Source: TradingView, CNBC, Bloomberg, Messari

Why Did Bitcoin Finally Go Higher?

A week ago, I tweeted the following:

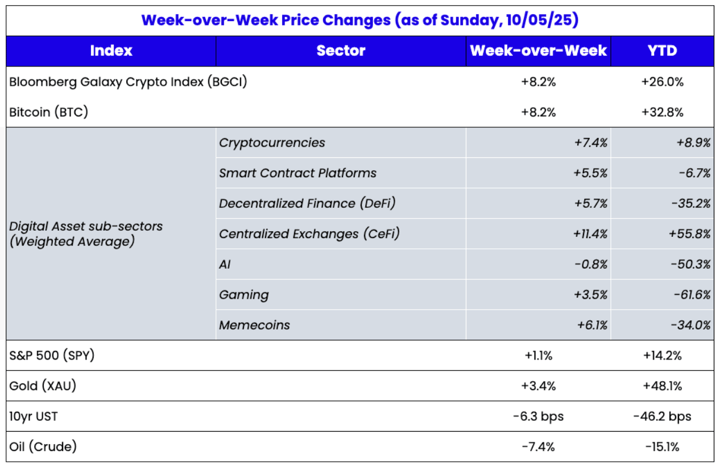

Was I right? Not entirely. Bitcoin did not rise in a vacuum. Gold also continued its march towards new all-time highs, as did equities. And many other large-cap crypto assets ascended as much or more than Bitcoin last week. So it wasn’t just a Bitcoin rally. But it’s all related to the government shutdown and other government fiascos. President Trump kicked off Wall Street’s new “debasement” trade last week after stating that the only way out of our debt spiral is to grow our way out of it, and Wall Street took that (rightfully so) as a cue that you have to own inflation-protection assets, else be left holding increasingly worthless fiat.

This isn’t a new concept. We’ve been writing for years that Bitcoin tends to rise when people lose trust in their local governments or banks, rather than when markets tank due to other risk factors. Bitcoin rose during the March 2023 regional banking crisis, the Canadian trucking standoff, the Cypress banking crisis, the 2019 Chinese tariffs, and every time the currencies of Argentina or Turkey debase. There is a common theme here – Bitcoin rises like a credit default swap when the risk of governments or banks increases.

And now we can add “Bitcoin rises when the government shuts down, and the President explicitly states that there is no way off this debt spiral train other than currency debasement”.

Cash continues to be trash.

Why I pick on Coinbase, and will continue to do so

- Robinhood (HOOD) and bulge bracket brokers will win the trading business as Wall Street eventually starts trading more tokens (HOOD stock has vastly outperformed COIN since this tweet)

- Their custody business has no moat, and is super easy to replicate from BNY Mellon, State Street, and others once regulation allows it

- Their stablecoin income (from their business development agreement with Circle) is going to zero, not just because rates are going back to 0%, but because the GENIUS Act is going to produce a ton of stablecoin competition, and the interest income is going to find its way to users, not the “banks”

- Their customers hate them

- Their acquisitions have all been flops (though I like the recent Deribit acquisition)

- Their management team makes baffling decisions (like buying back 0% coupon debt)

- Their decision to constantly support the VC community while putting zero effort into supporting secondary trading, plus an illogical/incoherent new issue listing process, and zero customer education/research on the tokens they offer

I don’t hate Coinbase. There are parts of their service offerings that we use. I think their legal team has done a great job fighting the SEC on behalf of the industry. But I stand by everything I wrote, and still believe it. Coinbase revenue and EBITDA peaked in 2021 ($7.8B and $3.3B, respectively), and haven’t come close to these numbers again, even as the stock rises. I think Coinbase, as a business, is in trouble. But Arca was never shorting COIN stock, nor do I think Coinbase is going to go away. I just think it is not a particularly well-run business, and they will struggle to grow amidst competitive pressures. Their monopoly on the U.S. is coming to an end.

I have no axe to grind with Coinbase. It wasn’t an emotional statement. It was just an investment thesis (one of hundreds we make per year).

That said, of all the things I mentioned, the last bullet point is the one that does incite some emotion from me. Coinbase continues to make the majority of its revenue from trading (still over 60% of revenue comes from trading, though that’s down from 95%), but continues to screw this business up. Even though Robinhood, Kraken, Paypal, and other U.S. venues allow some trading of crypto assets, Coinbase still has a large regulatory moat in the U.S. (for now). And as a result, I do hold Coinbase responsible for educating new crypto users, especially in the U.S. They are the face of the industry, and they have failed miserably. Not only has this held the industry back through misinformation, but it also makes my life harder, as I (and other asset managers) have to constantly re-educate investors whom the supposed leaders of the space have misled.

If you call yourself an exchange, your goal should be to list every asset and be neutral. This is not what they do.

If you call yourself a broker, then your goal should be to list/trade the best assets, help your customers make money, and write research to educate your customers. This is not what they do.

Coinbase calls itself an exchange, while listing the worst possible assets that are guaranteed to lose their customers' money (due to both poor inflationary tokenomics and a horrific listing process where they purposefully allow market makers and token issuers to price assets way too high), while pretending to be neutral even as they write research on select (terrible) assets. They are just a really really bad broker.

Many of the assets Coinbase refuses to allow its customers to trade are the best-performing assets in crypto history, and are the best examples of tokens in history. Look at the charts below of LEO, BNB, TRX and HYPE for example. All 4 have gone pretty much up and to the right since token launch, all 4 are tokens issued by other exchanges or stablecoin platforms that compete with Coinbase in some way, and all 3 have incredibly strong tokenomics (using a large part of their revenues to buyback tokens). Banks and brokerages allow you to trade their competitors’ stocks on their platforms, but Coinbase won’t let you trade their competitors’ tokens on their platform? However, to clarify, Coinbase does allow you to trade some exchange tokens. They allow you to trade Uniswap (UNI), another worthless governance token where VCs refuse to turn on a fee switch to benefit tokenholders, and Aerodrome (AERO), where Coinbase Ventures is one of the largest token holders. So again, this is a purposeful, selective process. And it is hurting their customers.

Worse, aren’t these high performing tokens the types of tokens you’d want crypto customers to be able to own? Wouldn’t you want crypto customers to learn about these quasi-equity, quasi-loyalty reward tokens instead of the predatory and inflationary L1 and L2 tokens that all go straight down as the Venture Capital investors dump on Coinbase’s retail clients? Wouldn’t you want to write research on these incredible growth stories, some of the fastest in history with billions of revenues, instead of listing and celebrating every worthless memecoin you can get your hands on to ensure that the media and TradFi continue to call this industry a laughingstock? Wouldn’t you want to help your customers understand the tokenomics, and the inflation/unlock schedules before they blindly buy tokens that are destined to go down? Wouldn’t you want your customers to make money investing in tokens, since that is, in fact, your core business model?

Apparently not.

Source: Coingecko

Recently the CEO of Bitwise wrote that more and more investors are asking about revenue as a metric for evaluating crypto assets, as if this is some sort of amazing discovery. Are you kidding me? I would have rewritten this statement as “Obviously, revenue has been, and always will be, the most important metric for investing, whether that be in stocks, bonds or crypto assets. It's downright criminal that it took so long for some crypto investors to realize this because they’ve been purposefully hoodwinked by exchanges like Coinbase, and their VC, media and influencer cronies. After all, obfuscating the truth with made-up metrics has helped fuel their business.”

Token investing has evolved, for the better. Yes, Bitcoin was the first, and it has no revenues. But Bitcoin is the biggest anomaly / smoke screen in the history of investing. Its success is miraculous, one-of-a-kind, and should not be studied or applied to literally anything else.

Yet Coinbase and others are still profiting by trying to compare everything to Bitcoin, and continue to market the horse and buggy instead of the SUV, while purposefully steering unsuspecting new crypto users and investors towards the worst assets in this industry.

It’s a shame. And I feel no regret pointing this out until it changes.