While we still care about the token market, the investable universe continues to shrink. But blockchain continues to be one of the hottest areas of investment (alongside AI and robotics), as long as you expand the playing field beyond just tokens. While some of the crypto IPOs have been flops (see COIN, BTGO, BLSH, and GEMI), there are a few under-the-radar stocks that have caught the market’s attention.

After years of operating as one of crypto’s largest private merchant banks, Galaxy Digital (GLXY) first went public in 2018 through a reverse takeover of a Canadian shell company, which gave it a listing on the Toronto Stock Exchange Venture Exchange before graduating to the main TSX. Following a multi-year regulatory and restructuring process that included redomiciling from the Cayman Islands to Delaware, Galaxy completed its long-awaited U.S. listing on the Nasdaq in May 2025 under the ticker GLXY, joining a small group of crypto-native firms with access to both Canadian and U.S. public capital markets.

If you are unfamiliar with Galaxy Digital, it can be best understood as two separate companies under one ticker.

Stumbling Into a Gold, Bitcoin, AI Mine

Helios, the name of the HPC/AI data center site, sits in Dickens County, West Texas. When Galaxy bought it, the site was roughly 160 acres with a single 200-megawatt (MW) mining hall. Today, it is a 1,500-acre campus with a privately owned high-voltage substation, long-haul fiber engineered for roughly 10–15 milliseconds of round-trip latency to Dallas, and regulatory approval for more than 1.6 gigawatts (GW) of power.

Helios was previously built and owned by Argo Blockchain (ARBK). Argo broke ground on the buildout in July 2021. At the time, this was designed to be one of the largest immersion-cooled mining operations, and it wasn’t cheap. In 2021, total capital expenditures were $216.3 million, with nearly all of it directed to Helios infrastructure construction and the purchase of mining machines. Argo ultimately energized the first 200 MW phase in May 2022.

By December 2022, the bear market had hit. Bitcoin was down 65% YoY, and Argo was on the brink of bankruptcy. They were forced to sell Helios to Galaxy Digital for significantly less than they had invested in the facility.

The deal with Galaxy Digital was almost a distressed “Sale-Leaseback” and was structured in two parts. Galaxy bought the Helios facility and real property for $65 million and, separately, extended Argo a $35 million asset-backed loan secured by Argo’s mining machines. The sale let Argo pay down debt and avoid bankruptcy. Galaxy secured the data center and, most importantly, the initial 800 MW of ERCOT-approved power.

Weeks after the purchase in January 2023, ChatGPT reportedly reached 100 million users, kicking off the AI wave and massive demand for approved data center power.

From $65m to $4.5bn

In late 2024, Galaxy Digital informed Argo Blockchain that it would not renew its BTC mining hosting and instead hinted at a hyperscaler tenant. At the end of March 2025, it was announced that Galaxy had signed a 15-year, $4.5 billion HPC/AI hosting agreement with CoreWeave (CRWV).

The buildout guidance is as follows:

Across all phases, Galaxy guides to average annual revenue of more than $1 billion over 15 years, at roughly 90% lease-level EBITDA margins. Phase I reached its milestone in April 2026, when Galaxy delivered the first data hall to CoreWeave and began recognizing lease revenue; the full 133 MW was due online by the end of Q2 2026, with Phase II deliveries beginning in the first half of 2027.

Might be Time for a Spin-off

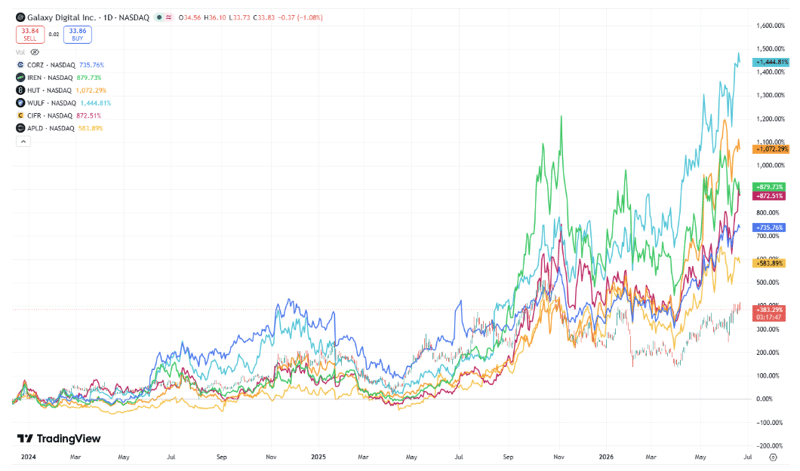

While the Helios/GLXY story is relatively compelling, the stock price has dramatically underperformed other BTC miners that have similarly signed HPC/AI contracts. Since the start of 2024, GLXY has gained +383% compared to 5-15x returns for other HPC/AI stocks.

Source: TradingView

This underperformance, in our opinion, stems from Galaxy Digital having an identity crisis. Galaxy has long been viewed as a digital asset investment bank. Prop trading, IPO underwriting, M&A for crypto equities, and asset management drove the GLXY story. This was how they were able to provide distressed financing to Argo Blockchain in the first place.

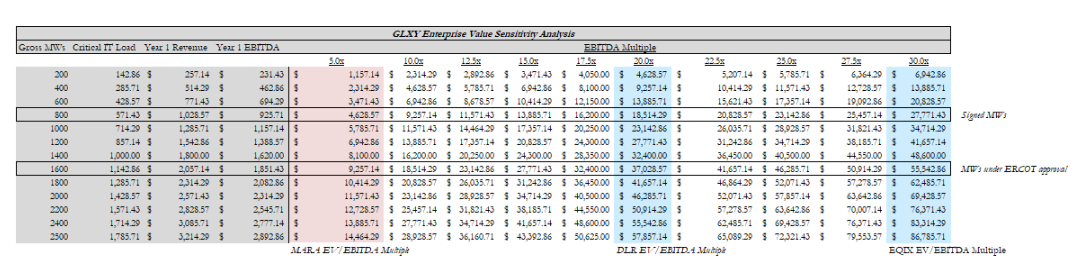

But GLXY is now an AI story, more than anything, and the back-of-the-napkin math is well known and compelling:

Source: Orange Grove Capital X

Source: Orange Grove Capital X While the valuation is compelling, the story is confusing. One can argue that GLXY should be worth north of $30 billion at data-center multiples, but it’s tethered to a historically crypto-focused business that has seasonality and volatile earnings driven by crypto activity. Given where the business sits today, it doesn’t fit into any peer set, making it a confusing story for investors and publishing equity analysts. Who should even cover GLXY? Should it be the crypto team, or the AI team, or the tech team?

However, with Phase 1 delivery expected by the end of the month, the data center/infrastructure side of the business can begin to stand on its own. This makes a spin-off more compelling to both shed the drag of depressed crypto multiples AND make it an easier story to understand for investors. I would argue that having Digital Realty (DLR) and Equinix (EQIX) as clear peers is probably better for the stock than having Coinbase (COIN) and Marathon (MARA) as peers.

Source: Internal Calcs, Rittenhouse Research

We believe the growth of blockchain is real and is happening across 4 verticals:

Finding assets whose returns may be driven by one or more of these sub-narratives for the foreseeable future is key, and GLXY might be among the best-positioned companies to benefit from all four.

And That’s Our Two Satoshis!