Much Ado About Nothing

A few years ago, I’d go weeks without logging into Bloomberg. The CRYP page contained little to no useful information about digital assets (and still doesn’t), mainstream news didn’t care much about digital assets, and, more importantly, the digital assets market didn’t care much about traditional finance. Those invested in this space didn’t care about FOMC meetings, jobs data, CPI, corporate earnings, rates, or DXY, and many prominent digital assets investors didn’t even know these events existed. A cursory glance at stocks and rates was all one needed.

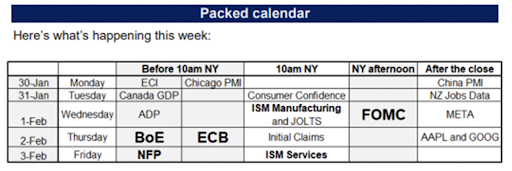

The events of 2022, of course, changed all of this. You couldn’t validate a node without having an opinion on macro. And last week, all eyes were on the economic and earnings calendar again. It was a doozy:

But ultimately, none of it mattered for digital assets investors. So it may be a while before I log back into Bloomberg again.

- The FOMC? Less hawkish.

- Large-cap earnings? Mixed and mild.

- NFP? Much stronger but mixed underlying data.

Equity indices did close the week on a down note Friday after the monthly jobs report beat expectation by a mile, stoking fears that the Fed’s rate increases may continue longer than expected. Still, it was a positive week for risk assets. And while the jobs headline number was very strong, wage growth came in line and is not accelerating, which means laborers are losing some negotiation power.

And then there is the Fed. The problem with the string of 75 bps hikes last year was that they had to slow down at some point. Now, even if the Fed raises 5 more times, the pace of rate hikes is slowing due to that aggressive front-loading last year, and that's all the market cares about—rate of change. A year ago, the market was pricing in three 25 bps hikes, and we got four 75 bps hikes instead. That’s a huge delta. But what’s the worst-case scenario now—an extra 25 bps? Yawn. Further, terminal rate doesn't matter because we all know that the Fed eventually goes the other way and cuts rates again. So there's literally nothing the Fed can do at this point to stop the animal spirits unless they pull a crazy Ivan and start hiking 50 bps and 75 bps again. The Fed did its job—it temporarily crushed demand. But that chapter is over.

With inflation cooling, the jobs market stable, and earnings thus far not a train wreck, there isn’t much to look at in macro. While many expect a massive recession and a hard landing—or at best, a soft landing—after last week’s data, they may now have to entertain the possibility that we get no landing at all (at least not this year), and the plane will just keep humming along. It appears investors will have to get used to this new environment and stop thinking in binary terms of:

- low rates and low growth = good for speculative assets

- high rates and high inflation = bad for risk assets

Instead, the market may have to get accustomed to a scenario where the economy chugs along, inflation is above target (but not at an uncomfortable level), and nominal rates are slightly higher than what we have been used to for the past 20 years, but still at very low absolute levels. This means it’s time to stop trading beta and start looking for alpha.

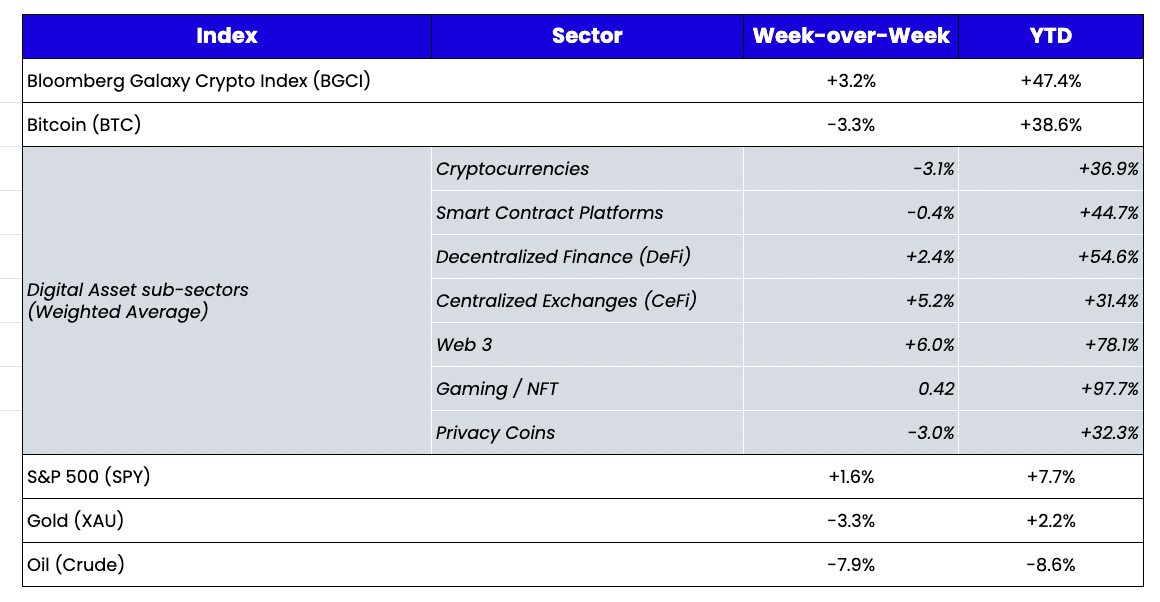

And that’s exactly what is happening in digital assets land. As Cumberland pointed out in an internal note to their clients, there has been a renewed interest in thematic investing. Optimism (OP) traded above $3 this weekend after starting the year at $1, hitting all-time highs as Layer 2s on Ethereum continue to take market share. Render (RNDR) is now up over 300% YTD after a new tokenomics model passed. dYdX (DYDX) is up about 200% after pushing back an investor lock and offering more transparency following Arca’s public campaign. LIDO (LDO) is up over 100% ahead of the Shanghai fork. In each of these tokens, Cumberland noted that it has traded more volume OTC in 2023 than they did in the entire second half of 2022. And each of these tokens—plus many others—has moved higher due to themes emerging or idiosyncratic catalysts. “Token picking” is back in vogue, and that was not the case in December or even in most of the 2nd half of last year, when trading was entirely dictated by general "risk on/risk off" price.

Washington Policy Is Coming to a Head

Instead of admitting mistakes or wrongdoing, Congress is sitting back and watching other government bodies light fires to cover their tracks. If you can’t join ‘em, beat ‘em!

For instance, last week, the Federal Reserve released a policy statement further limiting digital asset activities by member banks. A few weeks earlier, the Federal Reserve, Office of the Comptroller of the Currency (OCC), and Federal Depository Insurance Corporation (FDIC) issued a joint statement questioning the “safety and soundness” of digital asset activities and discouraged banks from being involved in the sector. The letter told banks to limit the portion of their businesses consisting of digital assets and/or related activities. It basically prohibited national banks from issuing or holding digital assets stored on public blockchains.

Meanwhile, the SEC continues its crusade to regulate by enforcement. However, SEC Commissioner Hester Peirce remains a lone voice for regulation by guidance. A few years ago, Peirce laid out what was, in my opinion, the first logical guidance on token issuance, granting a 3-year safe harbor for issuers who needed to start centralized but could meet certain milestones on their path towards decentralization. The beauty of this simple idea was that it would encourage issuance and experimentation rather than the current stalemate and offshore tinkering, which has led to monopolies and stifled innovation. Perce joined Arca’s Finance on the Blockchain conference last year to discuss the factors shaping the regulatory environment for digital asset securities.

A few weeks ago, Peirce was at it again, this time in a speech at a Duke conference, where Peirce again laid out constructive suggestions on how to move the space forward. While it is worth a full read, there were a few highlights:

“The first and most important lesson of the evening for people who believe in crypto’s future is that they should not wait for regulators to fix the problems that bubbled to the surface in 2022. They can act themselves to root out harmful practices and encourage good behavior. Regulatory solutions, which tend to be inflexible, should be a last resort, not a first resort. People working together voluntarily are much better at fixing things than regulators using their inherently coercive power to impose mandatory solutions. Moreover, private solutions avoid the systemic risk that comes from an industry homogenizing because everyone has to fit into the same regulatory parameters.”

This is a refreshing take that Arca believes strongly in. We have been on the offensive numerous times over the past few years, trying to demand transparency via both the court of public appeal and via formal governance of protocols like Gnosis, Sushiswap, and dYdX. We will continue to encourage others to do the same.

“Second, remember the point of crypto. It is not driving up crypto prices so that you can dump your tokens on someone else. Digital assets need to trade, so centralized venues or decentralized exchange protocols are necessary, but trading markets are not the ultimate point. Rather, at its core, crypto is about solving a trust problem: how can you interact and transact safely with people you do not know. Traditionally, people have looked to centralized intermediaries or government to solve this problem, but technology like cryptography, blockchain, and zero-knowledge proofs offer new solutions. Out of these technologies flows a multitude of potential uses, including smart contracts, payments, provenance, identity, recordkeeping, data storage, prediction markets, tokenization of assets, and borderless human collaboration.”

While Peirce’s influence at the SEC is quite neutered, her guidance is still refreshing. And despite the public campaigns from certain SEC officials who seem to care more about political advancement than technological progress, Pierce’s perspective is consistent with how many regulators feel about the growth of blockchain technology.

“Invoking the Howey Supreme Court case, which fleshed out the investment contract subcategory of securities, we repeat the mantra that all, or virtually all, tokens are securities. As one commenter has argued, functionally the ‘most important’ factor of the Howey test is an SEC-invented ‘fifth shadow factor’: whether the SEC wants to regulate the asset. The SEC wants to regulate crypto assets.”

No problems here. Feel free to call every token a security. Contrary to popular belief, there is nothing illegal about something being a security. But when you do, lower the barriers and costs of registration, grandfather all existing DEXs and exchanges as they work to get licensed, and allow for ICOs and other fast and easy sale and distribution mechanisms. If the SEC wants to own this space, it should do it without mimicking existing Wall Street rules that have not adapted to technology and changing investor habits.

“Mainstream regulated institutions are experimenting to see whether cryptography and blockchain technology can make existing processes cheaper, faster, safer, and more efficient. But a regulatory model that effectively forces all innovation into regulated entities is not likely to foster the kind of dynamism that will broadly benefit society. Last year was so brutal for crypto that some people want to relegate it to the dustbin of failed experiments. Rather than swiping left on crypto, we should remember that new technologies sometimes take a long time to find their footing. What kind of country would we have if regulators prohibited people from experimenting with technologies that other people think are stupid or meaningless or even ones that could cause harm? Our country is built on a presumption that people are best able to choose for themselves.”

That alone should be enough to realize that the path we’re on is not working. So here’s hoping members of Congress read Commissioner Peirce’s speech instead of simply trying to run away from their SBF and FTX linkages.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari