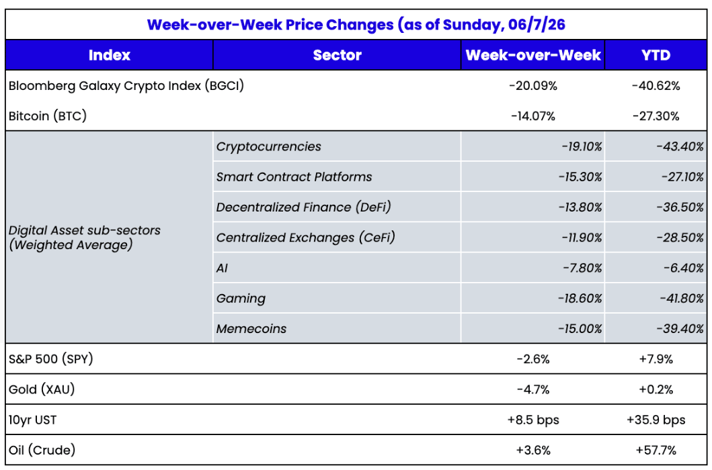

MSTR Crashed the Market

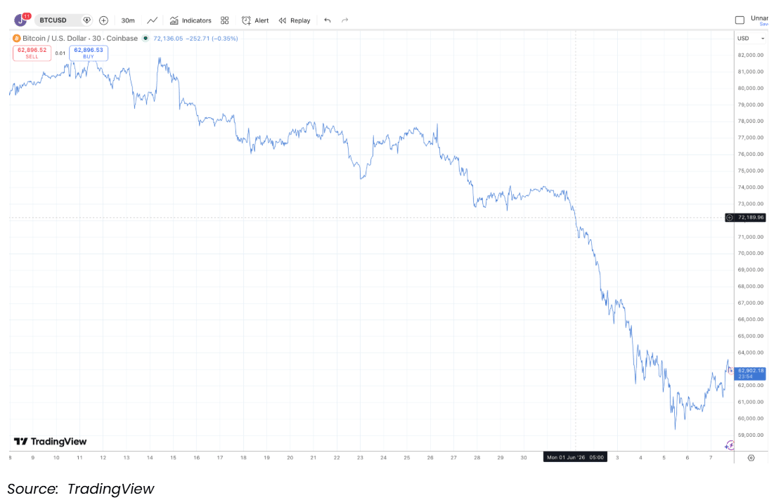

Last week’s write-up proved fairly prescient regarding Strategy (MSTR) and its first Bitcoin sale in 4 years. As expected, this news tanked the digital assets market and MSTR stock (-20%+).

MSTR only sold 32 BTC (approximately $2.5 million worth), so prices didn’t fall due to the selling pressure. Prices tanked because the market is realizing what we’ve been writing about for 3 months: that MSTR is going to need to sell way more Bitcoin in order to satisfy its preferred interest obligations.

At this point, only one scenario saves Bitcoin and MSTR in the short-term. Saylor has to come out and say (via Monday's 8K, or next Monday's 8K), that they sold $2-4 bn of MSTR and BTC, enough to cover the STRC (and other preferred) dividends for the next 2.5 years. That takes them to September 2028, when the first bond maturities come due (even though a small amount of their debt is puttable in 2027). These converts will be easy to refinance, so they won’t cause a default. The only risk is the cash dividend, and a cash buffer to cover these would be enough to calm the markets and let Bitcoin breathe.

If he does that, we believe the market would rip higher. But if MSTR does this, it also makes MSTR uninteresting for years (no longer an accumulation story, but at least not a forced seller either). STRC would probably trade back close to $100, and MSTR stock would stop nosediving. And while the capital markets might be closed to MSTR for a while, it would at least buy a ton of time, and in that time, who knows what other catalysts might pop up.

But I think we all know Saylor won’t do this, and he pretty much told the market he didn’t do this.

Source: X/Twitter

Source: X/Twitter

Saylor is basically addicted to buying Bitcoin. And that’s most likely what he will keep doing, right up until the point where he has to kill the dividend on the preferreds. If he doesn't, and he continues to just wait it out (only has 5 months of cash flow currently), or he sells tiny amounts as he goes (just enough to pay each monthly dividend), this selling pressure likely won’t stop. When the world's biggest buyer becomes a forced seller, the market will keep pressing until there is blood.

For a while last week, this selling pressure was specific to Bitcoin and MSTR only. We weren’t cheering for BTC to go lower while many other crypto assets rose or stayed flat, but we were happy to see it go lower. If BTC can move lower on its own idiosyncratic bad news without taking down the whole market, this would be yet another sign that digital asset market participants are becoming more sophisticated. This industry was historically held hostage by misinformation from the large exchanges, brokers, media members, and influencers, who failed to educate investors on the nuances and differences between different sectors and types of crypto assets. If investors can now properly assign individual risks to assets rather than blindly buying/selling the whole market, this becomes a much more investable asset class for the masses and institutions. That almost happened, but alas, Bitcoin’s underperformance proved too much, and by week’s end, most other digital assets fell as much or more than BTC.

As a result, many will try to sweep away BTC’s role in this. They will try to tell you the whole market was weak, but it just isn’t true. The selling pressure last week was clearly due to the Saylor / MSTR news despite the gaslighting from MSTR and other Bitcoin bulls. For example, Saylor himself blamed the selloff on AI, saying, “The AI buildout is absorbing capital at a historic scale, creating temporary pressure across global markets. That does not weaken Bitcoin. It strengthens the case for scarce, liquid, digital capital. Bitcoin remains the premier asset for the long term.”

That, of course, is nonsense. The growth in AI is certainly sucking capital away from all other investments, and has been for well over a year, but last week’s BTC selloff was primarily due to MSTR becoming a seller.

NYDIG also tried to blame this on other factors, saying in their weekly note to clients, “Bitcoin's recent weakness has pushed the asset back toward the February cycle lows of $60K, inciting investor questions around what’s driving the move. While no single catalyst appears sufficient to explain the decline, several narratives have emerged across macro, crypto-native, and technology markets that may be influencing sentiment, positioning, and capital flows." NYDIG then goes on to list all the other nonsense factors, including:

But the timing shows it was due to the 8-K put out by Strategy on Monday morning at 8 a.m. ET.

Saylor made a series of mistakes in the last 3 weeks (paying off 0% coupon debt with his only cash, and teasing the market with a $2.5 million BTC sale). That is why Bitcoin fell, and that is why MSTR underperformed all crypto stocks.

Prediction: Polymarket Ruined Prediction Markets

We’re big believers in the future of prediction markets. A few weeks ago, Arca even structured and participated in one of the first institutional block trades in a binary prediction market on whether the CLARITY Act would pass or not by 2027 (with coverage from Bloomberg). Fortunately, we are using Kalshi, not Polymarket, as the mark-to-market oracle.

That said, we don’t really follow most prediction markets that closely. But one particular event last week happened to be about MSTR, so we were watching it closely, like everyone else, and it turned out to be one of the dumbest, most spectacular failures we’ve ever seen.

There was a contract on Polymarket that stated: “MicroStrategy sells any Bitcoin by May 31, 2026”. Pretty cut and dry. Either YES, they sold, or NO, they did not.

In an 8-K on Monday, June 1st, MSTR indicated, without a shadow of a doubt, that MSTR did, in fact, sell BTC between May 26 and 31.

Naturally, you’d assume that this contract paid out "YES."

In reality, it paid out "NO."

Umm… what?

When the 8-K filing hit, YES shares spiked from 10% to ~80%. Then Polymarket posted “additional context” (at 1 p.m. ET Monday): “no MSTR filing, on-chain data, or credible reporting had confirmed a sale within the market’s timeframe, and confirmation achieved outside that window doesn’t qualify.” YES shares collapsed below 1c within seconds. Two NO proposals, two disputes, and 48 hours of final review later, the contract resolved NO. The YES holders, who correctly predicted the event, were wiped out. The June 30 and December 31 contracts in the same series resolved YES at ~99.9% without dispute; the entire controversy is over one deadline sitting on the wrong side of a filing date.

If the contract technically ended at midnight on May 31st, why were you still able to trade the contract after May 31? It makes no logical sense why this contract resolved "NO" in the first place, since there is no dispute that MSTR sold BTC in May, but if you want to say that "rules are rules, the contract ended on May 31 before the news was out", then the contract should not be tradable anymore after May 31.

Will Owens at Galaxy Digital said it best, in their weekly recap:

“Strip away the oracle mechanics and one fact survives: Strategy sold Bitcoin before May 31. Everyone who bought YES predicted the future correctly, and the market told them they were wrong. A prediction market is supposed to price what will happen; when resolution diverges from what actually happened, the product is merely pricing how the platform will read its own rules after the fact. That’s worthless.”

Almost $400 million was wagered on this contract. This is not just some small mistake. The Polymarket PR team is probably banking on the hopes that this egregious mistake/fraud/scam will just fade away with time. And they are probably right. The reality is, most people are selfish and only really care about things that directly affect them... so Polymarket might be right to assume this will have a short shelf life, since very few were actually negatively affected.

But this will be an interesting case study in the persistence of negative public opinion that is almost unanimously against Polymarket, the outcome, the oracle, and the UMA protocol’s voting mechanism. Polymarket equity just went from a $1 bn market cap to a $20 bn market cap almost overnight, and easily has the means to do the right thing should they choose to. It appears only a court will make them do it, though.

And That’s Our Two Satoshis!