Over the last few years, we’ve released annual predictions focused on the source of growth for digital assets. Over the years, we got a few big ideas right:

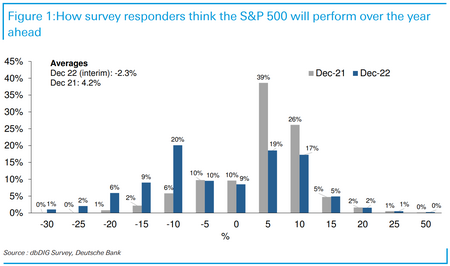

In 2022, we got little right. In fact, we missed the mark on just about everything, but we weren’t alone. In a Deutsche Bank survey at the beginning of 2022, only 19% expected a negative return for the S&P 500 in 2022, and only 3% thought the return would be less than -15%. The S&P 500 lost almost -20%. Naturally, this year, 39% expect a negative return of more than 10% for 2023.

Source: Deutsche Bank

Projections are a mixed bag. While it’s nice to have an investment plan, how investors react to new information throughout the year ultimately matters much more for returns. So in 2023, we will set the stage for our expectations of investment growth, but we will stay nimble to process the inevitable flow of new information.

Overall, we believe 2023 will be a bounce-back year for digital assets, both in terms of prices and fundamental growth and usage. For a broader perspective, we reached out to Arca team members across legal, compliance, marketing, business development, and labs/innovation. We also tapped the investment teams from our venture, liquid, and NFT portfolios.

Prediction #1: Digital assets as an asset class will continue to decouple from traditional markets and remain uncorrelated for the foreseeable future.

If you’re a blockchain enthusiast, none of the events of 2022 should shake your thesis. Many of the castles built around blockchain fell, but the blockchains themselves worked. On the other hand, if you’re a blockchain skeptic, none of the events of 2022 should give you reason to change your thesis either. Growth and adoption slowed, and many use cases are still siloed. However, from an investing standpoint, the second half of 2022 should have changed your outlook on correlations. While central banks’ responses to rising inflation drove negative returns and high correlations in the first half of 2022, the second half of 2022 was defined by digital asset-specific events. From the Terra Luna/UST collapse to the Ethereum merge, the seemingly endless string of bankruptcies to the FTX fraud, digital assets (outside of Bitcoin) decoupled from traditional debt and equities.

While most of the idiosyncratic events in 2022 were negative, 2023 will likely bring the opposite. Many casual blockchain investors felt that investing in the equities of blockchain companies was a safer way to express a view on the growth of blockchain. This perspective led to investments from pension funds and TradFi funds into the equities of FTX, Celsius, BlockFi, Voyager, and many others that are now facing recoveries of zero. Meanwhile, even the failed Terra Luna blockchain (formerly LUNA, now LUNC) still carries a $1 billion market cap because protocols can’t go bankrupt, and the perpetual optionality alone of a future use case for a functioning blockchain is still worth something. If your thesis is that blockchain will succeed, it’s not your thesis that needs to change, but rather how you express that thesis. A common narrative for many years was that equity provides downside protection. The reality is that tokens actually have less downside than equities because they are perpetual call options with high volatility and no ability to get zeroed out in a restructuring. We wrote about this in 2019, suggesting that the “lack of intrinsic value of tokens” is a lazy argument for not investing since most debt and equity instruments trade at massive multiples above intrinsic value anyway.

Heading into 2023, this thesis is about to be tested. Many companies (both in the blockchain industry and elsewhere) will face restructurings due to high debt loads and low cash flows, leading to low (potentially zero) recoveries for the equity and lower trading multiples for those that avoid restructuring. Meanwhile, most tokens are hybrids, exhibiting both equity-like properties tied to the cash flows of the enterprise, but also utility value in the form of usage and rewards. That utility value (or expected future utility value) will provide a floor on tokens, while the financial value will provide operating leverage to the upside. This fundamental difference between tokens and their debt and equity counterparts will lead to even further differentiation and low correlations. And as we wrote in 2020, even if we enter a recession, digital assets will likely prove to be far more recession-proof than equities. In 2023 and beyond, there will be a more overt distinction between investing in blockchain technology infrastructure, Web3, and cryptocurrencies.

Prediction #2: The onboarding of Web 2.0 and TradFi corporates will drive Blockchain growth

Public and privately traded tokens represent slightly less than $1 trillion of market cap—75% of which is made up of just BTC, ETH, and stablecoins alone. It is estimated that there are roughly 200 million users of blockchains today—of which only a fraction (10-20 million) are active users. While this is no small feat for such a young industry, it’s no massive success story. There are individual businesses with more users than the entire digital asset industry: Visa has 300 million customers, iTunes has 225 million customers, Delta has 100 million customers, and Starbucks serves 60 million customers per week.

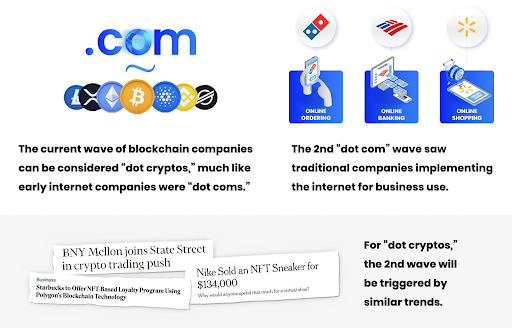

While the organic growth of blockchain-native companies, protocols, and applications is cute, it pales in comparison to the growth blockchains will see when they onboard existing users of much more prominent, established non-crypto companies. The current wave of blockchain companies can be considered the “dot cryptos,” much like early internet companies were “dot coms.” But the second wave of the internet’s success came when traditional companies that had been around for hundreds of years started to use the internet for business. The same will be true for blockchain as traditional companies adopt the technology’s benefits.

Tokens and NFTs are the most remarkable fundraising and capital formation tools ever created. They have become the greatest customer bootstrapping and incentive/alignment system we’ve ever seen. Much like companies began to see the benefits of the internet 20 years ago, they will start to see the benefits of tokenization. While U.S. regulations currently restrict the ability to issue “corporate tokens,” for now, companies will continue to dabble with DeFi transactions and NFT issuance. Large corporations like Nike, Starbucks, Reddit, KKR, Apollo, and more are becoming pioneers; others will surely follow. Web 2.0 companies will continue to utilize NFTs to strengthen customer relationships. And when this happens, a layer-1 protocol can onboard as many users in a single day from these existing user bases as they have in a lifetime organically.

Utility with tangible value propositions will drive the long-lasting adoption of digital assets.

Prediction #3: TradFi and centralized finance will continue to lose market share to DeFi

For every failed exchange like FTX and Voyager, there was a perfect substitute in DeFi (Uniswap, dYdX) that had the same customers but thrived through the chaos.

For every failed lender like Genesis, Celsius, and BlockFi, there was a perfect substitute in DeFi (MakerDao, Aave, Compound) that had the same customers but thrived through the chaos.

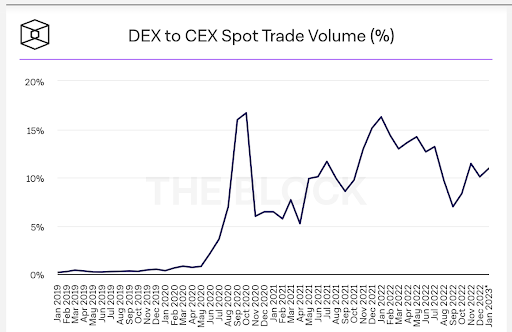

While many are currently discussing 2022 and its failures, the year may one day be remembered for enduring a successful stress test of DeFi. Last year, DeFi protocols with similar business models as their CeFi counterparts performed admirably despite negative market environments. None of the protocols went down, none created bad debt in excess of their assets, and none completely wiped out their investors. In the past two years, we’ve already seen digital asset trading move from entirely centralized to over 10% of volumes traded on decentralized protocols. A similar trend will likely continue for decentralized derivatives exchanges and decentralized lenders. Eventually, this will move beyond the siloed walls of digital assets, and we’ll also see real-world trading and lending from banks and brokerages on blockchains.

DeFi has really only been relevant for a little over two years, but each time a stress test is passed, it increases the likelihood of further usage and adoption. Further, an increased focus on transparency, immutability, and analysis will help DeFi gain market share. Finally, although the market size shrunk during the “crypto winter,” we will continue to see traditional financial services companies announce plans to enter the blockchain ecosystem.

Prediction #4: Thematic investing

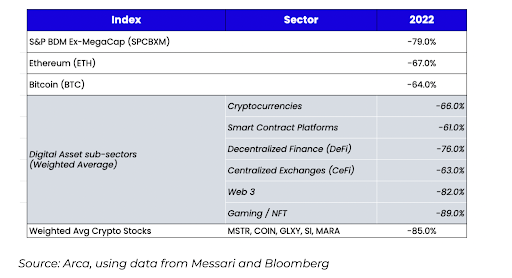

In 2022, the lack of dispersion was the biggest difference between digital assets and other asset classes (outside of the abject failures and frauds). In equities and fixed income, sectors mattered.

For example, energy greatly outperformed tech. But correlation has never been higher within digital assets, and dispersion has never been lower. So while there were a few tokens and equities of blockchain companies that effectively went to zero (and therefore significantly underperformed), for the most part, it did not matter what you invested in—the asset class itself was the problem.

In 2023, this will likely revert to normal. From an investment standpoint, thematic investing will once again reign supreme. The top themes that Arca’s research team is considering are:

- On-Chain Identity or Decentralized Identity (DIDs): The creation of identity products on-chain will solve the problem of potential KYC/AML issues, allowing institutions more comfort when interacting with crypto projects. Additionally, it allows for more efficient use of capital as we can also have on-chain credit.

- Broad Corporate Partnerships and Adoption: 2022 saw the likes of Nike, Starbucks, Meta/Instagram, and a slew of other large Web 2.0 corporations announce their strategy for digital assets, primarily geared toward consumer/brand loyalty initiatives. 2023 will be all about if and how these companies execute on this vision and if it drives more users into digital assets.

- Scaling: Simply put, the last bull cycle showed us the importance of blockspace and that most smart contract platforms could not handle the massive volume of users and transactions in their current iterations. As a result, scaling solutions would be critical infrastructure for widespread adoption. Importantly, we believe that the themes mentioned above can only be accomplished with proper scaling solutions. This theme encompasses layer-2 solutions on Ethereum and non-Ethereum layer-1 solutions.

- Non-custodial Wallets: The blowups of most centralized counterparties in the space reminded us why crypto was created in the first place—to cut out middlemen. Exchanges and centralized lending protocols have become those intermediaries. As the ecosystem has grown, users have gotten complacent and chosen to trust the intermediaries instead of custodying their own assets. 2022 reminded everyone of the expression, “not your keys, not your crypto.” Therefore, we will see the emergence of more non-custodial wallets and other storage solutions, as well as a potential resurgence in DeFi.

- Security and Testing: Without harping more on what 2022 taught us, we saw an unprecedented number of hacks, exploits, and bad actors last year. The lesson is that the space needs more rigorous security and testing practices going forward. We cannot continue to “test in prod.” Whether it’s products that offer simulation stress testing for DeFi protocols, greater security of private key storage, or transparency around exchanges/custodians, these initiatives must be taken seriously by the next cohort of builders.

- Web3 Social Movement: The Web3 social movement has had a few moments in the spotlight over the past 3 years, but given recent events at Twitter, there seems to be a concerted push now more than ever for a decentralized social media platform. The hope is that with true Web3 social, users will have ownership over their data and brand and can monetize those things instead of lining the pockets of large corporations.

Prediction #5: Distressed investing will lead to outsized returns, but few will participate

Most native digital asset investors come from a technology or venture investing background and have little experience with distressed investing. Most distressed debt investors and funds are too big to bother with small retail claims at BlockFi, FTX, Voyager, Celsius, Genesis, and others.

As a result, there will be a significant opportunity to access the growth of digital assets with less downside volatility and limited competition for those that have a 5-7 year time horizon, a smaller asset base, and an understanding of both digital assets and bankruptcy proceedings.

Distressed investing in blockchain will be an important driver of returns in 2023 and beyond and will likely extend beyond the current crop of exchanges, lenders, and miners. Those who spend the time reading through dockets and sourcing claims will likely see 5-10x returns over the course of 5-10 years.

Concluding Thoughts: The 2018 bear market produced a 3-year stretch of outsized positive returns, and that was during a time when blockchain really hadn’t produced much product-market fit. The 2022 bear market already has four legitimate use cases: Stablecoins, DeFi, NFTs, and Bitcoin. This space has come a long way in the last 3 years, while the majority of investors ignored or didn’t fully understand the investable universe. If we see a similar renaissance and recovery, imagine the possibilities now that the entire world is watching.

Stay tuned for updates on these themes and predictions as we progress through 2023.

Source: The Block

Source: The Block