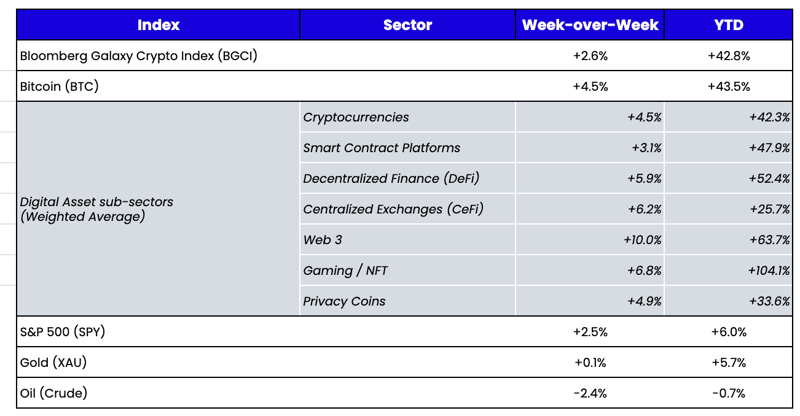

The Bottom Was Obvious. The Rally Was Harder to Predict. As measured by the Bloomberg Galaxy Crypto Index, the broader digital assets market gained for the 4th straight week. In hindsight, the bottom in December was obvious. We wrote the following on December 5th:

“I believe we’re at, or close to, a market bottom. For one, it’s incredibly hard to short right now, given lending is virtually dead and the easiest place to short futures (FTX) just short-circuited. So, the only way to really move the market lower is if a long holder of digital assets who has yet to sell everything suddenly decides now is the time to throw in the towel. Second, the macro picture is definitely changing for the best as the U.S. dollar subsides, rates retreat, growth indicators fall, and the Fed indicates rate hikes will slow. Third, there has been carnage in all asset classes this year outside of the energy sector, and there are far fewer people invested (and therefore hurt) by digital assets’ declines than those who are getting hurt by their equity, debt, and real estate allocations. This suggests we could see some new inflows in digital assets and out of other asset classes at some point. But here’s the problem with calling a bottom: there has to be a reason to go higher eventually. And that immediate bull case is much harder to see right now.”

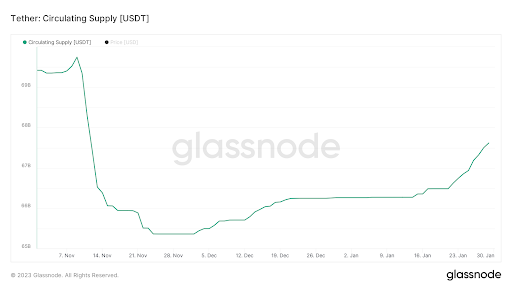

These “bottom” factors are still in play today: the macro picture continues to improve for risk assets, with the VIX approaching 2-year lows and the U.S. dollar at 9-month lows. Shorting digital assets continues to be incredibly difficult, with Binance and a few other Asian futures exchanges really the only game in town (and these exchanges are much less capital efficient than the now defunct FTX and OTC lenders were). Moreover, we are beginning to see inflows into digital assets (albeit in small, cautious sizes) and growth in stablecoin AUM, which is generally a good indicator of capital flowing into the digital assets ecosystem.

Source: Glassnode

While the bottom factors are still supportive, the “lack of a reason to rally” also still rings true. There really hasn’t been a defining moment yet to spark the massive move higher. And this may be why so many are trying to fade this strength. The 2017 rally was sparked by ICOs. The Spring 2019 rally was sparked by Facebook’s entry into a (now mothballed) stablecoin project. The 2020 rally was sparked by Covid. The 2021 rally was sparked by DeFi, stablecoin, and NFT growth. And the mid-2022 rally was sparked by the Ethereum 2.0 Merge.

Meanwhile, the 2023 rally has thus far been sparked by, um, the lack of fraud and bankruptcies? Essentially, this rally has just been a reversion to the mean, as investors closed out overly aaggressive and late shorts following the FTX collapse. Accordingly, those left on the sidelines (or worse, stuck short) are incredulous. Meanwhile, those reaping the gains are convinced that higher prices will reflexively spark rising fundamentals and user growth, thereby retroactively validating the move higher.

Until then, the “no-name” rally carries on.

DYDX Exemplifies “Good Project, Bad Token.”

In the corporate bond market, it is not uncommon for a bad company to have attractive bonds or for a good company to have very unattractive bonds. The disconnect is generally attributed to the seniority of the debt, or the covenants, which may be very favorable or unfavorable to investors regardless of the strength of the underlying issuer.

This pattern is also common in the digital assets industry. Many projects and companies with uncertain or even doomed futures create attractive tokens due to structuring investor-friendly tokenomics. But there are also plenty of very good companies and projects that lacked the willingness or the foresight to build sustainable token structures.

dYdX (DYDX) is the leading decentralized derivatives exchange with over 70% market share. A sub-sector of DeFi, decentralized derivatives are gaining market share versus their centralized counterparts,

especially in the wake of FTX’s collapse. When you find a competent team with the #1 market share in a growing sector, odds are it is a good investment.

- 100% of its revenues flow to dYdX Trading LLC—a privately held company—instead of to DYDX tokenholders

- An incredibly high inflation schedule coupled with massive upcoming unlocks from their founding team and early investors

- A governance token with no actual ability to govern, as most major decisions don’t go through the voting process, while the founding team and its handful of early equity investors (who were gifted tokens) dominate others

- Little to no transparency

- Continuous delays to their V4 upgrade, which is meant to solve some of the problems above

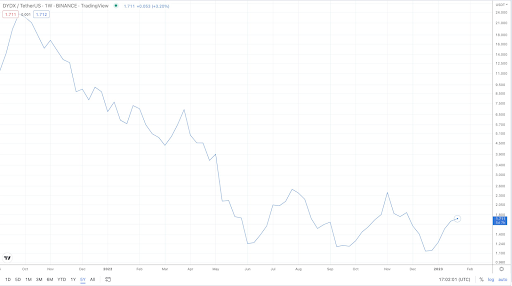

In 2021, dYdX airdropped the DYDX token to its largest users, equity holders, and founding team. It is a governance token mostly used for incentives/rewards and is most well known for its volume incentives, where the more you trade on dYdX, the more tokens you earn. Like most incentive tokens, it does its job in terms of incentivizing usage, but also creates a dynamic where there are constant sellers from those earning the token, and few (if any) buyers. The DYDX token is now down -92% from its peak (and that’s after a 110% gain YTD).

Source: TradingView

At the same time, since inception, dYdX has generated ~$378 million in revenue to the protocol. This sounds great and is truly impressive relative to so many projects in digital assets that haven’t found product-market fit. Unfortunately, all revenues flow to dYdX Trading LLC instead of to tokenholders. This is not exactly the stakeholder alignment that we’ve come to know and love in digital assets. Now, you might say, “The token didn’t promise any cash flows, so you can’t be upset.” And to some extent, that is true. On the other hand, no one forced dYdX to issue a token. In our opinion—and one that many investors in this industry share—once you issue a token, you have a responsibility to do right by your tokenholders, even if there is no explicit claim. Most projects in this space adhere to this unwritten rule; those who don’t experience a lot of pushback from their communities.

Worse, many project leaders who have already issued tokens, and the large VCs who helped them, are now hiding behind a fear of regulation as a reason not to support their already issued tokens. This is baffling—the tokens have been issued, so they already face potential opposition from regulators for unregulated sales or distributions. Simply making the already-issued token more appealing to their tokenholders doesn’t increase that risk. Taking a “throw caution to the wind” approach to issuance but a “cautious regulatory approach” to supporting it may be the worst and laziest argument we’ve seen. Either don’t issue a token in the first place or support the token you already issued. Anything in the middle is irresponsible at best and downright negligent at worst.

Further, even if you believe that dYdX will one day do the right thing, the revenue numbers for dYdX publicly displayed on Token Terminal have been reduced twice with no update from dYdX (we caught this because we were tracking it daily). The revenues accrue off chain to a privately owned vehicle and are updated manually (and inconsistently) by the team. Over the years, we’ve written extensively in favor of voluntary, public transparency; dYdX showcases the opposite. At a minimum, dYdX Trading should provide a transparency report on how this $378M in revenues is calculated and used. Is it being invested or distributed? Is it being paid out to employees/foundation members via salaries? How exactly does $378M go unreported when you have publicly available tokens, especially when the dYdX Foundation says that it values transparency? The only way to offset a token’s inflation is via growth/profits. Unfortunately, the DYDX growth/profits flow to dYdX Trading while the inflation goes to DYDX tokenholders.

Source: dYdX website

It’s worth noting that Arca is quite bullish on dYdX the business. We have previously discussed that the DYDX token would be a very attractive investment IF the team would change the tokenomics, but thus far, they continue to kick the can down the road.

DYDX Pushes Back Their Token Unlock, But Unlocks Are Gimmicks

So what has dYdX done to combat this? Instead of creating value for their token (demand side), they simply pushed back their token unlocks (supply side). Delaying unlocks drives your token price higher because it gives traders some short-term comfort. Still, in the long run, it changes nothing and proves that you can't (or won’t) generate a reason to create demand, so instead, you artificially tinker with supply. Which raises the question, why were discounts and unlocks created in the first place?

The venture capital community loves lockups for token issuances. For example, here’s a post from one of the industry’s leading venture investors defending the structure (note: Arca helped with some of the data analysis but disagrees with some of the conclusions). And, of course, they are defending it—the VCs get a massive discount in exchange for a legally binding (or in dYdX’s case, a loosely structured handshake) agreement not to sell their tokens for a specified period. While this is often pitched as “stakeholder alignment,” indicating that their investors are “long-term holders'' and won’t dump it on you, it actually creates the opposite effect. The well-known unlock dates create unnecessary overhangs and fears, creating time-based selling pressure instead of merit-based buying. As Delphi Digital wrote:

“Most (if not all) projects distribute their tokens based on a predetermined schedule, often completely unrelated to the project’s health. In certain cases, the incentive for the team and investors to continue developing and growing a project declines. One way of doing this would be by opting for milestone-based unlocks instead of time-based unlocks. The impact of the token unlocks wouldn’t change, assuming the liquidity is low or the project suffers the low-float/high FDV curse. But, it does force the team and investors to deliver before receiving their tokens. Delivering a working product would bring in more users and, by extension, more demand. This could potentially translate into a reduced impact from a token unlock. Though this solution is far from the holy grail, it would be difficult to imagine where this structure doesn’t fare better than the current structure.”

Exactly. Imagine asking any reasonably intelligent person the following question:

“Would you rather invest in an asset that creates reasons for people to buy or an asset that simply defines when people can sell?”

I’d argue that no one would pick the latter.

Those in favor of lockups may argue that the lockups help stabilize immature markets by gradually rolling out tokens to the market and reducing a supply shock. But supply shocks wouldn’t happen if you stop selling massive rounds at discounts with pre-defined selling terms, and early locked-up buyers aren’t forced to hang on to massive positions until some arbitrary “you’re allowed to sell” date occurs. Others might argue that lockups align incentives, creating an easier transition between private and public markets. That is true in the equity market, where you can only go public after achieving some level of success, thus creating new buyers due to your success, but there is no merit-based requirement for token listings. A token can become publicly traded much earlier in the lifecycle of a project, often within weeks or months of the initial private sale to VCs with a lockup. As a result, the lockup doesn’t actually create a distinction point between private and public markets. Instead, it creates an unnecessary discount to early investors who can benefit immediately from early liquidity and meritless gains.

Now, consider the opposite structure. Imagine you issue tokens to your founders, employees, and early investors with no lockups and simultaneously list your token publicly. There would be two potential outcomes: the project struggles or the project succeeds.

If the project struggles, it will fail quickly. Very few new investors will emerge, and the early investors should be able to sell their tokens for whatever value they can get—likely much lower than what they paid for them. This prevents the 2-3 year window where new investors buy into the low float, artificially inflating the price to a higher level so that the eventual unlockers can dump at a higher price. If, for some reason, the project recovers and ultimately succeeds, those new investors who did see the longer-term vision will benefit at the expense of any earlier investors who gave up on the project. Allowing early investors to sell early could benefit new investors who were able to buy at a more favorable price commensurate with the risk they were taking.

If the project succeeds with no lockups in place, free markets would entice some early investors to sell sooner at higher prices, allowing a more diverse group of investors to benefit from any further upside. It would also put pressure on companies and projects to deliver good results. A larger, more diverse ownership group seems much better than the alternative, wherein a handful of early investors and the founders own the majority of the token and every investor who bought it on the open market just fears when one of them may sell. Constant but scattered selling is much more controlled than when everyone runs for the exits at a predetermined time.

If you create incentives to buy instead of just incentives not to sell, markets function more efficiently. Hopefully, future token issuers heed this guidance. Just because “it was always done this way” doesn’t mean it is the right way to do it.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari