Much Ado About Nothing

A week ago, we discussed how the macro impact on digital assets was slowly fading just as Washington’s influence intensified. Right on cue, the onslaught of government attacks continued in an otherwise slow news week.

The

SEC charged Kraken with failing to register the offer and sale of their crypto asset staking-as-a-service program. To settle the SEC’s charges, Kraken agreed to immediately cease offering or selling securities through crypto asset staking services or staking programs and pay $30 million in disgorgement, prejudgment interest, and civil penalties. A few days later, Paxos appears to be facing an SEC lawsuit over Binance USD (BUSD)—a Paxos-issued stablecoin. U.S. government officials are taking an aggressive approach to regulating digital asset participants through enforcement action. On the heels of these actions and others, Nic Carter of Castle Island Ventures wrote a provocative (albeit somewhat hyperbolic) op-ed stating that the Biden Administration is quietly trying to ban crypto using similar tactics as the controversial 2013 effort by the Obama administration called “Operation Choke Point”:

“This program, known as Operation Choke Point, operated unrestrained for years. Officials at both the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) threatened banks with regulatory pressure if they did not bend to their will. Gun and ammunition dealers, payday lenders and other businesses operating legally suddenly found banks terminating their accounts with little explanation aside from ‘regulatory pressure.’”

Carter argues that the current administration is doing something similar to the digital asset industry.

When the SEC issues a ruling, especially when Chairman Gary Gensler is taking victory laps for political gain, the common refrain is that the SEC is wrong and overreaching. Similarly, when anyone writes a negative opinion about government overreach, many in the digital asset industry rush to assume the worst.

But I’d like to offer two controversial and contrarian opinions:

- Chairman Gensler was actually right regarding the Kraken ruling.

- If “Operation Choke Point 2.0” were actually happening now (which I don’t believe it is), it would be wildly bullish for the prices of many existing tokens.

Let’s start with Gensler. SEC Chairman Gensler released a short video about Kraken’s staking product, including why it was an unregistered security offering. Despite popular opinion, I believe everything Gensler said was 100% accurate. Kraken and other exchanges and lenders in the industry—many of whom are now in bankruptcy— need to provide better disclosures. We’ve been requesting this from the service providers in this industry for years—over and over and over. In this specific case, the SEC does not appear to have an issue with staking-as-a-service itself; rather, their problem lies with the marketing and repackaging of this product. Staking does, in fact, provide a direct yield back to those staking, but when you trust an intermediary (in this case, Kraken) to pay your rewards instead of getting it directly from the source itself, there is significant risk and subjectivity.

As we've seen with BlockFi, Celsius, Voyager, and a host of others, when you pay out a yield without adequately explaining where it comes from, that yield can be a combination of marketing spend, rehypothecation, and actual rewards. If the payments can no longer be made, you can become a creditor of the intermediary rather than a token owner. In fact, Gensler even went on CNBC after the ruling and said, “Not your keys, not your crypto”— a reference to the fact that a token holder loses control of their coins/tokens when they trust a third party. Therefore, I don’t believe this is a war on staking itself. Nor is this an attempt to label all staking products as securities. Instead, this was unique to Kraken (and potentially others) that are using staking yields as part of a risky package that offers a yield to investors. Shutting this service down—and others like it—makes sense.

Naturally, others refuted this perspective. Coinbase CEO Brian Armstrong, who offers a similar staking-as-a-service product, was quick to point out that the ruling affecting Kraken does not apply to Coinbase. Whether Coinbase is next on the SEC’s list remains to be seen. Others, including the SEC’s own Commissioner Hester Peirce, pointed out the hypocrisy of asking companies to register with the SEC when it isn’t even possible. I believe Commissioner Peirce is correct in her rebuttal: independent of whether Kraken’s services were a security offering, there was no way for Kraken to register the product in the first place. This doesn’t mean Kraken's solution was kosher, but it does shed light on one of the many problems facing digital asset companies that want to be law-abiding but simply cannot under the lack of guidance and rules. Former Kraken CEO Jesse Powell

took a jab at the SEC Chairman for this reason.

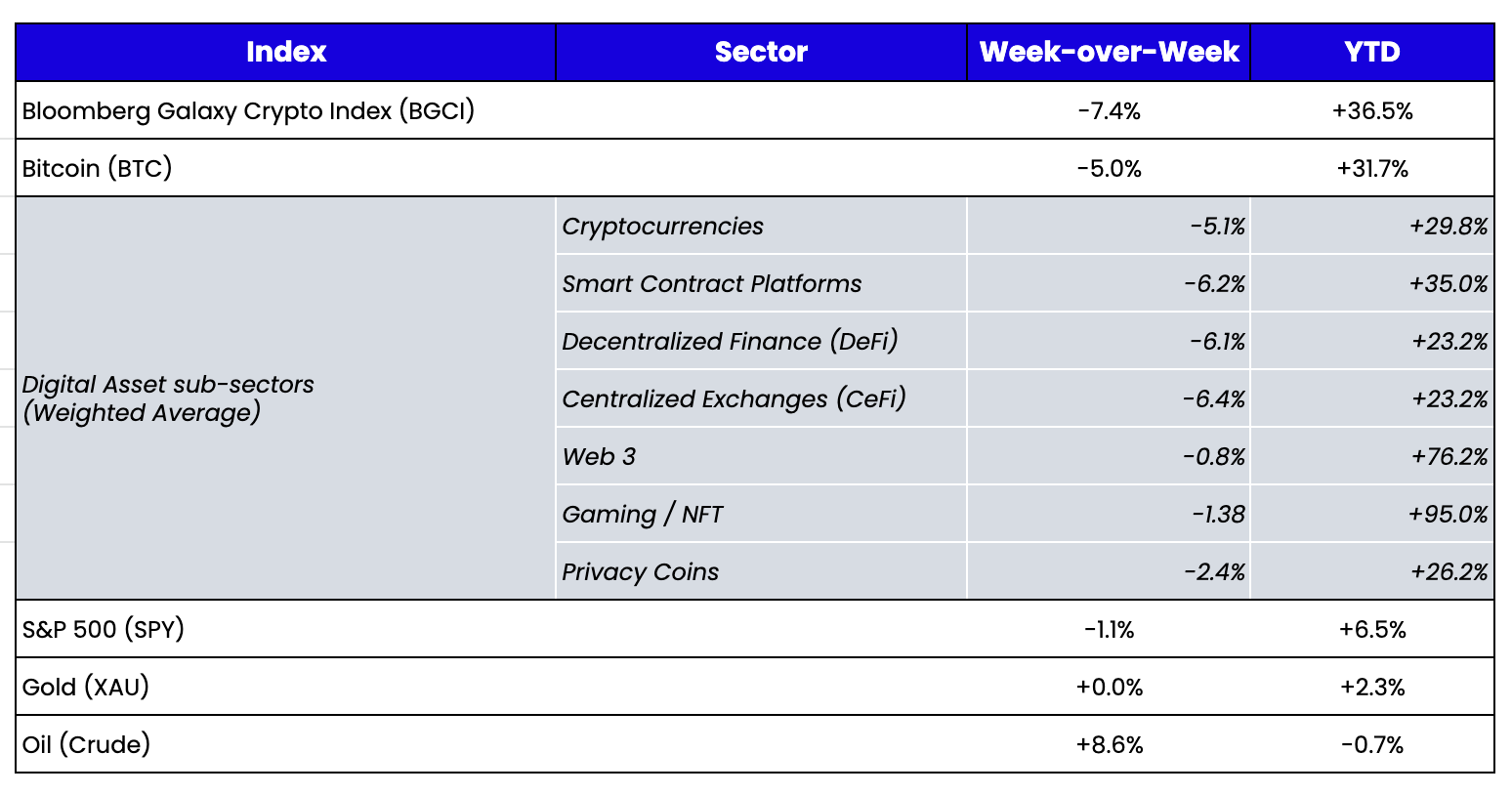

While the common narrative is that the SEC is trying to either ban staking in the U.S., or at the very least, call staking a security, the market seems to be telling another story. The 3 largest decentralized staking providers that compete with Kraken and Coinbase’s centralized services, Lido (LDO), Rocket Pool (RPL), and Frax (FXS), all saw their token prices rise last week upon the Kraken announcement. Staking itself will be just fine, as long as it is on-chain and not through an intermediary with discretion about whether or not to pay your staking rewards.

Source: TradingView

Moving on, Nic Carter’s article about the Biden administration trying to “ban crypto” by choking off the banks scared a lot of market participants. Many assumed that this crusade would be terrible for the digital asset market. As a result, prices of most digital assets began to dip last week. But in my opinion, if "Operation Choke Point 2.0” is correct, it would be very bullish for token prices.

Now, I don’t think Carter is correct in his assessment. For every anecdotal report about a bank reducing its exposure to digital assets, or a blockchain company losing its banking relationship, there are just as many anecdotal stories about new entrants to this space. Further, even if he is correct, this is a global industry, and there will always be ways to access banks and other services in other jurisdictions. But for the sake of argument, let’s assume Carter is correct and all banks become terrified to offer digital asset services. This would likely take the form of a lack of off-ramps from digital asset custodians and exchanges back to banks and an unwillingness of banks to offer redemptions of USD-backed stablecoins (like USDC).

Contrary to popular belief, I think this is a long-term problem for the industry, but it would likely provide a short-term boon for the price of existing tokens. If banks get shut out, a giant ball of money effectively gets trapped in this small ecosystem with really only one viable use case: buying more tokens.

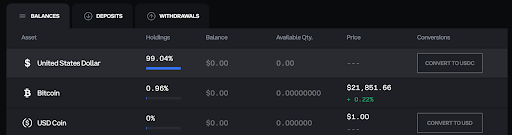

Roughly 15% of the total market cap of digital assets consists of USD-backed stablecoins (with USDT, USDC, BUSD, and DAI as the 4 largest). Stablecoins today act as 2-way assets—easy to get money into the digital asset ecosystem and an easy way to get money back out to the banking system. Coinbase, for example, allows users to push a single button to seamlessly and immediately convert USDC to USD and vice versa.

Source: Coinbase

But if a "choke point" begins to restrict users’ ability to get their money back out of this ecosystem, there will be no reason to hold stablecoins anymore. Stablecoins offer a safety net from the price volatility of digital assets but have the same peer-to-peer transfer properties of other digital assets. Suppose that price volatility shield suddenly goes away because you can no longer get your dollars back immediately. In that case, stablecoins look a lot like other tokens in terms of spendability and transferability. The faster you swap your stables into BTC, ETH, or other assets, the more likely you'll be to preserve (and grow) that value since you can no longer take it out of the ecosystem and use that money to buy stocks, real estate, or other goods. These no longer relevant stablecoins won't be redeemed per se (meaning AUM won't necessarily fall) but will likely end up predominantly owned by market makers, exchanges, and the stablecoin issuers themselves.

We’ve already seen a small example of this. When FTX was preparing for bankruptcy and halted withdrawals, many continued to trade heavily on FTX, buying tokens they wanted to own even as the rest of the market went down. The thought process was that if your money was trapped (and potentially gone forever), why not trade as much as you can and try to increase the value of your estate just in case you could one day get it out again? Similarly, any move by the Biden administration to restrict off-ramps would likely be challenged or reversed in a new administration, so increasing your estate while you wait is the logical choice.

One might argue that without adequate off-ramps, some market participants might cash out as fast as possible and leave the system altogether. Sure, some might, but remember that most people who remain in this ecosystem after the events of 2022 truly believe in the assets they own and the future of a blockchain-based society. Those who don’t really believe in DeFi, Web3, and NFTs have likely already left. And let’s also remember that most tokens are hybrids—they are part equity, part utility. The equity value can still grow (natively) without a USD off-ramp, but that value is only realized if that token has eventual utility. By limiting off-ramps, that utility has to grow much faster. For instance, very few people redeem airline miles for cash. Instead, as the airlines offer more services, those miles accrue more value because the services themselves are valuable. Similarly, a protocol, game, or entertainment company (e.g., ETH, AXS, or CHZ) could work the same way. As more services within the ecosystem are offered, the token’s utility value grows, and the need to redeem back for U.S. dollars becomes less important. Further, some have argued that if off-ramps get shut down, then on-ramps will be shut down too. But this is less likely. Users will always be able to get money into the ecosystem via gaming, investing in private funds, and even direct consumer spending via credit cards. The difficulty will always be sending money back to the “real world” via banks. As a result, all of the current cash (plus new cash) in the ecosystem will be chasing a defined and limited token investment set. Combined with the fact that the current regulatory onslaught is restricting the ability of any companies and projects to issue new tokens, we end up with a simple supply/demand imbalance.

While "Operation Choke Point 2.0" would be bad for the long-term viability and growth of the digital asset industry, it could be very good for investing in what exists today. And what exists today will likely continue to grow in monopolistic ways.

- Binance currently captures roughly 78% of centralized trading market share

- Uniswap currently captures roughly 80% of decentralized spot trading

- dYdX currently captures roughly 70% of decentralized derivative trading

- Ethereum currently captures roughly 65% of TVL

With high barriers to entry now, the kings will just keep getting bigger. So while the Biden administration may think they are killing the industry, the opposite is actually true—they are ensuring that the incumbents win, prices go higher, and services all move on-chain or offshore.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari