What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

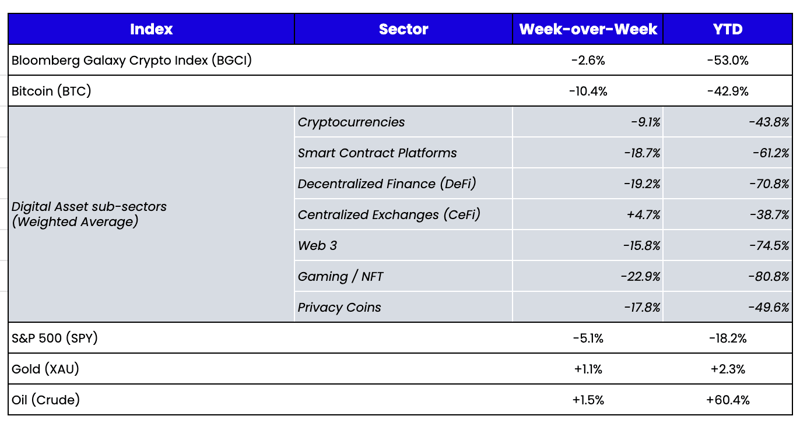

Week-over-Week Price Changes (as of Sunday, 6/12/22)

Source: TradingView, CNBC, Bloomberg, Messari

Lido’s Staked ETH (stETH) in the Market’s Crosshairs

It’s gone from bad to worse in financial markets.

- The Consumer Price Index rose to a new high, rising +8.6% YoY, driving all assets lower once again last week.

- The 2-year Treasury sold off 24 bps to 3.065% (the highest level since 2008), and the 10-year Treasury yield rose 12 bps to 3.165%. The odds of a 75bps increase for the June meeting went from 9% on Thursday to 27% on Friday post the CPI data.

- The High Yield Index (HYG) fell -1.7% on Friday.

- The Dow Jones Industrial Average has been down 10 out of the last 11 weeks, which is the first time since the Great Depression.

- Digital assets are in a free-fall and have now erased over an entire year’s worth of gains, falling below early 2021 prices.

- U.S. average gas prices crossed $5 for the first time last week, with gas now +63% on the year and +112% since Biden took office last January, which has led to the President’s approval rating sinking to new lows.

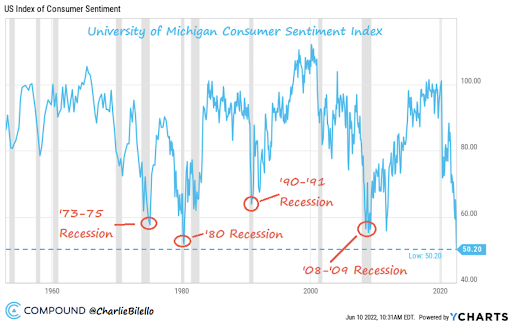

The University of Michigan Consumer Sentiment index fell to 50.2 from 58.4—the lowest ever, dating back to the 1952 launch of the sentiment index.

The macro environment is bad and not getting any better. As a result, there is little to no support when bad news breaks in digital assets, and we’ve seen a string of negative news in the past two months. The latest? Another depegging, only this time it is a different variety than what we saw with LUNA and UST a month ago.

There are different types of arbitrage and asset-backed relationships. For example, stablecoins like USDC and USDT (assuming you trust that the assets truly are backed 1:1) will always converge eventually if the market price trades below the value of the collateral, with any discounts reflecting uncertainty of that backing or liquidity concerns. This is not only because it’s 1:1 backed, but because there is an actual redemption mechanism, similar to an ETF, which can be created/redeemed to close any price arbitrage. This is much different than an algorithmic stablecoin where there is no explicit backing, which is why an asset like UST can depeg indefinitely (or why a regional bank used to suffer large depositor losses before FDIC insurance).

Assets that are explicitly backed by another asset will eventually converge as long as there is a mechanism to force convergence. Therefore, any discount to fair value is essentially the same as pricing a 0% coupon bond. For example, the Grayscale Bitcoin Trust (GBTC) is explicitly backed 1:1 by BTC, but GBTC trades at over a 30% discount to the value of that BTC. Similarly, Nexus Mutual (NXM) tokens are explicitly backed by the ETH that Nexus holds in its Capital Pool, but wrapped Nexus (wNXM) tokens currently trade at a 57% discount to the collateral backing it. Neither GBTC nor wNXM has a defined timeline for when or how you will force this conversion, so the yield (inherent in the discount) reflects that perceived timeline. If GBTC converts to an ETF in three years, the 30% discount is the market’s way of saying that the yield required for a 3-year zero coupon bond with no liquidity is 10% per year. For wNXM, perhaps it is 2 years and an annual yield closer to 30% per annum. These arbs will eventually close because the backing is explicit, but the discount can persist as long as there is illiquidity and/or uncertainty on when and how you can force conversion.

This past week we saw another example of a “depegging”—which seems to be mystifying the market. Lido is a liquid staking solution that, amongst other things, allows you to stake ETH on the Beacon Chain ahead of the upcoming ETH 2.0 merge. Once Ethereum completes its merge (meaning the protocol converts from Proof-of-Work to Proof-of-Stake), any ETH staked to the network along with ETH staking rewards will become liquid. But until that happens, Lido offers you a token called Staked ETH (stETH) in return for your ETH, which is an IOU fully backed by ETH but not redeemable for ETH until after the merge happens. Recently, stETH has been trading at a growing discount to ETH. As our friends at Galaxy Digital wrote, this discount could be for a number of reasons, including merge execution risk, validator slashing risk, and Lido-specific smart contract risks. In addition, there remains continued uncertainty around when exactly stETH will become redeemable for staked ETH given that withdrawals are not currently enabled on the Beacon Chain, nor will they be until at minimum 6 months after mainnet Merge activation.

No big deal in normal markets. Staked ETH is definitely 100% backed by ETH, despite many misconceptions (a good summary of what is actually happening here), and there is some level of yield on the “zero-coupon bond” that would be worth the risk. But this is not a normal market anymore—collateral values are shrinking, market liquidity is drying up, and lenders are struggling and pulling back. Thus, something that should be no big deal suddenly becomes a big deal, and the yield required to entice an investor to own a “zero-coupon bond” like this is going up. The price of stETH can deviate quite a bit from ETH, even if the peg itself is still fully intact. And when that happens, trouble ensues since stETH is a token that can also be used as collateral for other loans. Said another way, a non-event suddenly becomes an event if cascading liquidations occur due to the temporary de-peg. And as stETH goes down, arbitrageurs buy stETH and short ETH against it, sending ETH lower, which again lowers collateral values across DeFi. Add in the news overnight that Celsius is pausing withdrawals, partially due to stETH losses and the lack of liquidity, which turned them into forced sellers of other assets to meet redemptions (though this has less to do with stETH and more to do with the fact that Celsius and other lenders are just unregulated hedge funds that have to put up gates if withdrawals/redemptions come too fast).

This too shall pass, and it will again be a case study of whether or not we want to live in a fake world like TradFi where all problems are immediately “fixed” with Too Big to Fail bailouts, or if we want to live in a new regime where these relationships will eventually work themselves out—but many will suffer pain as it plays out. The answer is probably somewhere in between.

But make no mistake about it—there is nothing wrong with the peg or the mechanism of stETH vs ETH. There is, however, a lot wrong right now with liquidity, confidence, and leverage in the system.

Inflation and Rates STILL Don’t Really Matter for Digital Assets in the Long Run

Digital assets are nothing without narratives. Right now, the defining narrative is that digital assets are the riskiest assets, and all risk assets are going down because of the Fed’s tightening and subsequent recession.

But it’s worth going back in time to rehash old narratives and how they did or did not pan out. For example, was there anyone who had “digital assets will be lower because of inflation and rising rates” on their 2020 and 2021 investment risk factors? Nope. In fact, it was the exact opposite. Paul Tudor Jones’ now-famous inflation post from exactly two years ago in May 2020 looks completely wrong. The entire thesis was that inflation would get out of control (check), and the solution was to:

- Buy gold (marginal gains)

- Buy the Nasdaq 100 (worked well initially but obviously not at all a solution today)

- Buy Treasury steepeners (not working at all)

- Buy Bitcoin (worked initially but obviously not at all a solution today)

So how did smart investors get the call (inflation) so right, but the solution so wrong? And how did a consensus trade two years ago (that inflation was good for stocks and digital assets) suddenly become an opposite consensus trade (that inflation is bad for stocks and digital assets)? I asked my colleague Nick Hotz—former macro analyst and the author of a great article from a year ago discussing how digital assets have historically acted during different economic regimes—why this time is different. Nick’s response:

“For the past decade, stagflation was always positive for bonds, gold, and tech on a relative basis because it always meant growth was slowing faster than inflation was rising. Rising rates usually meant growth and inflation were rising, which is a great environment for stocks. This time is different because inflation is rising much faster than growth is slowing, which has crushed bonds and meant less of a change for real yields (falling real yields are positive for tech and gold) since the Fed had to tighten faster to deal with inflation. With respect to Paul Tudor Jones’ investments, steepeners are an explicit bet on positive growth and positive inflation without tightening monetary policy (rising front end), and the rest of his ideas were explicit bets on falling real rates. Usually, that means stagflation. However, real rates haven't fallen; they've actually risen due to tightening policy, and rising real yields crush all assets—the riskiest assets most. Many put on the same stagflationary playbook in December/January that has worked over the past decade, but the money made on the "growth slowing" portion of the book got completely offset by losses in bonds. The biggest misconception for the market was the extent to which inflation would get out of hand.”

So now we know why prices are down for almost all assets. But at some point, when the rate of change and missed expectations slow, we will be back to a core question: do higher nominal rates actually matter? I think digital assets will eventually outperform other assets in a higher rate environment. Rising rates affect valuations, cost of goods, and cost of capital—none of which has any real impact on most blockchain companies and projects:

1) Valuations – when rates rise, it affects discounted cash flows in a typical DCF model and comparable comps to alternatives like fixed income. Tech companies are historically “fat tail assets,” meaning most of the value comes from the expected cash flows way into the future (the fat tail). This means the terminal value of a DCF model has the highest impact on valuation, and when that terminal value goes down due to lower present value math caused by rising rates, so does the valuation. But many digital assets have no cash flows (like Layer 1 smart contract protocols, for example); thus, the terminal value either doesn’t exist or would be unaffected by rising rates. You could argue that digital assets have no value to begin with if you want, but it is difficult to argue that the valuation decreases because of rising rates (Bitcoin being the exception—gold has a ~0.9 correlation with 10-year real yields because the value of store of value assets is solely affected by the cost of money in the future, and Bitcoin should behave similarly).

2) Inflated Cost of Goods – Inflation affects the cost of goods/rent/employee salaries and all other costs a company bears. For blockchain-based companies, only employee salaries really matter. Most don’t have offices or rent, and most have no actual input costs or physical goods. As such, these projects and companies are largely unaffected by rising costs.

3) Cost of capital – In a rising rate environment, the cost of capital increases, making it difficult for companies to refinance their debt or finance high ROI projects. While cost of capital can definitely impact certain blockchain-based sectors like DeFi since higher rates make speculative trading and borrowing less attractive, most other blockchain-based projects don’t have liquidity issues (well-funded via token sales), don’t have to refinance debt at higher yields, and have no risk of bankruptcy since the protocols themselves run on their own. The recent Luna 2.0 relaunch we wrote about last week demonstrates how hard it is to actually kill a blockchain project. Essentially, blockchain protocols can’t file bankruptcy, and thus, cost of capital barely impacts their business, if at all.

Moreover, as we’ve discussed previously, many digital assets are hybrid instruments that are both part financial instrument (quasi-stocks) and part loyalty/member reward benefit. The latter is completely unaffected by a recession.

Eventually, we’ll have a new narrative to trade on besides just macro, but ultimately, we are undoubtedly going to remain in a higher yield world (at least for a while). Therefore, it’s important to realize which assets actually lose value versus those that are simply offered at lower prices.

What We’re Reading This Week