Bitwise launched an AAVE specific fund for clients.

- UNI (+27%) - Bitwise also announced the launch of a UNI specific fund for clients.

- RUNE (-2%) - the team released a more detailed blog following the post-mortem on specific tech improvements to be made to the protocol. The network is currently still paused.

- SOL (+7%) - TVL rose to $1.5 billion, the highest since early May. Phantom (the most usable wallet on Solana) launched staking capabilities in the UI.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Junior Portfolio Manager - Special Situations Analyst

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

Andew Stein, VP of Research

Kyle Doane- Trader Operations Associate

Matt Hepler- VP, Portfolio Manager

Nick Hotz- Sr. Global Macro Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)