What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

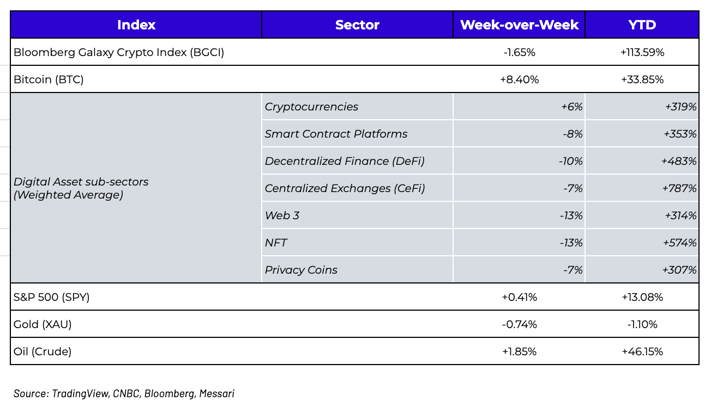

Week-over-Week Price Changes (as of Sunday, 6/14/21)

This Week’s Blog:

- Inflation and the macro setup for Digital Assets

- Bitcoin has been boring this year, but not last week

- DeFi risk is overblown due to recent regulatory misinterpretations

Inflation is Probably Transitory

We’re going to get into the inaccurate DeFi reporting that sent DeFi down 10% last week, but let’s start with Bitcoin and inflation. Even though the majority of digital assets have nothing to do with money or cryptocurrency, most investors begin their journey with Bitcoin, and therefore have strong views on inflation. So when the index of US consumer prices (CPI) rose at a 5.0% annual rate in May, the steepest increase since 2008, I had to do a double-take when I saw that both Bitcoin, gold and the 10-year US Treasury have basically gone nowhere this year compared to equities, commodities and other digital assets. In fact, of the 100 digital assets with over $500 million in market cap, only 8 other assets have performed worse than Bitcoin YTD. It’s clear that growth assets with fundamentals have trumped narrative-driven “inflation hedges”.

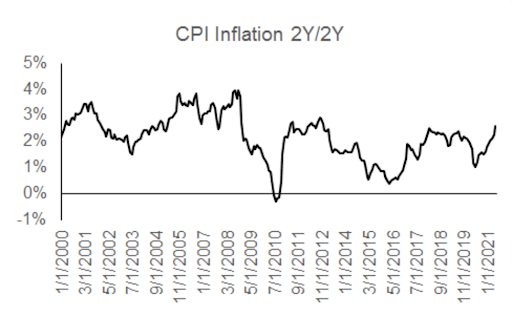

But there is probably a good reason for that. While the CPI headline is flashy, it means basically nothing. Those who already thought inflation is running rampant will feel validated by the number, while those who think it’s transitory have plenty of reasons to believe that is still the case. The steep increase is being boosted by comparisons with relatively low inflation a year ago, when the pandemic depressed prices. Yes, it was the highest year-over-year change since 2008, but did anyone look at the graph after 2008? Hint, inflation fell, a lot. And therein lies the problem with year-over-year comparisons following depressed levels after a near depression.

Arca intern-extraordinaire and former macro analyst, Nick Hotz, prefers to look at the annualized 2Y/2Y CPI reading, which gets rid of YoY denominator issues… looking at this chart, inflation is rising, but it’s nothing to get too concerned about yet.

Source: Arca Internal Estimates

Like most subjective arguments, everyone has a self-serving view, but no one actually knows what the future will hold. What we do know is that, despite this inflation spike, prices of US government bonds surged to their best week in over a year, pushing yields down for the fourth consecutive week to the lowest levels in more than three months. And that means we are right back to where we were last year, with a great macro setup for equities, real estate and digital assets:

- The Federal Reserve's balance sheet is printing new all-time highs

- Rates are low and the US dollar is declining

- The equity volatility index (VIX) is back to post Covid lows

So why is Bitcoin stuck in the mud?

Bitcoin is Back (Kind of)!

We haven’t talked much about Bitcoin this year because it really has been boring from an investment standpoint. Bitcoin is a binary call option -- it’s either worth essentially zero (doubtful), or it’s worth a lot more than it is worth today (most likely), and each data point along the way simply speeds up or slows down the inevitable. During the last few months, most of these narratives have been deflating -- from Elon Musk turning Bitcoin into a misreported ESG circus, to the China mining crackdown, to unemotional non-cult freethinking macro traders taking profits at the expense of leveraged retail gamblers. Bitcoin has even lost its “safe haven” status within digital assets itself. Whereas Bitcoin used to keep pace with rallies and outperform downturns, for the first time in years, Bitcoin now has poor up capture and poor down capture (meaning Bitcoin rallies less than other digital assets on the way up, but sells off just as much or more on the way down). All of these factors have turned investors against Bitcoin, with the pendulum swinging from “Bitcoin is the most crowded long trade in the first quarter” according to a Bank of America sentiment survey, to “everyone now hates Bitcoin” according to a new Goldman Sachs survey.

But this past week may have finally flipped that script. There has been a confluence of positive data points that may speed up the ultimate maturity of that call option:

- El Salvador adopted Bitcoin as legal tender, and while there is a lot to unpack here, it further solidifies the battleground that will be “Bitcoin versus governments”

- Microstrategy pulled off a heist, raising $500 million of secured debt with loose covenants to potentially purchase Bitcoin

- Bitcoin miners signaled approval for Taproot, a software update that adds privacy, programmability and data efficiency features, paving the way for activation in November.

- The US Department of Justice (DOJ) seized Bitcoin from ransomware attackers, and while some may question how they did this, the important takeaway is that Bitcoin is a terrible medium for criminal activity given how easy it is to track transactions.

Perhaps more importantly, some of the regulatory fears that have plagued digital assets since inception, began to subside this week:

- The G7 summit concluded and the communique didn't focus much on digital assets other than a brief comment on ransomware. In fact, according to FTX, the "Future Frontiers" section (beginning on bullet point 31) was actually quite positive on embracing digital innovation.

- In the US, digital assets did not even show up in the SEC's summer objectives

- The Bank for International Settlements (BIS) released a consultative document proposing a prudential framework for bank exposure to digital assets. At the highest level, BIS proposed a two-tier construct: (1) certain tokenized assets and stablecoins would be treated in accordance with the existing capital framework; and (2) other types of crypto exposures such as Bitcoin would face a 1,250% risk-weighting for other types of exposure such as Bitcoin. According to Compass Point, this release should be viewed as an early step in what will be a lengthy road from international concept to domestic rule. It is far too early in the process to pontificate on final structure, potential exemptions, or the ultimate capital charge.

As Jonathan Cheesman at FTX recently wrote, “Regulation fears and uncertainty are top of mind, particularly for institutional investors thinking of entering the space.” For Bitcoin, these fears have been dialed back a bit, or at least have been pushed out, but for Decentralized Finance (DeFi), the irrational fears have picked right back up. It’s bad enough when those inside the digital assets community incorrectly lead new investors astray about DeFi, but it's even worse when regulatory overhang is completely misinterpreted and misreported by the press. For more, we’ll turn it over to Arca Managing Director, Peter Hans, who ran a Washington Policy Research firm (Height Analytics) prior to joining Arca.

DeFi is Not Illegal, and other Nonsense Narratives Rebuffed

[Written by Arca Managing Director Peter Hans]

CTFC Commissioner, Dan Berkovitz, spoke on Tuesday June 8th in a keynote speech at the FIA and SIFMA, Asset Management Derivatives Forum 2021. For those unfamiliar with the acronyms, these are trade associations representing member centralized brokerage, banking and investment firms. The transcript of the remarks, available on the CFTC’s webpage, were then “reported” on by Coindesk with a click-bait headline along the lines of ‘DeFi may be illegal.’

Regulation across digital assets is a major overhang, and broad confusion around headlines only adds fuel to the fire of uncertainty. Regulation of digital assets, centralized exchanges, custodians, investment banking/issuance and AML/KYC are inevitable. My hope is that this inevitability is in the near-term, but I’m not holding my breath as the SEC and CFTC are still very much in discovery mode with more pressing priorities in front of the administration.

Despite this, we feel that it’s important to address the portion of the speech that wasn’t understood in the Coindesk article as well as share some thoughts on the potential interests of the relevant regulators.

First, let’s look at who gave the remarks and who he gave them to. Dan Berkovitz is coming under scrutiny for citing Wikipedia and a “google search” to define DeFi, and rightfully so. That said, Berkovitz was the General Counsel for CFTC when current SEC Commissioner, Gary Gensler, was in charge. The two remain close, and given Gensler’s stance on consumer protection and the need to regulate, it’s clear where priorities will eventually fall. However, this was a keynote speech at a lobbyist event representing special interest groups from traditional banking and finance. The audience was therefore CFTC-regulated entities who are interested in preserving the status quo, and the CFTC is interested in enforcing the status quo, where appropriate from a jurisdictional and feasibility perspective. So one not only has to consider the source, but the context that the source is delivering the remarks.

This does not mean that Commissioner Berkovitz is placating the audience and delivering exaggerated remarks. If one reads the transcript, everything he says is accurate:

- Peer-to-peer systems do not offer the same regulatory consumer protections as centralized regulated intermediaries. This is an accurate statement.

- We have a system in which intermediaries are legally accountable for protecting consumer funds. In a pure DeFi system, there is no intermediary to monitor markets for fraud, manipulation etc. This is also accurate, but the reason why it’s accurate is because there is no intermediary entity at all. An entity can’t, by definition, commit fraud or market manipulation if there is no entity.

- This next section is likely where Coindesk got its sensationalist take: “Not only do I think unlicensed DeFi markets for derivative instruments are a bad idea, I also do not see how they are legal under the CEA.” The CEA is the Commodities Exchange Act, and I think it’s safe to assume that Commissioner Berkovitz understands the regulations and enforcement authority under the law. So then why is DeFi “allowed to operate” in the US if the entire space is operating illegally under the CEA?

The fact of the matter is that DeFi is not “operating illegally,” and the Coindesk article is, at best, click bait. However, DeFi, and digital assets more broadly, is something that US regulators are watching carefully, and this is a very good thing for the continued growth and development of the asset class. Commissioner Berovitz’s closing remarks were as follows:

“...we should not permit DeFi to become an unregulated shadow financial market in direct competition with regulated markets. The CFTC, together with other regulators, need to focus more attention to this growing area of concern and address regulatory violations appropriately.”

I’m a huge proponent of DeFi, and I can’t argue with any of the logic behind those two statements. Yes, regulators are watching DeFi, as they are watching the entire digital assets ecosystem, but right now there is no statutory authority for the CFTC nor the SEC, and Congress remains highly unlikely to pass a bill that changes that. Further, these comments, and the CEA, very specifically cover commodities and futures markets. At best, this is a small subset of the DeFi universe, and many of the tokens in the Defi sector that have sold off on these comments and associated fears (the majority of DeFi) are very overtly outside of the jurisdiction of the CFTC. Additionally, as it pertains to DeFi vs CeFi, there is no ‘entity’ that could be causing consumer harm, and by definition, no ‘entity’ to “go after.” Note, that this is consistent with the SEC’s viewpoint that a decentralized protocol cannot be in violation of an unregistered security offering since there is no centralized beneficiary. In that same vein, while there might be consumers who are normally the victims of fraud or malfeasance, there is no entity that is even capable of committing those violations. This is why the Commissioner highlights the “concerns” and the “risks,” but of course he isn’t going to highlight the benefits in front of a centralized banking special interest group that he was asked to keynote for!

It should be increasingly obvious that Commissioner Berkovitz knew exactly what he was doing when he cited a “google search” as the research into DeFi. One only needs to look back a couple of months to see how much knowledge the CFTC does have, especially through its Technology Advisory Committee (TAC). You can access a detailed presentation on DeFi on the CFTC website here, which presents a much more objective view as to the growing landscape, risks and benefits. Especially when analyzing regulatory/political outcomes, one must first start with context and motivations, then one can move to the many dominos that need to fall for various scenarios to play out.

Finally, it’s very important to remember that there is no regulatory framework governing crypto, digital assets nor centralized intermediaries. This is the regulatory framework that is necessary, and likely a 2022 event, at best. Given that, there is certainly no regulatory framework nor authority of the broad DeFi space. Nor is there an idea of how it could be enforced if it existed.

Over the next 12-18 months, we will continue to see political posturing and headlines. We will continue to face risks associated with uncertainty, especially when those risks are highlighted in venues of political theatre. But like any other asset class, the ability to navigate uncertainty effectively is what creates long-term opportunity. We continue to see regulation of digital assets in the US as a long-term positive catalyst, but one that remains an overhang of uncertainty for the foreseeable future.

We think the risks to DeFi, however, are significantly overblown and have been taken well out of context in the Coindesk article.

What’s Driving Token Prices?

- CHZ (+10%) - Chiliz announced the first Brazilian soccer team to sign up for Socios (Atletico Mineiro) and conducted an FTO for the Argentinian National Team which sold out in two minutes and raised $1.2m from 17k users. CHZ also released a new feature called "Socio Predictor" where users can guess the outcome of matches and earn points in return. The points are used as raffle tickets to award prizes to users which include VIP experiences or more fan tokens.

- BNB (-10%) - Wei Zhou, the chief finance officer at Binance, has left the company, according to a spokesperson at the biggest crypto exchange by trading volume, after having worked there for nearly three years. Additionally, India's financial crime division opened an investigation into WazirX, the Indian crypto exchange owned by Binance.

- HXRO (-7%) - When Wall Street issues digital asset research it gets noticed. BTIG published a write up on HXRO: “Leveraging Solana Blockchain, HXRO Network Poised to Enhance Market Liquidity on DeFi’s Next Major Frontier – Options – Through Smart AMM (automated market makers) Protocols.” As Wall Street investment banks continue to adopt digital assets, research like this will become the norm and not the exception. HXRO is a decentralized derivatives network being built on the Solana blockchain that will provide the infrastructure for a fully functional decentralized exchange for vanilla, exotic and pari-mutuel options markets.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

'