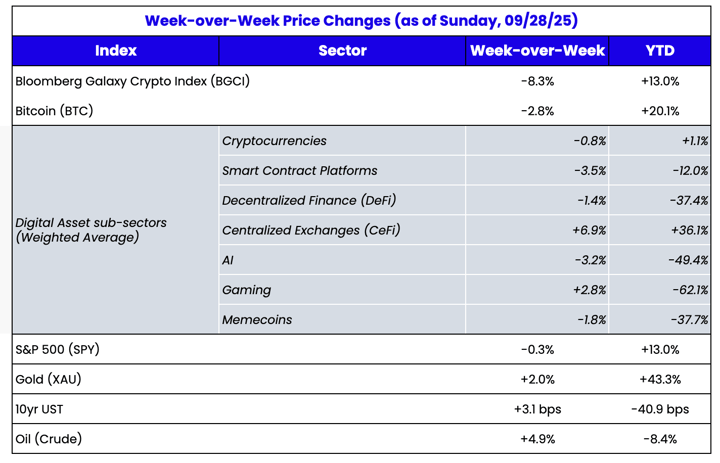

Source: TradingView, CNBC, Bloomberg, Messari

The Market is Heating Up Even as Prices Fall

Last week, we

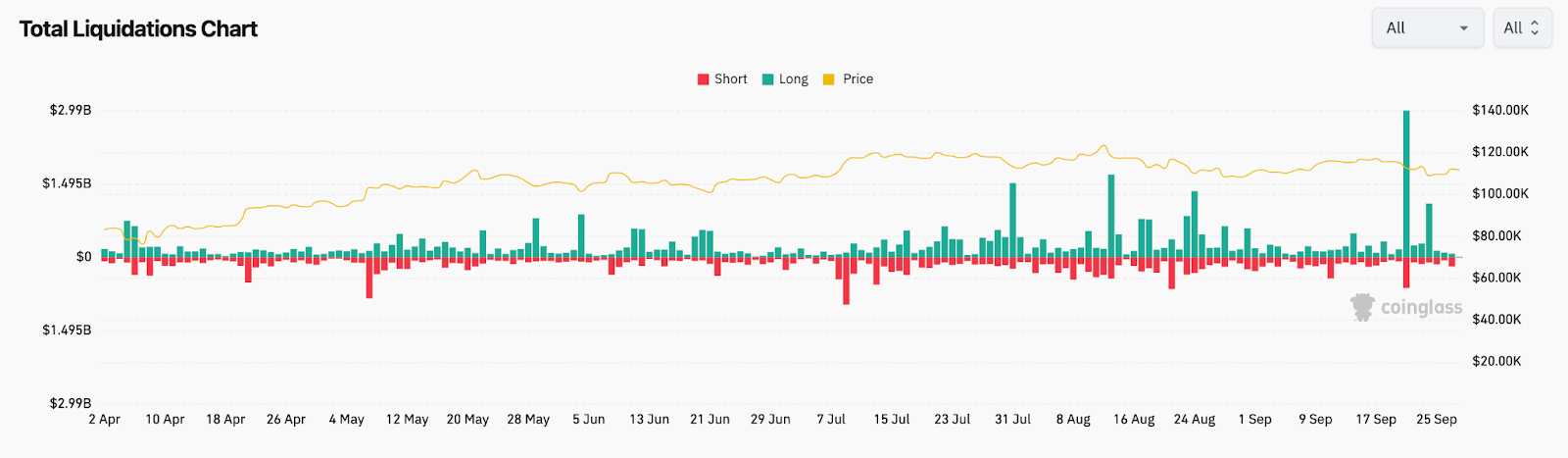

wrote about an incredibly busy week in crypto that didn’t quite translate into higher prices. This past week was similar, as the market was once again hit with an onslaught of seemingly positive news, yet prices fell, largely led by futures liquidations in BTC and ETH. Just under $4 billion of futures positions were liquidated last week, the highest weekly figure of 2025. The previous weekly highs were during the first quarter of 2025, with liquidations almost half of those seen this past week, driven by concerns about rate hikes, geopolitical tensions, and tariffs. But I couldn’t tell you what drove the selloff last week other than an exhausted buyer base turning short-term traders into top callers.

This deleveraging reduced open interest by ~10-15% from the September peaks, potentially setting up cleaner upside into the historically strong 4Q.

Among the more positive news, Tether, the world’s largest stablecoin issuer, is reportedly seeking to raise $15–20 billion in a private placement that could value the company at approximately $500 billion, placing it on par with giants like OpenAI and SpaceX. CEO Paolo Ardoino confirmed the potential raise, stating that it would fund an aggressive expansion across stablecoins, AI, energy, commodities, and media. The move comes as Tether’s USDT supply has surged to over $170 billion and follows new initiatives like the launch of Plasma, a stablecoin-focused L1, and plans for a U.S.-regulated stablecoin (USAT). While some are pointing to Circle’s $30 billion market cap as a comp, these are much different businesses. First, Tether has much higher operating margins since Circle has a huge business development team, and pays out a majority of its revenue to Coinbase and Blackrock via distribution agreements. Second, Tether has a lot of other business lines and investments due to the $3-6 billion in annual profits its earned over the past few years. As Galaxy Digital wrote in their weekly note to clients,

“The fundraising announcement also reinforces Tether’s evolution into something more than just a stablecoin issuer. Beyond tokenizing dollars on-chain, it wants to ensure those dollars circulate with the least friction possible. The company highlights AI, telecommunications, Bitcoin mining and energy, cloud computing, real estate, and even neurotech as other areas of expansion as it seeks to build a “resilient, long-term infrastructure for the digital asset economy.” In 2023, Tether invested over $600 million in Northern Data for AI infrastructure. In 2024, it paid $200 million for a majority stake in Blackrock Neurotech to advance brain-computer interfaces.”

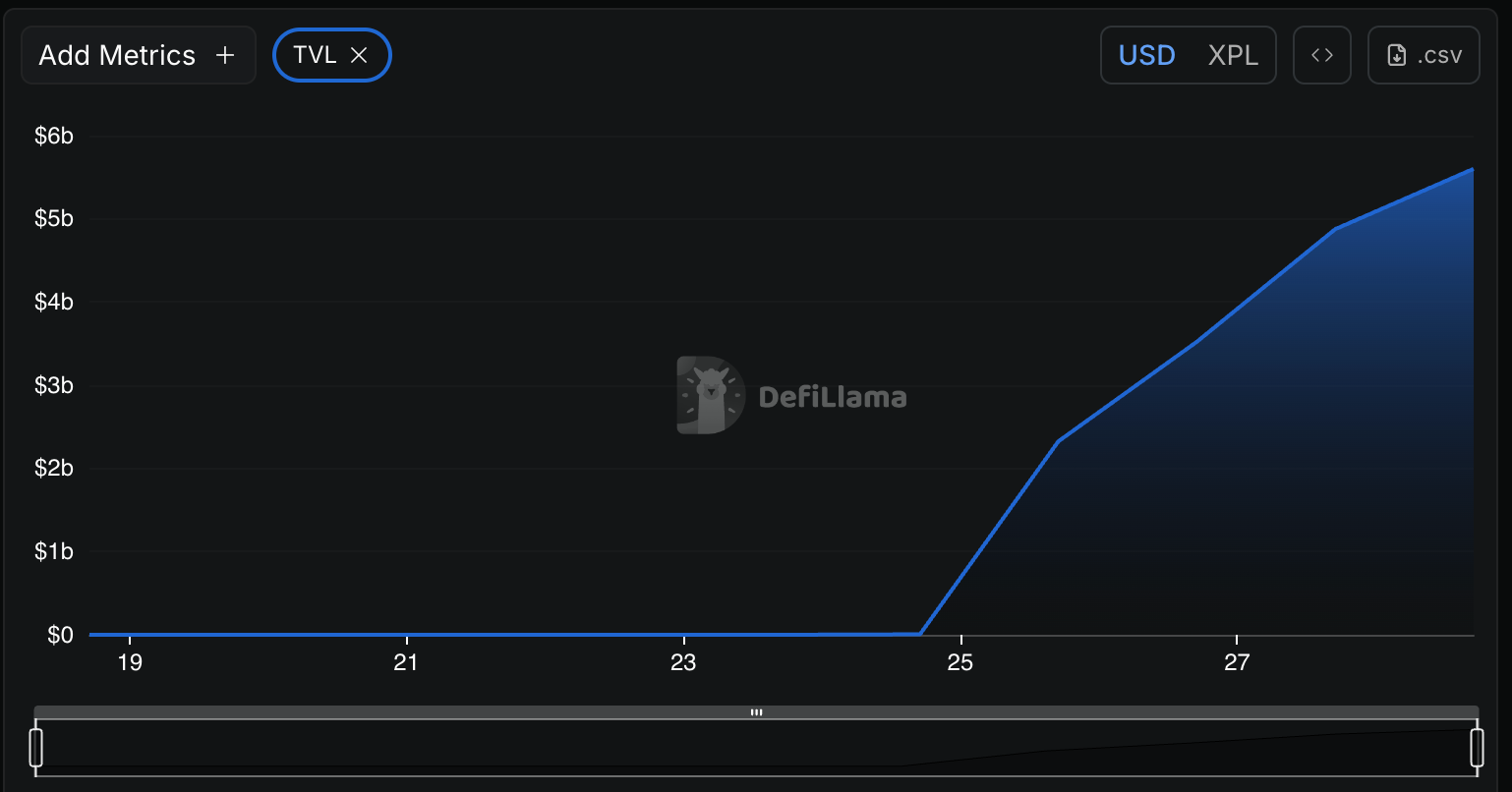

Speaking of Plasma, the long-awaited launch of its XPL token was one of the bright spots last week. The token was issued in a private sale a few months ago at $0.05, traded up to roughly $0.70 in pre-market futures contracts on Hyperliquid and Binance, and closed the week at $1.40 after the token itself began trading this week. The bull case is straightforward: the market loves anything related to stablecoins (as evidenced by the lofty valuations of CRCL stock and ENA), and especially loves anything related to Tether. Using “stablecoin supply to market cap” ratios, XPL has some room to run to catch up to Tron (TRX), but already looks expensive relative to other chains that have high stablecoin activity. The TVL growth for a new chain was extraordinary and quick.

Source: DefiLlamaMore importantly, the successful XPL launch demonstrates that even in a relatively benign bull market (

if it can be considered a bull market at all), investors will still invest heavily in good projects with strong narratives and robust growth engines. And stablecoin chains certainly fit that bill.

The Perp-DEX Wars Begin in Earnest

We often discuss how decentralized spot exchanges (DEXs) have been steadily eroding the volume share of centralized exchanges (CEXs). The data is undeniably a trend.

But until very recently, derivatives markets remained a fortress for centralized venues. Binance, Deribit, Bybit, OKX, and others have had a stranglehold over the decentralized derivatives market (Perp DEXss). But for the first time, decentralized derivatives (driven by perpetual futures) are gaining real market share against centralized derivatives.

What makes this moment even more fascinating is that it isn’t just about a handful of small Perp DEXs, but rather a full-blown arms race among Perp DEX incumbents and insurgents.

Prior attempts, such as dYdX hinted at what could be, but they never managed to crack CEX dominance. Today’s competitors are different because on-chain infrastructure, low-latency settlement engines, and novel token-incentive models have matured enough to offer a credible substitute to the CEX incumbency. Perp volume on DEXs is

hitting trillions annually, and Perp DEXs now command a nontrivial share of the total derivatives market.

The question many are now asking is, “Who will capture the lion’s share of that on-chain derivatives upside?”

It’s a good question, but perhaps not that important for investing. Wars are good for investors, because people spend money to win wars. A rising tide generally lifts all boats. While most crypto investors think you have to constantly play a game of token “hot potato”, selling one token for the next shiny new thing, the more rational answer might be to figure out what allocation you want to the overall Perp DEX industry, and own a little bit of ALL of the players involved.

This week was by far the largest perp DEX volume week ever. Hyperliquid started the recent craze and continues to be the leader in the clubhouse, with cumulative volume and revenue numbers that are eye-popping (over $1 billion+ annualized revenue). They’ve architected a model that aligns native token holders, liquidity providers, and traders. Hyperliquid also operates its own L1 architecture, featuring zero gas fees for trading, fully on-chain order books, and transparent markets. Since the path to L1 blockchain success is vertical integration (

own the chain, the DEX & the stablecoin), Hyperliquid has a clear advantage right now.

With Hyperliquid’s current size and dominant open interest and liquidity, it is still the king, but that buffer is thinning.

Enter, the challenger – Aster (and others).

The ASTER token launched last week, and it too was an immediate success like XPL. ASTER’s token skyrocketed from ~$0.17 to ~$1.90 in days, generating a ~1,000%+ move. Whereas Plasma (XPL) is a stablecoin chain with investments from Tether, ASTER is a perp DEX with investments from Binance and CZ himself. As of late September, Aster is now generating nearly $10 million in 24-hour revenue, surpassing Circle and Hyperliquid, and ranking just behind Tether. On one recent day, Aster recorded $36 billion in 24-hour perp volume, which more than doubled the total perp DEX activity that day. Hyperliquid, by contrast, recorded $10 billion+ on that same day.

Aster is making aggressive bets on synergies, by combining spot, perps, yield, a stablecoin, and eventually a chain. It aims to capture the entire session of a trader (funding, settlement, margin, yield). Sound familiar? See the trend here? Own the chain, the DEX, and the stablecoin.

While the current volume appears somewhat suspicious (with heavy wash trading and an unusually high level of trading relative to open interest and liquidity), ASTER is definitely competing in the war for attention and liquidity. Will users stick around once incentives fade or token emissions taper? That’s anyone’s guess, but it’s clear that winning the Perp DEX wars is a fight worth fighting. Meanwhile, Hyperliquid will likely respond with more aggressive fee cuts, new incentives, and deeper integrations. They have an aptly named “war-chest” available to win the war.

Other challengers (Lighter, BULK, edgeX, Drift, Pacifica, Zeta) are also entering with variant strategies (execution, fee routing, hybrid orderbook/AMM, MEV defense, etc.). Expect more “vampire” plays (fee or revenue siphoning) directed at Hyperliquid and Aster in the near future.

No conversation is complete without noting dYdX’s flop in this cycle. While dYdX was once the marquee name in decentralized derivatives with well over 66% market share, its current architecture (a Cosmos-based rollup, limited leverage, restricted markets, and less incentive velocity) failed to evolve into a threat status. dYdX never captured the kind of infrastructure-led momentum or token-alignment that Hyperliquid built. A

big part of their flop was self-inflicted, as they failed to align tokenholders and instead catered to their own profits and VCs instead of to their customers and tokenholders. Their growth stagnated; capitalization and activity flattened.. dYdX is now effectively sidelined from the top ring of perp-DEX brawlers.

So the question of who will win does matter a little, but what we know for sure is that the sector is a winner. And we’re witnessing the first true perp DEX share battle in the history of crypto.