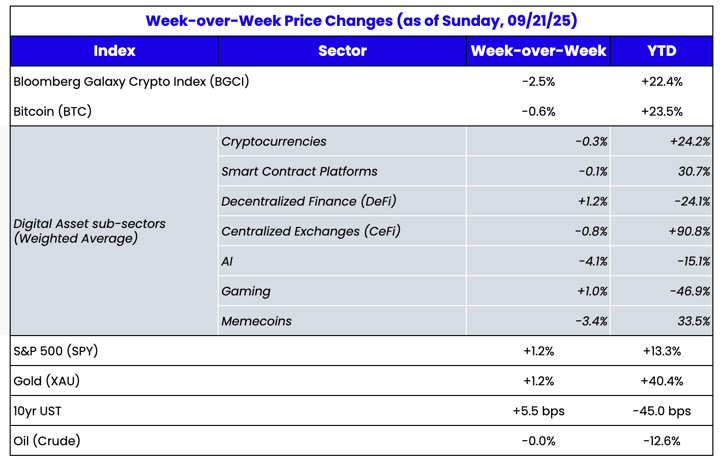

Source: TradingView, CNBC, Bloomberg, Messari

These are my opinions, not facts.

Random Thought #1: Circle (CRCL) is in trouble

The Fed cut rates 25 bps last week, as expected. As always, market participants tried to create volatility out of a Fed meeting, but continue to be thwarted by the fact that the Powell-led Fed is the most transparent in history. There are no wrinkles, there are no surprises. This isn’t Bernanke’s Fed or Greenspan’s Fed, where you’d actually go into an FOMC meeting with absolutely no idea what the outcome would be. This is the Powell Fed, where every decision is leaked weeks in advance to the WSJ (via

Nick Timiraos), and all suspense around the meeting is gone.

Still, the rate-cutting cycle has now begun, and the market is pricing in 2 more cuts before year-end, and 3 more cuts into 2026. While the suspense is gone, the outcome certainly has some effects.

For instance, Circle (CRCL) is cooked.

CRCL is currently trading at 15x LTM revenue. 100% of CRCL’s revenue comes from interest income on USDC, which currently has $75 billion in AUM, invested in short-term US Treasuries and equivalents. As such, its annual revenue falls by $187 million per 25 bps rate cut (.0025 x $75 bn). With the market pricing in 6 total cuts (including the one this week), that’s $1.13 billion of lost revenue for Circle over the next 1.5 years. At 15x earnings, that’s $17 billion in lost market cap (which would be a decline of over 50% from the current stock price).

Granted, that assumes that USDC doesn’t grow at all (it probably will). However, there is stiff competition on the horizon for USDC. The race to vertically integrate continues everywhere, as every Layer-1 protocol wants to build its own stablecoin and DEX, every successful stablecoin wants its own Layer-1 and DEX, and every successful DEX wants its own Layer-1 and DEX. For example, over $6B in USDC currently lives on Hyperliquid, but they are now creating their own stablecoin (USDH), and Solana’s reliance on USDC is causing some in the community to

ask whether they should move away from USDC as well. Not to mention, the Genius Act is likely to spark a Wall Street bank race for the creation of their own stablecoins. It’s not a coincidence that the two underwriters of the CRCL IPO, Citi and JP Morgan, immediately announced plans for their own stablecoin after seeing how easy and replicable a business model this is.

Circle certainly looks like a better company than most of the other recent crypto IPOs, which don’t even have any real revenue or earnings to lose. Still, if I were a shareholder of CRCL, I’d be very concerned about the direction of rates.

Random Thought #2: Metamask wallet token (MASK) will be a growth engine

Metamask recently announced that it would be

issuing a token (MASK). It also announced that it would soon start allowing

perpetuals trading via their wallet. Metamask claims to have 100 million users worldwide, with about 30 million monthly active users (MAUs). That’s a lot of people who will be chomping at the bit for an airdrop of tokens (and as a result, the airdrop per user will likely be pretty low). But the revenues of Metamask (via fees from trading directly from the Metamask wallet) will likely grow as a result of the wallet.

Many have questioned, “Why does a wallet provider need a token in the first place?”

It’s a valid question, but it completely misses the point. Clearly, a wallet provider does not NEED a token, as very few businesses or protocols actually do. Only a handful of Layer-1 protocols using Proof of Work or Proof of Stake actually NEED a token.

But that’s irrelevant. The old model of needing a token to secure a network has been replaced by the new model of properly using a token as a quasi-equity / rewards hybrid vehicle to grow your audience and revenues.

Binance pioneered this model using their BNB token as a quasi-equity token (receiving 20% of the profits of Binance) and a rewards token (allowing BNB holders to pay lower fees as customers of the exchange, and to use BNB as collateral for futures and options). Since then, others have improved upon this model, like Hyperliquid (HYPE) and Pump.fun (PUMP), both of which are earning over $1 billion in annualized revenues, and using over 95% of the revenues to buy back the tokens. It’s, of course, no coincidence that BNB and HYPE are two of the best-performing tokens to date (and predict that PUMP likely will be too). By giving customers tokens AND tying a customer’s success to the token’s success (via buy backs), a project can turn all customers into power users and evangelists for life, as the customers benefit from the overall company’s success (unlike say, Delta Sky Miles or Starbucks points, where top customers could not care less how the actual business performs as long as it doesn’t go out of business). Essentially, airdropping a token becomes a marketing expense, and buybacks become a way of paying them back for their loyalty and customership.

It’s not a hard concept (or at least it wouldn’t be if the exchanges, VCs, and crypto media would stop purposefully hiding this fact in order to keep the Layer-1 protocol and memecoins shenanigans flowing). The MASK token will likely follow in the footsteps of other hugely successful businesses – using a token to grow your business rather than as a necessity to run your business.

Random Thought #3: Layer-1 protocol inflation is a killer

Congrats to Solana, whose market cap has now doubled from the 2021 highs! Of course, I can’t congratulate SOL holders, because the price of SOL has gone nowhere over this same time period.

This market cap growth (2x) without SOL price growth (flat) is a function of 2 dynamics:

- SOL inflation is absurdly high, as are most Layer-1 protocol tokens. Solana’s initial inflation rate was 8% annually, and fell by around 15% per year until it hit a long-term floor of 1.5% annually – the current rate is roughly 4.5% per year. The cost to secure a network via “rewards” sounds great if you’re a blind technology buff, but if you’re a holder of SOL (or other Layer-1 tokens), it is a massive cost. It’s ironic that crypto enthusiasts constantly discuss US dollar inflation and the loss of purchasing power, yet somehow struggle to understand the damage of L1 inflation on their investments.

- Market cap is a flawed metric (which we’ve talked about A LOT). The market cap hasn’t really doubled due to the increased supply of tokens. The token count has just been blatantly and obviously stated incorrectly for most of SOL’s existence. Constant VC and Solana Foundation token unlocks have added a ton of supply to the float over the past 4 years, but if you had used Arca’s Adjusted Market Cap methodology (like everyone should because it’s common sense), then this additional supply would have already been baked into the market cap. Of course, the exchanges and data providers all know this, but their wilful ignorance has unfortunately hurt a lot of token holders who don’t understand this simple difference.

Token inflation, unlocks, and poor disclosures from exchanges and data providers are the silent killer of crypto success.

Random Thought #4: The Uniswap (UNI) token is a complete farce

Hayden Adams, founder and creator of Uniswap (UNI), has always been a little tone deaf with his public communications. But this one is truly amazing.

Yes, Uniswap, the protocol, is killing it, and is a great protocol with a great user experience.

The UNI token was one of the most successful airdrops in history, airdropping 150 million UNI tokens to anyone who had interacted with the protocol back in September 2020. Each eligible user got 400 UNI tokens, which were worth about $1400/wallet upon launch, and rose precipitously over the next few months, with the token peaking at over $40/token in May 2021.

So on the one hand, those who were airdropped tokens can’t look a gift horse in the mouth. On the other hand, unfortunately for Uniswap, the job doesn’t end after the initial airdrop. The token still exists and trades hundreds of millions of dollars per day. As such, the creators of this token have a fiduciary responsibility to support the UNI token, and on this, they are failing miserably. NONE of the revenue created by Uniswap protocol from the $1 trillion+ volumes accrues back to tokenholders. Worse, the small portion that is retained by the protocol actually goes to Uniswap Labs (the company behind the protocol, which has a different set of investors in the equity than those of UNI token holders).

The UNI token is just a complete nonsense token in today’s market, which has seen the tokens of companies that use revenues to buy back tokens grow at the expense of others that do not do the same thing. In today’s changing regulatory environment and investor demands, there is just no reasonable reason to hang token holders out to dry anymore.

There have been numerous proposals by token holders over the past few years to turn on the “fee switch”, which would turn a portion of the trading fees over to token holders, and they have all been shot down, largely by Hayden and his VC cronies, a16z. Both continue to hide behind legal and regulatory concerns, which are no longer relevant in today’s environment. The Uniswap team and its VCs are turning this token into a complete farce, and are the leading example for why DAOs don’t work.

Either turn on revenues and buybacks already, or don’t bother having a token at all. It’s that simple.

Random Thought #5: The BASE token is going to be legally very interesting

Back in 2024, I opined that Coinbase’s Layer-2 protocol, BASE, would eventually issue a BASE token to goose the struggling Coinbase (COIN) stock.

- Its Layer-2 protocol works perfectly fine without a token and

- There is seemingly no other category of tokens as out of favor, or more useless, or in less demand, than Layer-2 tokens (like ARB and OP)

A BASE token does have the potential to advance decentralization and expand creator and developer growth across the Base ecosystem. But let’s be honest… few really care about decentralization in general, and absolutely no one believes a protocol started by Coinbase is going to be decentralized.

Further, who is actually going to own this token? As I alluded to over a year ago, this protocol was built by Coinbase, and as such, I would think COIN shareholders have a legal claim to 100% of the tokens upon creation. Whether or not other lawyers will agree with me remains to be seen, but this is likely to be a lot of fun to watch play out as mutual funds who own the COIN stock will likely have to fight for the right to claim BASE tokens, as should be legally theirs, even though the BASE token will ultimately be pretty worthless like other Layer-2 tokens.

My guess is this announcement comes from Coinbase management interfering in an effort to find a way to goose the value of their COIN stock, which has lagged all other crypto stocks.

Source: TradingView

The Base protocol does have real traction, though, with rising TVL, accelerating transactions per active user, and deeper cross-chain liquidity initiatives. So it’s a good time to try this chicanery.

Source: Coinbase