The idea of digital securities was born out of the 2017 ICO boom and has been a topic of conversation ever since. Bringing the efficiencies of blockchain, such as instant settlement and embedded auditability, to the $1,600 trillion global securities market is undoubtedly an attractive value proposition for both securities issuers and investors. Since the first digital security issuance - which was actually a securitized fund - the question of how to tokenize existing traditional financial instruments still lingers. The challenges of integrating existing financial structures and infrastructure with blockchain technology span from technical to regulatory, among others. Arca Labs, Arca’s innovation division, has addressed some of these challenges with the launch of ArCoin in July 2020. The Arca U.S. Treasury Fund is registered under the Investment Company Act of 1940 (“ ’40 Act”) and is the first closed-end fund to issue digital shares on the blockchain. The team has learned a lot over the course of the past year and we’re here to share our learnings and dive deeper into our view of the future of issuing digital asset securities.

The Removal of the Need for Brokerage Firms

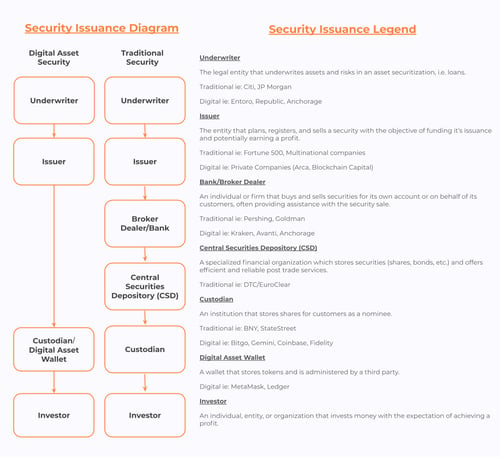

One of the core elements of creating a registered fund in the United States is appointing the required service providers needed to perform the operational elements of the fund. For a traditional ‘40 Act fund, these service providers include but are not limited to, an administrator, auditor, custodian, distributor, legal counsel, transfer agent, and adviser. Traditionally, ‘40 Act fund shares are held in street name at a brokerage firm, but digital shares, issued on the blockchain, enable investors to hold their shares (via wallets) and to manage the transferability of the shares in a peer-to-peer fashion. In the case of the Arca U.S. Treasury Fund, subscriptions into the Fund are issued in the form of digital asset securities, or digital 'shares', known as ArCoin, and issued on the Ethereum blockchain.

Digital shares, such as ArCoin, have the potential to offer efficiencies for shareholders as they have enhanced features when compared to traditional shares; acting as both an investment and a medium of exchange. The digitization of traditional financial instruments also provides investors with the potential for lower fees from fewer intermediaries, faster settlement, and automated agreement execution. However, change does not come without further questions. In order to understand how digital asset securities are maintained, let’s review how traditional assets are issued in comparison to the new digital workflow.

Currently, digital asset securities are issued in two key ways: in a permissioned blockchain or on a public blockchain via smart contracts. A permissioned blockchain, such as Symbiont, is essentially a controlled environment allowing tokens to exist in a closed ecosystem. Permissioned blockchains are generally preferred by users for their privacy. A digital asset security can also be issued on a public blockchain, such as Ethereum, where security features are built into the token in addition to the blockchain itself so the token can exist in an open ecosystem. Further, public blockchains give participants the opportunity to build freely, making public blockchains experimental ecosystems that offer creativity.

Will permissioned blockchains prevail or will public blockchains be the issuance norm, and is there room for both? The debate between which form of issuance is superior is an intense debate in the blockchain community. Some believe that private blockchains are inferior because they fail to embody blockchain’s principle of decentralization. Supporters of private blockchains say there is no way that institutional adoption can occur on a public blockchain, which they see as overly transparent and risk inviting. Finally, supporters of public blockchains argue that public blockchains are the only path toward mass scalability and innovation, as private blockchains lack the open-source innovation seen in public blockchains.

WHY DOES ISSUANCE MATTER?

Over the course of decades, the methods of traditional security issuance have been commoditized by banks, broker-dealers, and issuers. In digital asset security issuance, the jury is out on which thesis will prevail. In our view, scalability and security are two of the most important factors for the digitization of financial products. Digital asset securities, such as ArCoin, are required to comply with security regulations like know your customer/ anti-money laundering (KYC/AML) guidelines and whitelisting* requirements. In addition, digital asset securities offer enhanced features like mint, freeze, burn, and replace controls which allow issuers to affect the movement of tokens. Without smart contracts, a digital asset security could not adhere to these regulatory requirements. Permissioned and public blockchains have enabled the growth of the digital asset ecosystem over the past decade. At Arca, we are striving to pave the way as innovators of digital asset securities. We applaud the evolving digital security community as it pushes forward product development and comprehensive services with the goal of stimulating the continued growth of this digital asset ecosystem.

* “One aspect of compliant security tokens involves ensuring that only eligible token holders are indeed holding the tokens. An easy way to do this is through the creation of a list of approved addresses, called a ‘whitelist’, which represents authorized token holders.” - Tim Fries, The Tokenist

"At Arca Labs we're breaking through the current limitations, we're developing cutting-edge solutions, and really we're accelerating the evolution of finance."