What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?

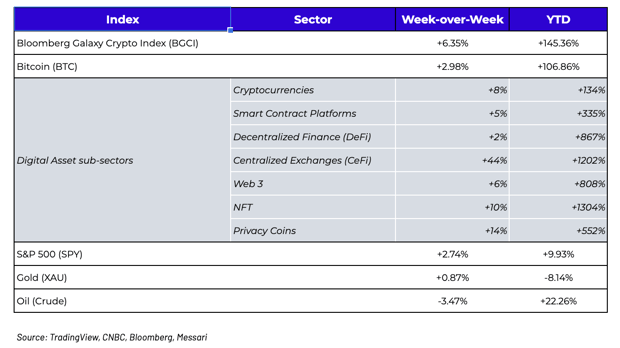

Week-over-Week Price Changes (as of Sunday, 4/11/21)

Coinbase (COIN) stock is coming

- Q1 revenue of $1.8 billion vs. $1.3 billion for all of 2020

- Q1 net income of $730 million vs. $322 million for all of 2020

- Q1 adjusted EBITDA of $1.1 billion vs. $527 million for all of 2020

- Monthly transacting users (MTUs) of 6.1 million vs. 2.8 million for all of 2020

Now, take a look at the table on the top of the page with week-over-week price changes for digital assets. You may have noticed one sub-sector as an outlier. Centralized Exchange tokens (CeFi) rose 44% on average, and are now up 1,202% on average since the beginning of the year.

Select CeFi tokens and their YTD price moves.png?width=667&name=unnamed%20(96).png)

Source: Messari

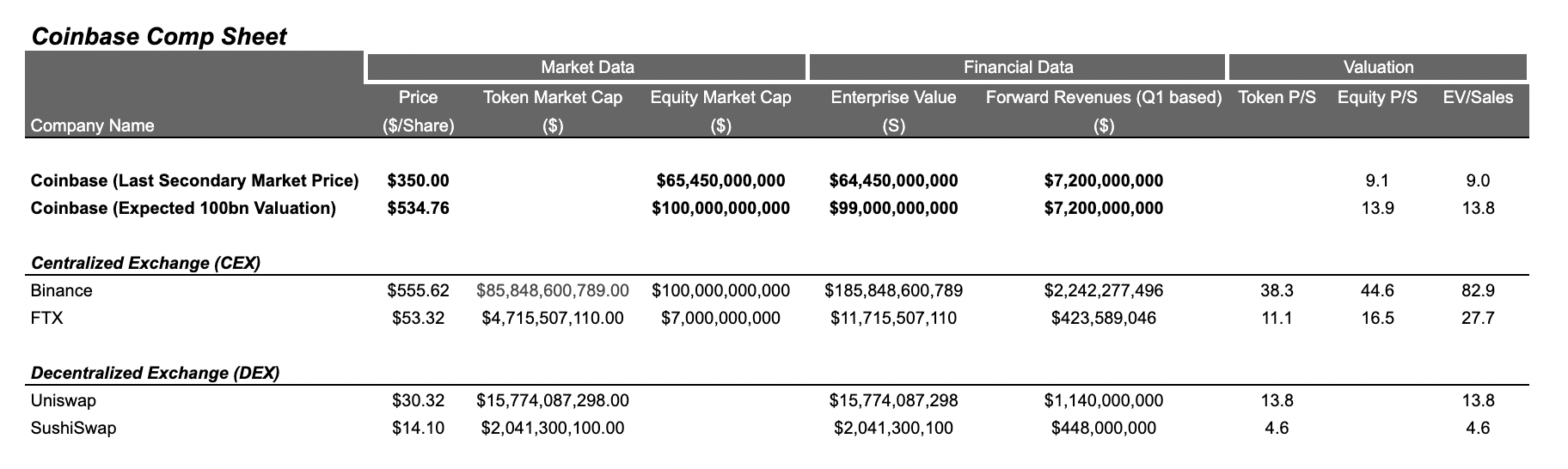

While equity sell-side desks are barely even talking about COIN’s arrival (more on this below), clearly the digital asset native world has recognized what this earnings result means for Coinbase’s competitors, and the market has repriced these tokens accordingly. As we discussed a few months ago, there are some nuances when making apples-to-apples enterprise value comparisons between companies with only equity, only tokens, and those that have both tokens and equity in their capital structures, but it is unmistakably clear that the market has been undervaluing both the growth potential and earnings potential of these giant financial entities. And to top things off, online brokerage app Robinhood followed up with their own announcement last week, showcasing that 9.5 million customers traded digital assets in Q1, up from 1.7 million in Q4 2020. That’s pretty astonishing growth. This is a market that rewards growth and doesn’t demand earnings --- what will equity investors do with a company that has both?

Source: Coinbase, Arca Estimates

Somewhat surprisingly, there really isn’t much of a buzz about COIN in the traditional debt and equity world (perhaps that’s because the sell-side is too busy counting losses from the Archegos blowup to focus on actual profits from financial institutions). By foregoing the traditional IPO in favor of a direct listing, the market lacks an underwriter selling this to institutional investors, and without a roadshow or underwritten process, it’s just not on every investor’s radar yet. And we don’t have a lot of public data to suggest how direct listings of well known companies will trade -- Spotify (SPOT) traded straight up in 2018 while Slack (WORK) shot up and then traded down for the next six months in 2019. There is a good chance COIN could take some time before finding a real market base.

| Spotify (SPOT) prices after direct listing in 2018 |

Slack (WORK) prices after direct listing in 2019 |

|

|

Source: Bloomberg

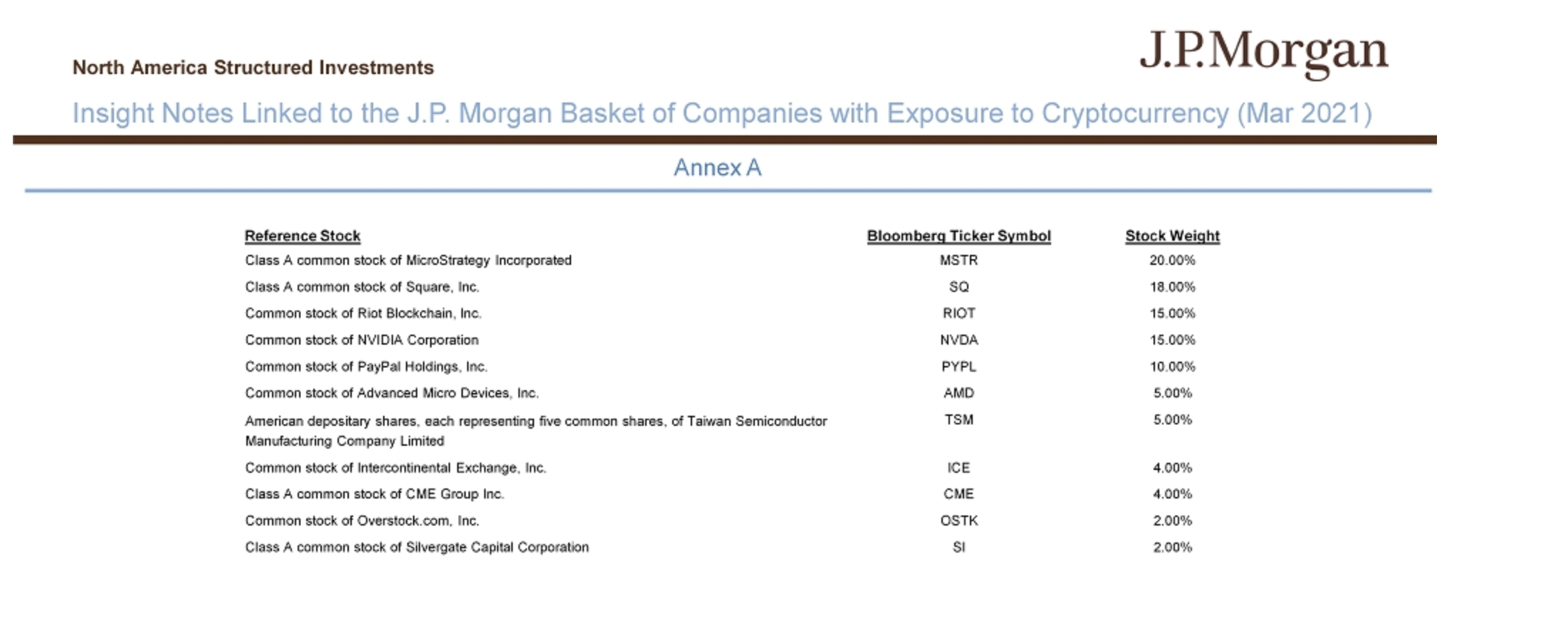

On the other hand, while pensions, endowments, family offices and even fixed income investors have found ways to gain exposure to digital assets in some way, shape or form, there is still one specific group of investors that has had little to no ability to invest in digital assets to date -- financial advisors and US equity mutual funds. And it just so happens that equity funds are seeing record inflows, while their choices for investing in the equities of digital asset companies has been quite limited to date. Some equity investors can invest in the stocks of mining companies which largely trade on Asian, Canadian and European exchanges, with companies like Hut 8, Canaan, and Argo Blockchain all having market caps less than $3 billion. Or they could invest in the slightly larger non-US listed stocks of other exchanges and brokerages, like Galaxy Digital, Voyageur and Diginex, whose stocks have already risen 760%, 4190% and 88% in the past 6 months. Or they can invest in the complete nonsense “cryptocurrency basket” from JP Morgan (which offers companies with VERY loose ties to the fate of digital assets).

Amidst this backdrop, it’s anyone’s guess how COIN will trade out of the gate. But the price action of CeFi tokens and existing digital asset equities gives pretty good clues as to how this will ultimately be perceived.

The DeFi Senior / Sub Relationship

Coinbase and CeFi are great -- but look closer at the table above and you’ll notice the tokens of the two fastest growing “companies” in digital assets (Uniswap and Sushiswap), in the fastest growing sector (DeFi), are trading at very moderate price-to-sales multiples relative to their centralized peers. And this doesn’t even include many other incredibly cheap sub-sectors of DeFi, such as insurance and traditional banking. As amazing as CeFi is, DeFi may be poised for even greater growth. Jim Bianco puts it best, calling them “taxis in a ride-share world”.

.png?width=349&name=unnamed%20(95).png)

While Coinbase news and price action will undoubtedly be all over CNBC and the Wall Street Journal this week, DeFi is still barely (if at all) mentioned. There are still so many misconceptions about DeFi, often from those who still confuse using DeFi with investing in DeFi. So let’s break down the difference using a traditional fixed income concept -- seniority.

When investing across debt and equities, there is a waterfall of claims on a company’s assets. The senior secured debt has the highest claim, followed by senior unsecured debt, subordinated debt, and ultimately equity. Naturally, the returns required to compensate investors for these additional risks are generally inversely correlated, as expected equity returns > subordinated bond returns > senior unsecured bond returns > senior secured debt returns.

This same risk-versus-reward relationship can be seen in DeFi (as well as in the decentralized base layer protocols themselves). If you choose to be a passive owner of a network’s growth via owning its native token, you may be rewarded with price gains, but those gains will likely be less than if you become an active participant of a network’s growth via staking, lending or yield farming. Of course, if you are an active participant, you are taking on more risk due to potential hacks and pooled losses that you don’t share if you are simply a passive owner. Essentially, passive ownership is like a senior claim, whereas active participation is like a subordinated claim. There are different tiers of value -- the more risk you take, the higher return you can expect, with potentially higher losses as well. Further, these additional benefits change rapidly in real-time, as rates are variable, so you may lock in a yield one minute, but as participation increases, your yield is reduced greatly. With the current high yield environment, it’s not surprising that Nexus Mutual, which provides insurance on losses due to active participant risk, is one of the fastest growing companies in all of digital assets.

Yields on select Defi and Protocol tokens - Snapshot in time (April 11, 2021)

.png?width=584&name=unnamed%20(94).png)

Source: Company websites and Arca Estimates

The nuance here is that the price to purchase “active and passive” tokens is the same - as it is just one token that you own where you choose what (if anything) to do with it. Therefore, the investment thesis for owning DeFi tokens without actively participating in the network is that each token is worth whatever one participating token is worth. For example, if there is $1 of “dividends” to be paid out on a token worth $10, if every token holder stakes, the yield for every token holder would be 10%. If, however, only one token holder with $1 worth of tokens stakes, that individual token holder will yield 100%. Each non-staked token is therefore more valuable because it could be bought and subsequently staked by someone else who can then maximize the return potential by taking more risk (and the original solo staker’s yield will go down as she now shares the yield with others).

Owning but not participating is a bet on growth, whereas owning and participating is a bet on the equity plus an attached warrant. But since each token trades at the same price, and the price is therefore determined by what it could be worth, the yield is determined by the actual cash flows accruing to the participants. The price will be the same but the total return changes based on your actions and your willingness to participate and take additional risk.

This concept has been defined further with a new term -- internet bonds.

“Internet Bonds, a new type of reward-based digital work agreement, and the introduction of a risk-free rate in the decentralized Web3.0 economy are the critical steps to instigate this broader participation and push the blockchain industry to the next level of the adoption curve. Internet Bonds offer a conceptual framework for understanding and valuing these new types of digital work agreements between the lenders of capital and resources and the protocol(s) operating on the base layer of the new internet economy.

Akin to traditional bond structures, Internet Bonds represent an agreement between the bond issuer (the protocol) and the bondholder (the validator).

However, unlike traditional bond structures, internet bondholders in Web3.0 are lenders of capital, labor, resources, and owners of the network at the same time. An Internet Bond is a new type of reward-based digital work agreement that can be best described as a hybrid-perpetual bond with debt and equity-like characteristics.”

The next time someone tries to tell you digital assets can’t be valued, simply smile and nod as you collect your yield on internet bonds.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency