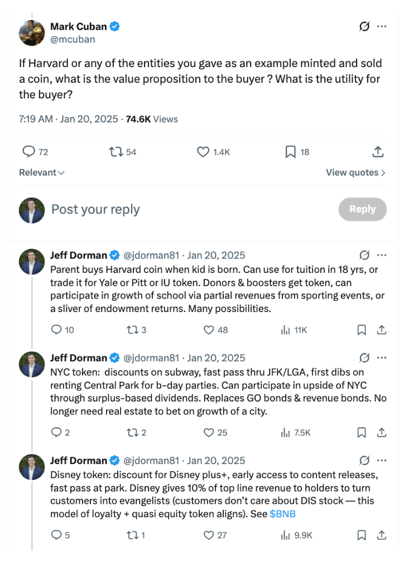

Will Other Non-Crypto Companies Issue Tokens After Seeing HYPE’s Success?

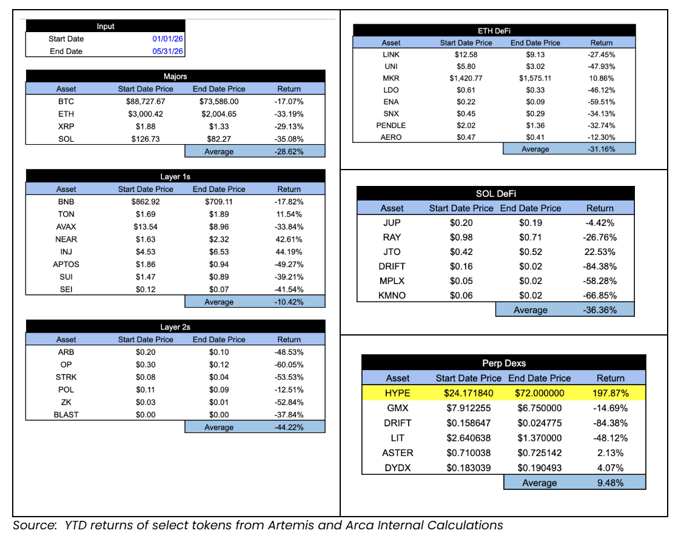

We’ve talked about Hyperliquid a lot over the past two years… more than I even remember. But when a token is up almost 200% YTD, while almost every other token and crypto stock is down YTD, it warrants talking about it again. The outperformance of HYPE is simply tremendous.

HYPE hitting all-time-highs as the rest of the crypto market does virtually nothing is a great scenario for digital asset markets. Asset classes that show dispersion and have strong rationales for price moves are simply more investable than markets that move up and down together for little reason. Having a single, strong, fundamental outperformance from one of the fastest-growing and most profitable companies in the world shows that crypto investors are becoming more discerning.

This comes as little surprise to those of us who focus almost entirely on revenue-producing token issuers with buybacks. We’re probably more surprised that it has taken so long for HYPE (and other amortizing tokens) to separate from the pack. There are only a handful of token issuers with deflationary token supplies – meaning revenues/buybacks outpace inflation/emissions/unlocks. If crypto market participants weren’t so jaded by BTC’s 1-in-a-million success and the 2021 bubble, it would seem obvious that these types of tokens would outperform inflationary tokens.

Moreover, with the advent of Hyperliquid Treasury companies (like PURR) and the recently launched HYPE ETFs, non-crypto market participants are finally becoming educated about HYPE. While many crypto-native investors are still hoping for 100x returns by throwing darts at microcap fliers with little to no value accrual mechanism, or the umpteenth L1 or L2 token, traditional investors who care about cash flows are finding HYPE to be a much easier story to understand, and far easier to underwrite as a long investment.

The problem with replicating HYPE’s success is that it isn’t easy for a crypto-startup to generate billions of dollars in revenue as quickly as Hyperliquid has, let alone do so while being entirely self-funded by its founders. While it seems obvious in retrospect that Hyperliquid’s token launch, airdrop, and tokenomics model are superior to most other tokens, that doesn’t mean other startups can necessarily do the same.

But you know who can?

Traditional, non-crypto companies that already have permanent funding and billions of dollars in cash flows. What’s stopping Disney, Netflix, Spotify, ESPN, and hundreds of other companies from issuing their own token? Tokens have proven to be, when issued correctly, like HYPE, one of the greatest capital formation and customer bootstrapping mechanisms ever created, instantly turning customers into power users and evangelists for life.

As we wrote over a year ago:

"We are on the cusp of leaving the "dot-crypto" phase of blockchain. We are about to enter a new phase where regular, 100-year-old companies use blockchain. No company is a "dot-com" anymore, because every company is, and it would make no sense to still call a company a “dot-com”. The same will be true in crypto. All of the existing crypto use cases are from crypto-native companies, but going forward, the whole world will come up with creative ways to use tokens.

Every company, university, municipality, organization, and sports team will issue REAL tokens one day (not memecoins). I call on every investment banker to help construct better tokens (or since this is unrealistic, I call on every potential token issuer to call Arca). There is a better way to do this!”

This eventuality should be even closer now that the whole world is watching HYPE.

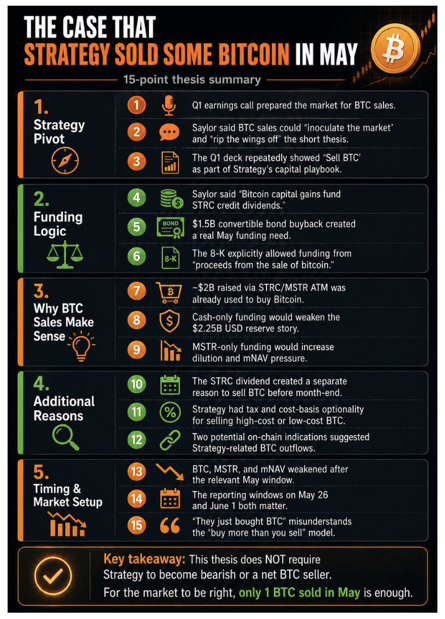

Did MSTR Sell BTC?

I’ve written a lot about Strategy (MSTR) over the years as well. While our historic view mostly centered around trying to calm markets about misinformation related to MSTR getting liquidated and being a forced seller of its Bitcoin, more recently, we’ve changed our tune as the capital structure changed (for the worse). While they will still never be forced sellers, they could become voluntary sellers, and that may even be worse.

In our opinion, the MSTR story is now pretty out of hand.

Strategy could have sat and done nothing for a long time with its old capital structure (a debt-light capital structure with no bond covenants). Strategy would have become a boring company (few BTC buys, no BTC sells), but it would at least have been sustainable while they hoped Bitcoin would rise. However, over the past year, MSTR has issued billions of dollars of preferred stock (over $15 bn), and these preferreds now carry over $1.7 bn per year in annual cash dividend obligations.

To take on this large of a cash burn, MSTR had to be thinking 1 of 2 things:

But then Bitcoin started falling, and the market grew concerned that MSTR would not be able to meet the annual cash dividend needs, so MSTR raised ~$2 bn in cash via stock sales just to ease near-term default concerns — that bought him almost 2 years of runway to pay dividends. Smart move.

Again, at this point, MSTR could have chilled for a while, and even though MSTR now has every stakeholder pinned against each other, there was at least no near-term risk. He had two years of cash cushion. Rest easy.

But then, for some unknown reason, MSTR decides to take that cash buffer and buy back the $1.5 bn 2029 maturity convertible bonds instead of using this cash to fund the annual dividends. The buyback was at a slight discount, so it's at least mildly accretive to MSTR, but this is a baffling decision for a company with annual cash flow problems. Why pay off 0% coupon debt with the only cash you have?

MSTR is now in a real predicament:

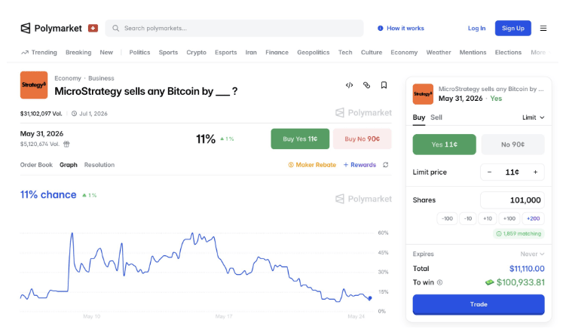

In fact, we may find out before most of you read this that he did, in fact, sell BTC this past week (which may be partially why BTC has been trading so poorly, and why ETFs have been large net sellers). On Monday, we will get the weekly update from MSTR that may tell us they sold Bitcoin last week. In fact, if you really want to go down a well-researched rabbit hole, there was a trade to make on Polymarket about when and if Saylor would sell BTC before May 31st (which, up until they bought back the converts, seemed like a long shot).

Source: Polymarket

All signs have been pointing towards this for the past two weeks.

Now, mathematically, selling BTC is no big deal. MSTR can sell a little bit every month, less than it is buying, just to satisfy the dividends. As long as Saylor is a net buyer, who cares if he sells right? But from a sentiment standpoint, how do you think the average Bitcoin investor is going to react when every major news outlet and social media influencer starts writing that “MicroStrategy is now a seller of BTC”? This company has bought over $50 bn of Bitcoin, and currently owns roughly 4% of the total 21 million outstanding. Meanwhile, the price of Bitcoin is BELOW MSTR’s average cost. Many argue that MSTR has single-handedly kept BTC afloat for years.

So when they become a seller, even if they are still a net buyer, I fear the headlines. “Buy more BTC than you sell” is a nice story, but “Saylor is selling BTC” is a terrifying headline.

We’ll likely find out more this week. But this is the first time that MSTR, Bitcoin, and MSTR preferred holders are really in a bind. One or more of these stakeholders could lose badly here, and it could be coming to a head in the next 6 months (if not sooner).

And That’s Our Two Satoshis!