Identifying an investment theme is typically the easy part. Finding the best way to express that theme via your investments is usually the harder part. One of the most rewarding parts of running a fund is when you find the best way to express a view, especially when it's a slightly unorthodox investment or uses new techniques, assets, or instruments.

As crypto fund managers for almost 8 years, we’ve had the opportunity to be first (or among the first) in many different types of investments. For example, we executed the first-ever activist campaign in crypto (Gnosis), and we were one of the first funds to invest in exchange tokens (i.e., BNB, LEO). We have also been active participants in DeFi markets, we’ve owned TradFi crypto instruments like stocks and convertible bonds (MSTR, GLXY, COIN), we’ve owned NFTs, we’ve hedged with options and futures, and we’ve executed plenty of bilateral structured trades.

That said, what we did this past week might be our most interesting trade yet.

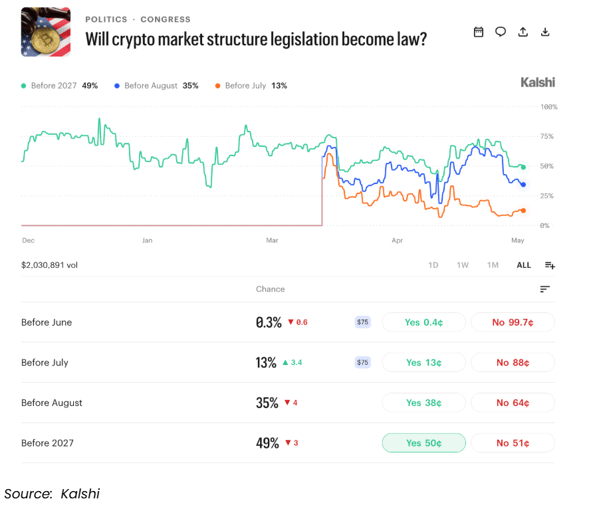

Across some of our funds, certain portfolio positions will likely be heavily impacted by whether or not the CLARITY Act is signed into law. It’s no secret that Arca is currently investing across three main themes: the growth of stablecoins and payments, DeFi, and RWA tokenization. All three of these sectors also happen to be the most sensitive to the negotiations in Washington over CLARITY. As we do with all binary events, we estimate the gains and losses that our portfolio would likely sustain upon either outcome.

While we have historically hedged our portfolio with many instruments, including BTC and ETH puts, a basket of token shorts, and even equity derivatives, these instruments have become less and less correlated with the broader crypto market. Moreover, it was clear that, in this case, hedging via prediction markets on CLARITY would be the most appropriate vehicle.

The problem, of course, is that prediction markets are still largely a retail gambling/recreational tool, and not a sophisticated institutional market. That means a fund of our size can’t execute meaningful size on most contracts directly via the platforms themselves. Others have pointed this out, but haven’t tried to solve the problem. So we reached out to our counterparties at Galaxy Digital and asked whether they could drum up some interest from potential buyers of the “CLARITY enters into law by 2027” contracts in an OTC transaction.

Ultimately, after a lot of back-and-forth and some negotiations, Galaxy took down the other side of this contract. We came up with a proper hedge ratio and made a bid on “NO.”

At the time of the trade, the contract was listed at 37 cents. Structurally, this looks very similar to a call option. If CLARITY is signed into law by 2027, we lose the entire amount (our premium), but we believe the gains in our core portfolio will be greater than this loss. Similarly, if CLARITY is not signed into law by 2027, then we will gain ~$0.63/contract, which we believe will partially (if not fully) offset the losses on our core crypto portfolio. In the meantime, the contract is marked-to-market based on the reference index on Kalshi, and either counterparty could try to close the position out at any point prior to the expiry of the contract. This was done solely as an OTC transaction via Galaxy as broker, and did not actually go through the prediction market platforms themselves. In fact, if it weren’t for this write-up, no one would even know this trade was executed, indicating that trades like this might be far superior to any traditional hedges that immediately show up on screens. The live prices indicated on Kalshi were simply used as a guide and a reference (currently, NO is trading at 50%, up +33% from our purchase price).

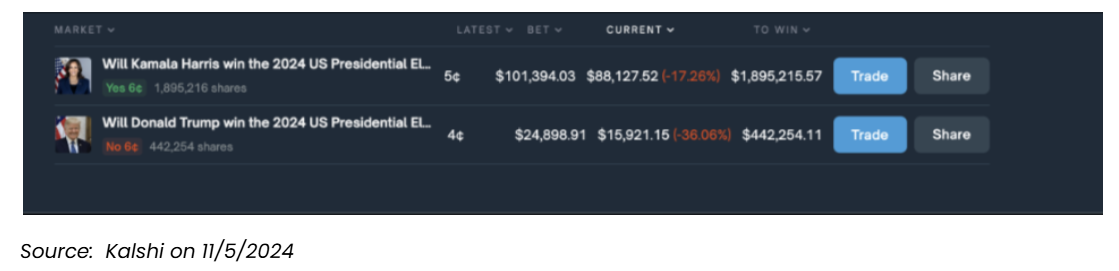

This isn’t even the first time we’ve used prediction markets as a hedge. Back in November 2024, on election night, it slowly became clear that Trump would run away with the presidential election. At the time, this was viewed very positively for crypto assets.

Late into the evening on election night, we bought “Harris Yes” and “Trump No” contracts just in case there was an unexpected shift in the election results. At the time of these trades, Kamala Harris was an 18-to-1 long shot (meaning a Harris victory would return ~18x payout). Due to how heavily traded these contracts were at the time on election night, in this case, we were able to execute directly on the screens. But we believe that was an outlier, and we think the OTC transaction via Galaxy for the CLARITY contract is more indicative of how most of these trades will be executed in the immediate future.

Like most hedges, we don’t actually think we will make money on this hedge. We believe there is a high probability that CLARITY will be signed into law by 2027, just as we believed that there was a high probability that Trump would win the election. We positioned our portfolio for both expected outcomes, and then hedged the expected outcome just in case we were wrong. Hedging is about probabilities and prices for those probabilities, not about picking the actual binary outcomes. And these prediction markets via large block OTC trades are starting to make more sense than traditional hedging instruments. In fact, this was easier, cheaper, and likely had a higher correlation to our portfolio than any crypto instrument itself.

Having worked at numerous asset management firms over the past 20+ years, I’ve been tasked throughout my career to find new and innovative ways to best express our views within the construct of our fund mandates. While these prediction market contracts are largely being viewed as toys, we found a way to make them a part of our institutional-focused fund strategy.

And That’s Our Two Satoshis!