What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

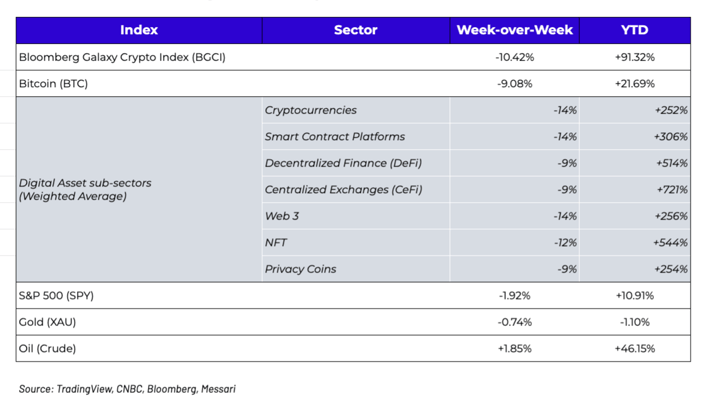

Week-over-Week Price Changes (as of Sunday, 6/20/21)

The Fed and Digital Assets

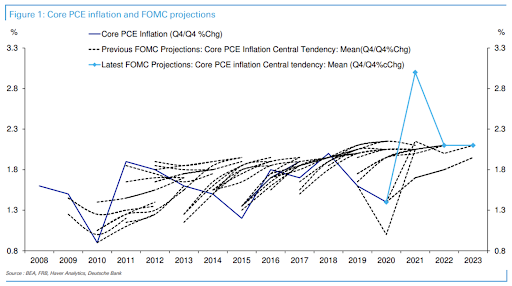

This was one of the most uneventful weeks of the year for digital assets Looking back on the news flow and the price action, there was very little worth discussing, which is a bit odd given this past week was also “FOMC week” and digital assets fell ~10%. Many market participants called this the most important FOMC meeting and press conferences of the past decade, though from a purely objective perspective, it was a rather neutral outcome. Powell continued to speak to the transitory nature of inflation, and inflation targets across the committee barely changed. But this is the era of signaling, and Powell’s shift to “The Fed would begin talking about tapering” from “The Fed will talk about talking about tapering” was enough to change the market’s outlook even though it is like that nothing material happens until 2023. And as Deutsche Bank pointed out, “it has been nearly impossible to predict inflation even in a period where it has been low and stable. The below chart shows the Fed’s projections over the last decade relative to what actually happened. Clearly they have generally over estimated inflation (as have most people). This shows how volatile rate expectations could become if the data changes. These are not automatic “carry and forget” times.”

Source: Deutsche Bank

That said, the slightly more hawkish stance roiled public markets. After three consecutive weeks of gains, US stocks reversed course and had their worst week since January. The VIX climbed +32%, and the Treasury curve flattened by 11 bps. The US Dollar rose +1.8%, its largest weekly gain since April 2020, while commodities had their worst week since March 2020. Meanwhile, digital assets once again fell across the board, the 5th decline in the past 6 weeks, with high correlations and few noteworthy drivers of price outside of macro.

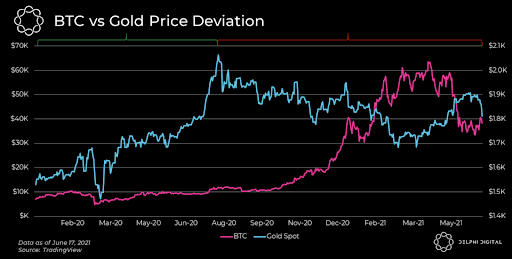

The irony here is that many look to digital assets as an escape from traditional markets, and yet here we all were glued to CNBC looking for clues from the largest central bank. In some ways, perhaps this is indicative of an asset class growing up, while in other ways it was a stark reminder of how powerless all markets are when it comes to monetary policy. But do these clues actually matter long-term? In some ways, absolutely. The low dollar, low rate environment has been positive for all risk assets, including digital assets. But in other ways the week-to-week price action has proven to be meaningless. We’ve talked about the spurious correlations between digital assets and other assets many times, most notably back in September 2020 when digital assets broke away from the herd shortly after another FOMC meeting. For example, at that time, all anyone could talk about was Bitcoin’s correlation to gold, but since then, the two assets couldn’t be less correlated (and at times, are even negatively correlated). So on the one hand, Fed-driven market reactions are less than ideal for an asset class that is meant to be driven by customer engagement and stakeholder coordination. But on the other hand, it’s always worth remembering that correlations in this new asset are definitely not set in stone.

Source: Delphi Digital

Source: Delphi Digital

A Long-term versus Short-Term View

So where should we look for clues? For starters, we can look at the private markets versus the public markets. Most digital assets are now down 50% or more from mid-May highs, leverage and speculation have basically been wiped clean, and the fear and greed index has been hovering near all-time lows. Coinbase’s retail app has dropped from #1 on the IOS app store in mid-May, to 125th today. That’s a pretty good indication of how short-term expectations have changed quickly to the downside.

In stark contrast, however, money continues to flow into the private markets, with many deals pricing at higher valuations than where they were priced just a few months ago. The past week alone saw a variety of newly funded digital assets projects, even as publicly-traded digital assets suffered uniform 10% week-over-week declines. These include (list courtesy of Galaxy Digital):

- BitDAO raised $230m in a private funding round led by Peter Thiel, Dragonfly Capital, Pantera

- Bitwise raised $70m in a Series B led by Elad Gil and Electric Capital

- TRM Labs raised $14m in a Series A funding led by Bessemer Venture Partners

- Lending protocol Goldfinch completed an $11m raise led by a16z

- Yield Guild Games raised $4m in a Series A funding round led by BITKRAFT Ventures

- Decentralized exchange dYdX raised a $65m Series C led by Paradigm

- InstaDapp raised $10m in a funding round led by Standard Crypto

- DeFi derivatives platform SynFutures raised a $14m Series A led by Polychain Capital

- Solana received $314m led by a16z and Polychain Capital

- Amber Group raises $100mm led by Chinese investment firm China Renaissance

Investor appetite remains very strong, as new entrants to the market are choosing to fund private companies and projects as a form of capturing beta to the market. This is another way of saying the shape of the curve has changed, with steep contango (future prices) but lower spot prices. In other words, it’s signaling that the market expects prices to go higher in the long-term regardless of near-term price action.

We’ve seen this toggle before -- as new investors seem to switch focus between Bitcoin and Ethereum, between currencies and DeFi, between public and private, and between digital assets and crypto stocks. All of these instruments are various proxies for the growth of this asset class.

Just like with the Fed, the end result is spelled out, but the path it takes to get their changes.

What’s Driving Token Prices?

- BTC (-9%) - Bitcoin has recently been faced with some challenging circumstances. Chinese hash rate will drop significantly as China is regulating and suspending miners. Lower hash rate typically means lower price yet BTC’s network security isn’t a going concern. There’s also an argument that hashrate moving out of China is a net positive as miners are going to be more distributed across the globe. There has been much talk of the “death cross” as BTC 50 day moving average crosses below its 200 day moving average, yet there is no statistical evidence as this event being a sell signal.

- MATIC (-6%) - Iron Finance, a partially collateralized stablecoin project on Polygon, suffered a bank run which sent its native TITAN token to zero. It had a peak of $2.3B locked, or around 1/6the the total TVL of Polygon at its peak before the issue. UMA announced scaling on Polygon and Polygon more than doubled liquidity incentives on Aave over the next 7 months.

- RLY (+26%) Rally was mentioned on the Today Show about influencers and the creator economy. Rally is an open network that allows creators to launch vibrant and independent economies within their communities powered by the ethereum blockchain. This publicity contributed to a solid week’s performance for RLY.

- UNI (-17%) Founder Hayden Adams tweeted that Uniswap has surpassed $300B in total volumes. Uniswap is the first decentralized exchange (DEX) to post such massive volumes which is also very promising for other DEX’s.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency