When Does a Bear Market Rally Turn Into Just a Rally?

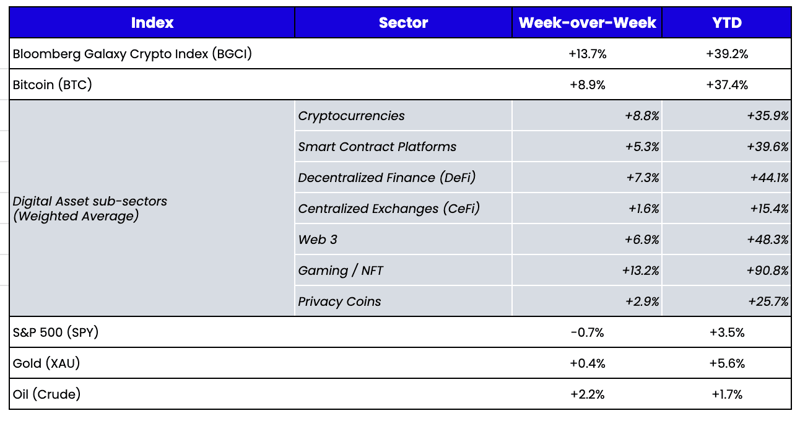

The 2023 digital asset recovery continued last week, with another week of near double-digit returns. The price action was almost in a straight line higher, with only the slightest hiccup when the DOJ teased a large enforcement action many assumed would be against Binance. Instead, it focused on a small and largely obscure Russian exchange, Bitzlato.

4Q laggards, including Bitcoin, again led the rally, as the tokens of applications and protocols largely left for dead have seen a sharp renaissance. As a result, it’s difficult to tell if this is just a bear market rally or if the price increases will reflexively spark enough economic activity to justify the price moves. At a micro-level, most individual applications and protocols are still near trough levels of users and activity. Still, in many cases, they are also up well over 100% in recent weeks—DEX volumes, NFT activity, and Layer 1/Layer 2 protocol activity fit this description. The market is trying to find equilibrium—something between last year’s dead zone and 2021’s euphoria.

Decentralized Exchanges: Volumes Grew 60% WoW But Remain at Trough Levels

%20(1).png?width=710&height=243&name=image%20(2)%20(1).png)

Source: Arca Internal calculations

At a more macro level, broadly speaking, it’s much easier to justify the quick start to the year. Almost every broad indicator that was a headwind in 2022 (the U.S. dollar, inflation, interest rates, credit spreads, energy prices) has now become a tailwind. Both equities and credit are off to historically fast starts to new years. And blockchain-focused bankruptcies are becoming more telegraphed and less impactful.

The Genesis bankruptcy is yet another example of “bad outcome for equity holders, good outcome for token holders.”

Thoughts on the Genesis Bankruptcy

By Michael Dershewitz, Head of Risk Committee

A long-running public insolvency finally reached its endgame when Genesis filed for Chapter 11 bankruptcy protection last week. We had forecast this outcome months ago—as did many other market participants. Genesis had been in negotiations on an out-of-court restructuring for weeks with its largest creditors—most notably, the Winklevoss-led Gemini—but the parties could not reach an agreement. Importantly, Genesis Global Holdco LLC and two of its lending business subsidiaries, Genesis Global Capital LLC and Genesis Asia Pacific Pte. Ltd., filed, but Genesis Global Trading brokerage did not. Chapter 11 is a useful process to stay liabilities and negotiate a court-approved restructuring. As advisor Paul Aronzon wrote in first day filings:

Now that negotiations have changed from backroom talks to the public bankruptcy court, we will watch closely how this plays out for two prominent industry players in Genesis and its parent, Barry Silbert’s Digital Currency Group (DCG). The Chapter 11 filing envisions an expedited 90-day process to market company assets, finalize any support from DCG relating to its equity ownership and intercompany promissory note obligation, and strike a deal with creditors. We cannot add much to predict how these negotiations will end, but we are watching at the edge of our seats.

That said, we have pored through all filings on the docket and spoken to professionals on the case to synthesize lessons learned and determine where the puck is going. Here are some key conclusions:

1) The Genesis bankruptcy represents the end of the forced selling of assets—especially the Grayscale trusts. Since extreme distress started for Genesis (and DCG) post FTX’s demise, market participants have wondered if phenomena such as the unusually large discounts to NAV for GBTC, ETHE, and other DCG-owned Grayscale trusts could be attributed to technicals. We wrote about this last month and predicted a bullish market reaction from the closure of forced selling.

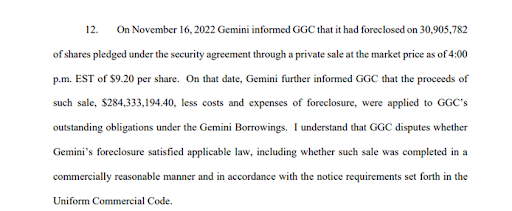

Now that Genesis has finally filed, we have proof: Gemini liquidated about 5% of GBTC shares in November that were being used as collateral for the loan from Gemini Earn to Genesis. This liquidation caused an artificial widening of spreads to record levels. These shares were liquidated at $9.20/share—24.4% below the closing price of shares on January 20. As Michael Leto from restructuring advisor Alvarez and Marsal wrote in first day filings:

Furthermore, regarding Grayscale, not only is forced selling halted now, but DCG’s decision to file Genesis instead of raising capital for creditors likely removes any near-term impetus to monetize the trusts. We continue to believe that over the fullness of time, the Grayscale NAV discounts will continue to converge back to spot, and see Chapter 11 as a positive entry point.

2) DeFi again proves superior to CeFi for risk management. The 2022 bankruptcies of FTX, Celsius, Voyager, and other centralized financial institutions clearly illustrated their inadequate risk controls, poor accounting, and chances of damaging frauds. On the other hand, DeFi has passed every stress test. Its formulaic collateral and risk management mitigate damaging losses, and on-chain data makes fraud almost impossible. We have written about this theme many times.

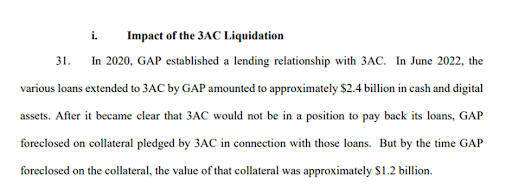

The Genesis bankruptcy is now another prime example of the relative failure of CeFi. It has been known that Genesis had $2.4B of impaired loans to 3AC, but first day filings revealed the extent of its risk management failure. Interim CEO Derar Islam wrote:

DeFi would not have been asleep at the wheel like Genesis’ risk management was. Instead, it would have foreclosed on that collateral much faster, given predefined rules, potentially mitigating losses and avoiding insolvency entirely. It’s shocking how fast we went from “most customers don’t care about decentralization” to “the only customers who weren’t crushed this year used DeFi lenders.”

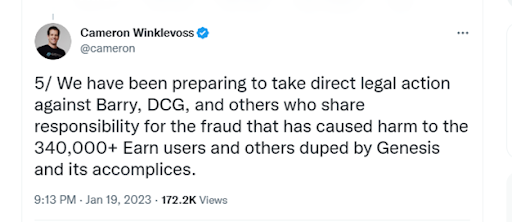

3) Prudent structuring is superior to public spats. As first day filings bear out, we know definitively that Gemini Earn is the largest creditor to the Genesis estate. While the parties were negotiating behind the scenes, a lack of progress caused Cameron Winklevoss to accuse DCG of misdeeds publicly. Upon Thursday’s filing, he followed up with tweets threatening legal action:

We will see what comes to light in court and if Gemini can use the fact pattern to force compensation from DCG, leading to a better recovery. However, the first day filings from Michael Leto also revealed to us that Gemini could and should have been more rigorous about structuring and managing the relationship. This loan does not seem to have been set up under separately managed accounts, which could have given Gemini more control. The loan appears to have been uncollateralized since before August 2022, only after 3AC’s demise. Finally, the health of Genesis seems to have been overstated through a cursorily communicated “Gemini Risk Metric Request” versus what proper counterparty diligence would have revealed.

Public complaints about Genesis’ misdeeds and obfuscations are understandable. However, some of this mess can seemingly be attributed to relaxed loan structuring and counterparty operations.

As a final point on Gemini, we also recognize the dark humor in the initial Plan of Reorganization regarding their envisioned recoveries. Gemini lenders are importantly granted a separate creditor class that separates them from all other Genesis creditors, although these creditors should be pari passu. Gemini recoveries are identical to other creditor recoveries as pro rata on their asset pool, with the sole addition of Class C1 and C2 recoveries. What are Class C1 and C2 recoveries? As defined in the plan, any proceeds from legal actions against…Gemini. Thanks, Cameron; we’ll poke the bear right back!

4) DCG’s future remains fragile. The likely proximate cause for the Chapter 11 filing of Genesis was a breakdown in negotiations with creditors. Days before the bankruptcy, the media incorrectly predicted an out-of-court settlement with Genesis creditors seeking a mix of cash and equity from DCG. Equity is an easy ask, but there is a high chance of a scarcity of cash at DCG, thereby torpedoing the requested framework. This likely translates into financial distress at DCG that may lead to their own Chapter 11 if not properly handled.

All is not lost, as DCG has two valuable assets they can monetize: the Grayscale trusts worth an estimated $600M-$1B and their extensive VC portfolio worth an estimated ~$500M at current market pricing. However, there are significant upcoming obligations against these assets. The highly public loans are the ~$550M in intercompany loans owed to Genesis in May 2023 and the notorious $1.1B promissory note owed to Genesis that matures in 2032 that is said to be not callable. While problematic, both debts may be restructured in favor of DCG flexibility as part of a global Genesis settlement. However, there is one more liability that we would like an update on—DCG’s $350M facility with Eldridge Industries. We would particularly appreciate an update on the capital drawn from this facility and if there are any cross defaults between it and any of the Genesis loans that may have just triggered. Given the lack of updates, our suspicion is that precious DCG cash was sent to Eldridge to refinance that facility and remove one threat while opting for Genesis’ Chapter 11 to mediate the other.

From a legal perspective, this story isn’t going away any time soon. But from a market perspective, it’s quite clear that it will have very little impact on anyone other than Genesis and DCG creditors.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari