"You only have control of three things in your life: the thoughts you think, the images you visualize, and the actions you take." - Jack Canfield.

Recently, we have collectively experienced a global disruption. The Covid pandemic has stretched our medical, social, and economic structures to their breaking point. But it is often out of times of great stress that tremendous growth occurs.

THINK

The pandemic was a powerful catalyst, causing many to look at the world through a new lens. Now that we are emerging on the other side, what changes will prevail? One apparent long-lasting change is the ascent of digital assets and the rush of certain institutions to embrace them in some form or another.

As recently as the beginning of 2020, major financial institutions were still questioning the validity of digital assets. Now, incumbent financial players are launching their own digital asset initiatives with new announcements coming on a regular basis. Bank of New York Mellon and Morgan Stanley are the newest banking giants to take a seat at the Bitcoin table. Energized by the digitalization revolution, BNY has announced plans to custody Bitcoin and other cryptocurrencies, and Morgan Stanley has filed with the SEC to add Bitcoin exposure to 12 of its mutual funds’ investment strategies. The increased use of digital tools during quarantine spurred behavioral changes such as increased digital adoption, changes in mobility patterns, and modifications to personal finance. These noticeable habit changes have caused financial institutions to address the digital assets market and develop meaningful, adaptive customer and business solutions.

Financial institutional adoption of digital assets has been talked about for years, with many false starts, but now, filings have been submitted to regulators and real dollars deployed. With established financial participation comes money, industry validation, and friendly competition. The present attraction and enactment were triggered at least in part by the successes of early adopter companies, like ourselves, who already identified the potential business advantages and built products designed to meet the standards of traditional investors. The path has been conveniently paved for financial institutions to now support the latest needs of their customers.

VISUALIZE

A corporation’s primary purpose is to create value for its customers and themselves. Thirteen years after the Bitcoin whitepaper was published, and after countless institutional firms’ claims that digital assets were fraudulent (Jamie Dimon in 2017), a scheme (Bill Harris in 2018), or worthless (Warren Buffet in 2020), institutions now crave a piece of the pie. So how big is the pie?

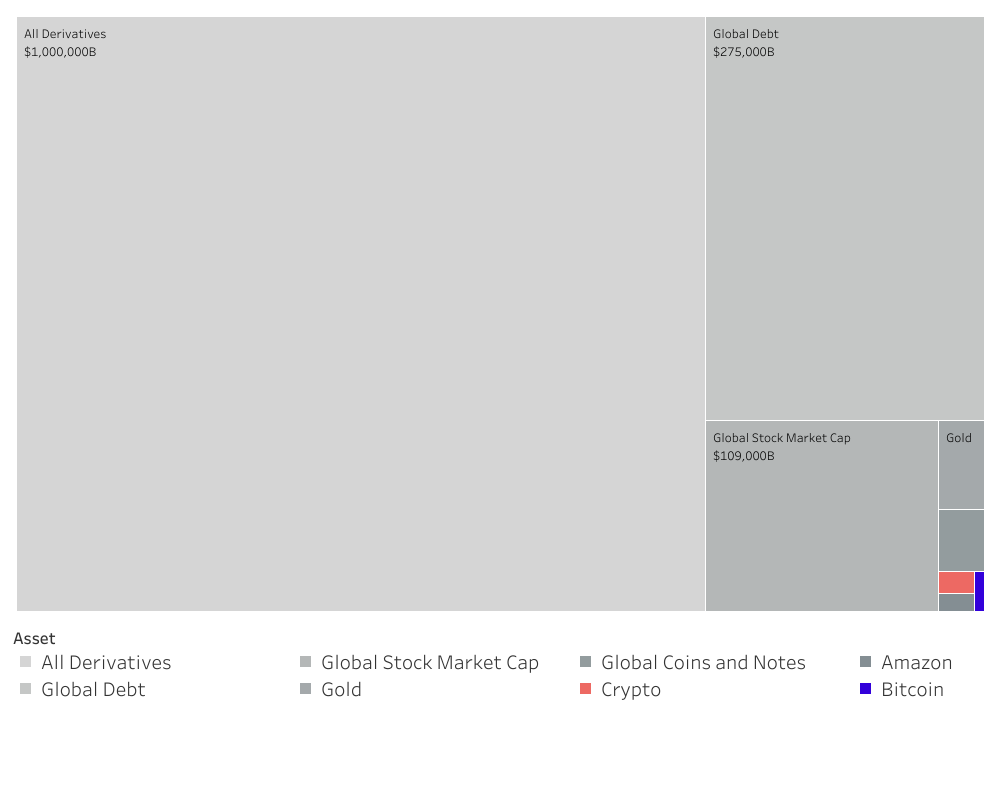

When envisioning the current size of the digital assets market and its potential value, it is difficult to conceptualize because of the enormous size and complex nature of the existing financial system. Digital assets are potentially disruptive to other financial assets. As illustrated in the above chart, the blue box represents Bitcoin today, the pink, the entire digital asset ecosystem - even combined they are almost invisible when compared to the market cap of all stocks. They are an even smaller fraction of global and a rounding error when compared to the notional value of all derivatives.

Yet, it is still quite remarkable how far the digital assets market has come, especially when compared to other transformative financial products and markets. In the early 2000s, I co-founded WisdomTree, an investment pioneer for ETFs. At that point, approximately 13 years after ETFs were created, the asset class was ~ $40B and has since grown to become an $8T industry today. Let’s interpret this comparison.

- ETFs are solving a particular need in the market - liquidity and tax efficiencies; while digital assets are addressing integrated, fundamental obstacles inherent to the financial system.

- ETFs are a single financial instrument and, in my opinion, have a sliver of the disruptive power that cryptocurrencies, decentralized finance, Web 3.0, smart contracts and the larger digital assets ecosystem carries.

- ETFs took ~13 years to get to ~$40 billion market capitalization, while digital assets have a $2 trillion market capitalization after 13 years of existence.

Either ETFs took a long time to permeate the financial ecosystem, or digital assets have a seemingly greater unrealized market potential. With a little over a decade under our belt, we are far beyond the “Will this survive?” point and, as we see it, have approached the, “How big will it become?” phase.

I believe we are on the precipice of a transformation comparable in scope to the internet revolution. The internet made information ubiquitous, free, and frictionless; digital assets arguably are doing the same thing with value. Also, beyond the technological revolution, the internet stimulated cultural, economic, and political change. It modernized how and why people communicate, business productivity and growth, information dissemination, and freedom of knowledge exploration.

ACT

The rise of digital assets resembles the internet metamorphosis; technology-driven upheaval of archaic systems and development of new behavior. At times like these, it’s imperative to have real agents of change driving the transformation for the benefit of all. It is for this reason that companies like Apple and General Electric exist. During these turbulent times, the public relies on companies like Arca to help them navigate these uncharted waters. But it is also in these times that value can be accrued by the knowledgeable and the bold. The words of Shakespeare’s Brutus come to mind:

“There is a tide in the affairs of men,

Which taken at the flood, leads on to fortune.

Omitted, all the voyage of their life is bound in shallows and in miseries.

On such a full sea are we now afloat.

And we must take the current when it serves, or lose our ventures.”

To learn more or talk to us about investing in digital assets and cryptocurrency