Green Shoots

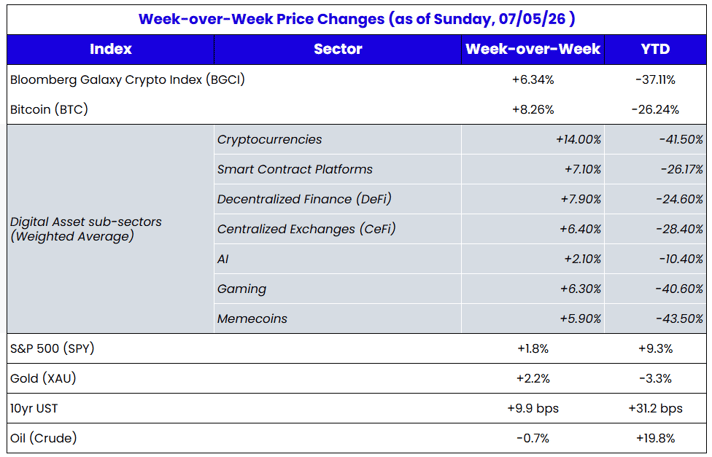

The digital asset market was due for a strong week, and it finally got one. While one week doesn’t necessarily mean anything amidst a 9-month “down only” environment, there is some reason for optimism. We’re starting to see some green shoots develop in a pretty heavy news-driven week.

Let’s review some of the positive news from MSTR and HOOD, and potentially negative news for CRCL and VVV:

For starters, Strategy (MSTR) may have finally gotten out of its own way. After weeks of downward pressure on Bitcoin, MSTR, and its preferred securities (including STRC), Strategy announced a broad overhaul of how it intends to manage its balance sheet. The company adopted a new Digital Credit Capital Framework that includes a board-approved U.S. dollar reserve policy, a revised dividend policy for its STRC preferred shares, a $1 billion authorization to repurchase preferred securities, a separate $1 billion authorization to repurchase MSTR common stock, and a formal bitcoin monetization program. Strategy also increased STRC’s annual dividend from 11.5% to 12% for future payment periods.

To support the new framework, Strategy raised more than $1 billion in cash through common stock sales, established a policy to maintain a minimum 12-month cash reserve, and increased its current cash coverage to approximately 17 months. Rather than relying solely on issuing new securities and accumulating Bitcoin, the company introduced a broader set of capital management tools to actively manage both its assets and liabilities, while providing greater flexibility in how it allocates capital going forward. MSTR and STRC rose over 15% on the news.

Strategy is now an actively managed hedge fund that can buy or sell BTC, MSTR stock, and its preferred shares at its discretion. While that may not be great given Saylor’s buying and selling track record, he at least finally did the right thing by alleviating concerns about dividend coverage. Of course, they already had the dividend coverage 6 weeks ago before foolishly buying back the $1.5 billion 2029 maturity convertible debt, which is what kick-started the whole MSTR collapse in the first place. So, I guess, congrats to Saylor for fixing the self-inflicted problem that caused a $40 billion collapse in enterprise value?

Regardless, this trade (from the short side) is now over for the time being. Those shorting BTC, MSTR, and/or STRC most likely covered (or are being greedy if they haven’t). The can has been kicked down the road for the foreseeable future. It is, for all intents and purposes, a boring story now. Whatever part of crypto’s recent decline you associate with MSTR is now behind us. Sure, cap structure trades will pop up again in the future, because again, there's no real long-term answer that satisfies all parts of the cap structure other than wishful thinking that BTC moons to $150,000+. Plus, Saylor will likely create more unforced errors at some point (like paying down the debt, or making small symbolic BTC sales, which kicked all of this off in the first place). We'll probably be doing trades for 10 years on this cap structure. But the downward spiral is over for now. And that is positive for the overall market.

For what it’s worth, it turns out people care a lot about this story. I’ve been writing and speaking about digital assets for 8 years now, and no topic has captured the broader media’s attention more than MSTR (other than Trump crypto stories). We did multiple podcasts on this story the last few weeks (here, here, here, and here), and some interviews (here and here), and I’ve probably left out a few.

Strategy wasn’t the only green shoot. Venice AI (VVV) raised $65M in a Series A financing led by Dragonfly, valuing the privacy-focused artificial intelligence platform at more than $1 billion. Venice provides users with access to more than 200 open-source AI models through a platform designed to prioritize user privacy by avoiding centralized storage of prompts and interactions. Beyond its AI platform, Venice has developed an on-chain ecosystem centered around the VVV token, which users can stake to access AI inference capacity. Unlike traditional subscription-based AI platforms, Venice uses blockchain infrastructure to tokenize access to AI compute, allowing users to own, transfer, and monetize compute resources through digital assets. The funding follows management's announcement that the company has surpassed $70M in annualized revenue while achieving profitability, highlighting growing investor interest in blockchain-enabled AI infrastructure and tokenized AI services.

While on the surface this is good news, it once again reignites the debate over equity versus token. Unsurprisingly, VVV tokens fell 15% last week.

Most crypto projects are better off choosing either equity or tokens, not both. While dual-asset structures can work in theory (as seen with Binance, which has managed to grow both its equity value and the BNB token), they often create conflicting incentives because companies have a fiduciary duty to maximize value for shareholders, which doesn’t always align with tokenholders' interests. At the same time, many projects struggle to clearly define how value should accrue to each asset, leaving tokens without a compelling economic claim while shareholders capture the benefits generated by the business.

The result is added legal complexity, governance challenges, and operational inefficiency that can outweigh any perceived advantages of having both equity and tokens. There are exceptions, particularly when a company’s off-chain business directly strengthens an on-chain protocol or when the token serves an essential function within the network, but those cases are relatively rare. For most projects, a simpler single-asset model is likely to produce better alignment, clearer value accrual, and stronger long-term outcomes.

The Venice team, of course, defended the equity raise, as did Dragonfly, while others were more objective. But the majority of crypto market participants hated the raise, as it certainly throws a wrinkle into VVV's long-term value accrual.

Elsewhere, Robinhood (HOOD) unveiled one of its biggest crypto expansions to date, launching the public mainnet of Robinhood Chain, an Ethereum Layer-2 built with Arbitrum technology, while rolling out tokenized stock trading, perpetual futures, on-chain lending, and new international markets. The company also introduced Robinhood Earn, allowing users to earn an estimated 7% APY on stablecoin deposits through Morpho, expanded its AI-powered trading capabilities, and announced launches in Canada with Singapore and the U.K. to follow. Collectively, the announcements position Robinhood as a much broader crypto-native financial platform spanning brokerage, wallet, blockchain infrastructure, lending, derivatives, and tokenized assets.

From an investment perspective, the announcements strengthen the long-term case for both Robinhood and several of its ecosystem partners. For Robinhood shareholders, the company is expanding beyond transaction-driven crypto revenue into higher-value infrastructure, lending, and global distribution while deepening customer engagement across its platform. At the same time, Robinhood’s decision to offer perpetual futures through Lighter (LIT) puts millions of Robinhood Wallet users in front of the Lighter protocol, potentially driving meaningful increases in trading volume, fees, and ecosystem activity that could ultimately benefit the LIT token as adoption grows. LIT rose +48% last week.

It’s hard to see this announcement as anything other than a positive green shoot for the market.

Finally, Circle (CRCL) shares suffered last week at the hands of a new consortium of competitors. A consortium of more than 140 financial institutions, payment companies, technology firms, and crypto companies announced the creation of Open USD (OUSD), a new dollar-backed stablecoin that will be operated by an independent entity called Open Standard. Founding partners include major names such as Visa, Mastercard, Stripe, BlackRock, BNY, Standard Chartered, Coinbase, Google, Shopify, Ripple, and Solana, with the stablecoin expected to launch later this year. Unlike traditional issuer-controlled stablecoins, OUSD will be governed by a board composed of its partner organizations.

The consortium also introduced a different economic model for the stablecoin. Participating businesses will be able to mint and redeem OUSD at no cost and without volume limits, while nearly all of the interest earned on the reserves backing the stablecoin will be distributed back to participating partners after a small management fee. Rather than concentrating governance and reserve economics with a single issuer, OUSD is designed as a shared industry-owned payments network supported by a broad coalition of banks, fintechs, payment companies, and crypto firms.

Now, there is a LOT of noise in this announcement. Companies with a single leader often fail, let alone one that is supposedly going to be run by 140 competitors. We also spoke to a few companies from the list, as a number of them are partners of Arca, and they said they never signed or agreed to anything. Either the media deeply twisted something, or the participant list is misleading. Either way, this is a big enough project to excite the masses, and while the immediate threat to Circle might be a bit overblown, it does strengthen the case that stablecoins and payments could grow 10-fold over the next few years.

Overall, this was one of the busiest and most positive weeks for digital assets this year. Blockchain continues to be one of the hottest areas of investment (alongside AI and robotics), but all of the growth in blockchain is happening in 3 distinct areas, and nowhere else:

1) Stables/Payments

2) DeFi

3) RWA Tokenization

Every chart in those 3 sectors has generally trended upward, and the positive news flow is following the charts. Notably, Bitcoin doesn't touch any of those 3 areas. SOL, ETH, XRP, and other top coins by market cap barely touch these areas either, or if they do, their tokens don't accrue much value from them. Similarly, most of the crypto IPOs have been flops (see COIN, BTGO, BLSH, and GEMI) largely because those companies don't operate or benefit from the 3 areas mentioned above (CRCL is the notable exception because it is in category 1, and new IPO Securitize (SECZ) could buck the trend as well). Of course, we’re also learning that stablecoin issuers are no longer the most important participants; instead, it’s the distribution engines that matter (see Coinbase and Hyperliquid profiting more from USDC than Circle does, and the new OUSD consortium built on distribution).

Finding the actual investments that accrue value from these areas is hard, but this past week at least provided some hope and some concrete examples. We believe most crypto professionals are now in Arca’s camp, believing that a broad-based crypto rally may never happen again and that instead it’s going to be a handful of companies and projects that capture most of the growth in blockchain.